Learn how to maximize the benefits of using debit cards while keeping your financial information secure. Discover essential tips on using debit cards safely and wisely to protect your money and personal data.

Understanding Debit Card Terms

Before you can use your debit card safely and wisely, it’s essential to understand the common terms associated with it. Familiarizing yourself with these terms will help you navigate the world of debit cards with confidence:

1. PIN (Personal Identification Number)

Your PIN is a four-to-six-digit code that you use to authenticate transactions at ATMs and during in-person purchases. Memorize your PIN and never share it with anyone.

2. ATM (Automated Teller Machine)

ATMs are electronic machines that allow you to access your checking account to withdraw cash, deposit funds, or check your balance, 24/7. You’ll need your debit card and PIN to use an ATM.

3. POS (Point of Sale) Terminal

A POS terminal is the electronic device used by merchants to process card payments. When you swipe, insert, or tap your debit card at a POS terminal, you’re authorizing a transaction.

4. Debit Card Number

This is the 16-digit number located on the front of your debit card. It’s unique to your card and is used to identify your account when making purchases.

5. Expiration Date

The expiration date on your debit card indicates when the card is no longer valid. You can find it printed on the front of your card, usually in the format MM/YY.

6. CVV/CVC Code

The Card Verification Value (CVV) or Card Verification Code (CVC) is a three or four-digit security code located on the back of your card, usually in the signature strip. It’s used to verify online and over-the-phone transactions.

7. Overdraft

An overdraft occurs when you attempt to make a purchase that exceeds the available balance in your checking account. Depending on your bank’s policy, the transaction may be declined, or you may be charged an overdraft fee.

8. Contactless Payment

Contactless payment methods, such as tap-and-go or mobile wallets, allow you to make purchases by simply tapping your debit card or smartphone on a compatible POS terminal. This technology utilizes NFC (Near Field Communication) for faster transactions.

Choosing the Right Debit Card

Not all debit cards are created equal. With so many options available, it’s important to choose one that aligns with your spending habits and financial needs. Here are some key factors to consider:

1. Fees

Pay close attention to potential fees:

- Monthly fees: Some banks charge a monthly fee for certain accounts or debit cards.

- ATM fees: Using an out-of-network ATM can lead to withdrawal fees from both your bank and the ATM provider. Look for a card that reimburses these fees or offers a wide ATM network.

- Overdraft fees: Overdraft fees can quickly add up. Consider opting for a card with overdraft protection or set up a low balance alert to avoid them.

- Foreign transaction fees: If you travel frequently, look for a card with low or no foreign transaction fees.

2. Rewards Programs

Some debit cards offer rewards programs, similar to credit cards. These programs may include:

- Cashback: Earn a percentage of your purchases back as cash rewards.

- Points: Accumulate points that can be redeemed for merchandise, travel, or gift cards.

- Discounts: Receive discounts on specific purchases or with participating retailers.

Carefully evaluate the rewards program and ensure it aligns with your spending patterns.

3. Security Features

Prioritize security features offered by different banks and cards:

- EMV Chip Technology: Opt for cards with EMV chip technology for enhanced security against fraud.

- Fraud Protection: Inquire about the bank’s fraud protection policies and procedures in case of unauthorized transactions.

- Zero Liability Policies: Many banks offer zero liability policies that protect you from liability for fraudulent charges.

4. Account Features

Consider the features and services offered with the debit card account:

- Online and Mobile Banking: Choose a bank that provides convenient online and mobile banking platforms for easy account management, bill payments, and money transfers.

- Customer Service: Look for a bank with responsive and reliable customer service channels in case you need assistance.

- Branch Availability: If you prefer in-person banking, consider the bank’s branch network and proximity to your location.

Using Debit Cards for Everyday Purchases

Debit cards are incredibly convenient for daily spending. They offer an immediate transaction process, deducting the purchase amount directly from your checking account. This direct link to your funds makes it easier to track spending and manage your budget effectively.

Here are some common everyday scenarios where using a debit card is beneficial:

- Groceries: Quickly and easily pay for your weekly groceries without needing to carry cash.

- Gas Stations: Most gas stations accept debit cards directly at the pump, speeding up your fueling process.

- Online Shopping: Debit cards are widely accepted for online purchases, providing a secure way to pay without sharing your credit card information.

- Dining Out: Conveniently pay for meals at restaurants and track your spending easily.

- Bills and Utilities: Set up automatic payments for recurring bills like utilities, rent, or subscriptions, ensuring timely payments and avoiding late fees.

By utilizing your debit card for these regular expenses, you can streamline your financial transactions and maintain better control over your money.

Monitoring Your Spending

Keeping track of your spending is crucial when using a debit card, as it helps you stay on top of your finances and avoid overspending. Here are some effective ways to monitor your debit card expenses:

1. Regularly Review Your Bank Statements

Make it a habit to review your bank statements at least monthly, if not more frequently. Online banking makes this convenient, allowing you to see all your transactions in one place. Scrutinize each debit card transaction, checking for any discrepancies or unauthorized charges.

2. Utilize Budgeting Apps

Numerous budgeting apps can link to your bank account and automatically categorize your debit card transactions. These apps provide a clear picture of where your money is going and can help you identify areas where you can cut back on spending.

3. Set Up Account Alerts

Most banks offer account alerts that notify you of specific transactions or account balances. Consider setting up alerts for low balances, large purchases, or international transactions to stay informed and prevent potential issues.

4. Maintain a Spending Diary

For a more hands-on approach, keep a spending diary or spreadsheet to track your debit card purchases. Note down the date, amount, and purpose of each transaction. This practice can increase your awareness of your spending habits and help you make more conscious financial decisions.

5. Reconcile Your Transactions

Regularly reconcile your debit card transactions with your bank statements. This involves comparing your records to the bank’s records to ensure accuracy and identify any errors or discrepancies.

Setting a Spending Limit

One of the smartest moves you can make with your debit card is setting a daily or monthly spending limit. This acts as a financial safety net, preventing accidental overspending or limiting the damage in case of fraud.

How to Set a Limit:

- Contact your bank or credit union: Most financial institutions allow you to set spending limits directly through them. You can often do this through their website, mobile app, or by calling customer service.

- Use your bank’s mobile app: Many banking apps have built-in features for managing your card, including setting spending limits.

Benefits of a Spending Limit:

- Budgeting Control: It helps you stick to your budget and avoid overdraft fees.

- Fraud Protection: If your card is compromised, a spending limit can minimize potential losses.

- Increased Awareness: It makes you more conscious of your spending habits.

Building an Emergency Fund

A key aspect of using debit cards wisely is ensuring you have a financial safety net to fall back on. Unexpected expenses, like car repairs or medical bills, can pop up at any time. Having an emergency fund prevents these situations from derailing your finances and potentially leading to debt.

How much should you save? A good rule of thumb is to have 3-6 months’ worth of living expenses saved. This may seem like a daunting amount, but even small, consistent contributions add up over time.

Where should you keep it? Your emergency fund should be easily accessible, so a high-yield savings account or money market account is a good option. These accounts offer higher interest rates than traditional savings accounts, helping your money grow faster.

Tips for Building Your Emergency Fund:

- Start small: Begin by setting aside a small amount each week or month, gradually increasing the amount as you are able.

- Automate your savings: Set up automatic transfers from your checking account to your emergency fund. This makes saving effortless and ensures consistency.

- Cut back on unnecessary expenses: Identify areas where you can reduce spending and redirect those funds to your emergency fund.

- Windfalls: Deposit any unexpected income, such as tax refunds or bonuses, directly into your emergency fund.

Understanding Overdraft Fees

Overdraft fees are charges incurred when you attempt to make a debit card purchase or withdrawal exceeding your available account balance. While some banks offer overdraft protection services, they often come with hefty fees. Understanding how overdraft fees work is crucial to avoid unexpected charges and manage your finances responsibly.

How Overdraft Fees Work:

When you initiate a transaction exceeding your account balance, the bank or credit union may approve it, causing your account to become overdrawn. This convenience comes at a cost, with most financial institutions imposing overdraft fees for each transaction made while your account is negative. These fees can range from $25 to $35 or more per transaction, quickly accumulating if you’re not careful.

Types of Overdraft Fees:

- Overdraft Fees: Charged for each approved transaction exceeding your balance.

- Sustained Overdraft Fees: Applied if your account remains negative for a specific duration, often several days.

- Returned Item Fees: Charged by both the merchant and your bank if a transaction is declined due to insufficient funds.

Avoiding Overdraft Fees:

Preventing overdraft fees is essential for maintaining a healthy financial standing. Here are some practical tips to avoid these unnecessary charges:

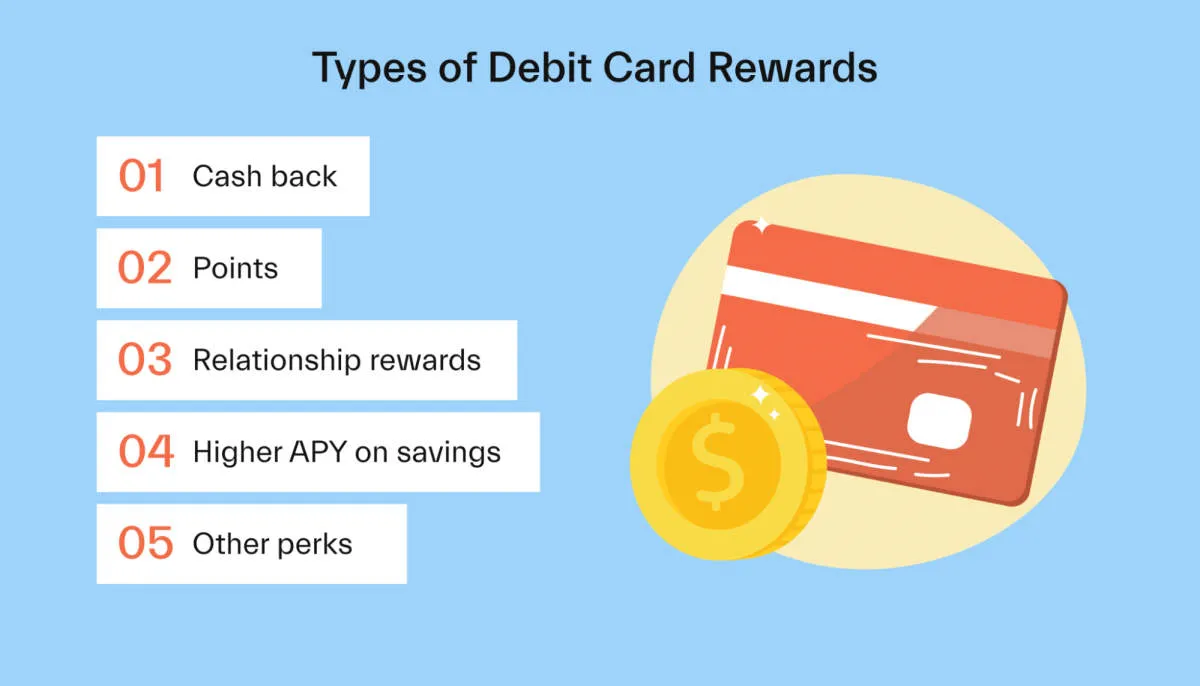

Using Debit Card Rewards Programs

Some debit cards, though not all, offer rewards programs similar to credit cards. These programs can include:

- Cashback: Earn a percentage back on eligible purchases, often deposited directly into your account.

- Points: Accumulate points for transactions, redeemable for merchandise, gift cards, or travel.

- Discounts: Enjoy reduced prices at participating retailers or on specific services.

To maximize debit card rewards:

- Choose a card with a rewarding program: Research and compare offerings from different banks and credit unions.

- Understand the terms and conditions: Pay attention to earning rates, redemption options, and any limitations or fees.

- Track your rewards: Most banks provide online banking or mobile apps to monitor your points or cashback balance.

- Redeem rewards strategically: Choose redemption options that offer the best value for you, whether it’s cashback, travel, or merchandise.

Remember, while rewards programs can provide added benefits, they shouldn’t encourage overspending. Use your debit card responsibly and prioritize your financial well-being.

Protecting Your Debit Card Information

Protecting your debit card information is crucial to prevent unauthorized access and potential financial losses. Here are essential steps to safeguard your card details:

1. Be Mindful of Phishing Attempts:

Phishing scams often target debit card information through deceptive emails, text messages, or phone calls. Be cautious of unsolicited requests for your card details, PIN, or online banking credentials. Remember, legitimate financial institutions will never ask for sensitive information through these channels.

2. Secure Your Online Transactions:

When shopping online, ensure that the website you are using is secure. Look for “https://” in the URL and a padlock icon in the address bar. These indicators signify that the website uses encryption to protect your data during transmission. Additionally, be wary of using public Wi-Fi networks for financial transactions, as they may be vulnerable to hacking.

3. Monitor Your Account Regularly:

Regularly review your bank statements and online account activity for any suspicious transactions. If you detect unauthorized purchases or withdrawals, report them to your bank immediately. Prompt reporting is crucial for minimizing potential losses and initiating investigations.

4. Choose Strong PINs and Passwords:

Select a strong and unique PIN for your debit card. Avoid using easily guessable numbers like your birthdate or consecutive digits. Similarly, create a complex password for your online banking account, combining uppercase and lowercase letters, numbers, and symbols.

5. Keep Your Card Secure:

Treat your debit card like cash. Keep it in a safe place and avoid sharing your PIN or card details with anyone. Be cautious of your surroundings when using ATMs or making payments at point-of-sale terminals. Cover the keypad while entering your PIN to prevent shoulder surfing.

Seeking Professional Advice

While this article provides helpful tips for safe and wise debit card usage, remember that it’s not a substitute for professional financial advice. Consider seeking guidance from a financial advisor for personalized strategies. They can help you with:

- Budgeting and Saving: Developing a personalized budget that aligns with your financial goals and finding ways to maximize your savings using debit card rewards programs.

- Debt Management: Creating a plan to manage and pay off existing debt, and advising on responsible debit card use to avoid accumulating new debt.

- Investment Options: Exploring investment opportunities that suit your risk tolerance and financial objectives, potentially helping you grow your money beyond what a basic checking account offers.

- Fraud Protection: Providing insights into advanced security measures and strategies to safeguard your debit card and financial information from potential threats.

A financial advisor can offer tailored advice based on your specific financial situation and goals. Don’t hesitate to reach out for professional guidance to ensure you’re making the most of your debit card and managing your finances responsibly.

Conclusion

In conclusion, utilizing debit cards safely and wisely involves monitoring transactions regularly, safeguarding personal information, and being cautious of phishing scams.

{kind=link}