In the world of personal finance, having a good understanding of the various types of credit cards available is essential. From rewards cards to balance transfer cards, each type serves a different purpose. Let’s delve into the different types of credit cards to help you choose the one that best fits your financial needs.

Types of Credit Cards

Navigating the world of credit cards can feel overwhelming with the sheer variety available. Understanding the different types of credit cards is crucial to selecting one that aligns with your spending habits and financial goals. Let’s break down some of the most common types:

1. Standard Credit Cards

These are the most prevalent type of credit card. They typically come with a set credit limit, interest rates, and may offer basic rewards programs or perks. Standard cards are a good starting point for building credit.

2. Rewards Credit Cards

If you’re looking to earn something back on your spending, rewards cards are the way to go. These cards offer points, miles, or cash back on purchases. Some popular categories for rewards include:

- Travel Rewards: Earn miles or points redeemable for flights, hotels, and other travel expenses.

- Cash Back: Receive a percentage of your purchases back as cash rebates or statement credits.

- Points Programs: Accumulate points to redeem for a variety of merchandise, gift cards, or travel options.

3. Balance Transfer Credit Cards

Carrying high-interest debt? Balance transfer cards often come with an introductory 0% APR period, allowing you to transfer balances from other cards and pay down debt interest-free for a set time. Be mindful of balance transfer fees and the regular APR that kicks in after the promotional period.

4. Secured Credit Cards

Designed for individuals with limited or no credit history, secured cards require a cash deposit as collateral. This deposit typically becomes your credit limit. Secured cards provide a way to build credit responsibly and graduate to other card types in the future.

5. Business Credit Cards

Tailored specifically for business owners, these cards help separate business expenses from personal ones. They often offer perks like higher credit limits, expense tracking features, and rewards programs geared towards business needs.

Choosing the Right Credit Card

With a vast array of credit cards available, selecting the right one can feel overwhelming. It’s essential to carefully consider your spending habits, financial goals, and individual needs to make an informed decision. Here’s a breakdown of factors to help you choose:

1. Analyze Your Spending Habits:

Start by understanding where your money goes each month. Are you a frequent traveler? Do you dine out often? Identifying your primary spending categories will allow you to focus on cards that offer rewards or benefits aligned with your lifestyle.

2. Consider Your Credit Score:

Your credit score plays a significant role in credit card approvals and interest rates. Individuals with excellent credit have access to cards with premium perks and lower APRs. If you’re building or rebuilding credit, secured cards or cards designed for fair credit can be good options.

3. Evaluate Rewards Programs:

Credit card rewards can offer significant value if utilized effectively. Cashback cards provide a percentage back on purchases, while travel rewards cards allow you to earn points or miles redeemable for flights, hotels, and more. Points-based rewards cards provide flexibility, often allowing redemption for a variety of options like merchandise, gift cards, or travel.

4. Compare Fees and Interest Rates:

Pay close attention to fees, including annual fees, balance transfer fees, and foreign transaction fees. APR (Annual Percentage Rate) represents the cost of borrowing money on your card. Choosing a card with a low APR is crucial, especially if you plan to carry a balance.

5. Read the Fine Print:

Before committing to a credit card, thoroughly review the terms and conditions. Pay attention to details such as grace periods, penalty APRs, and any limitations on rewards programs. Understanding the fine print will help you avoid unexpected surprises and make informed decisions about your credit card usage.

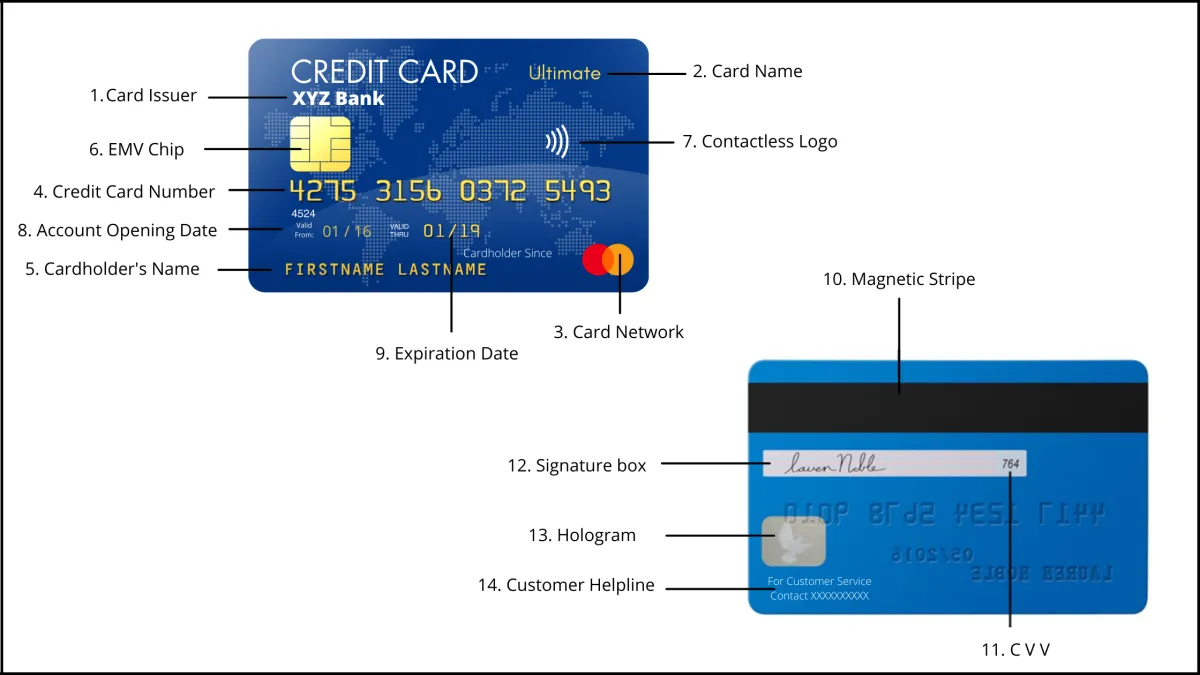

Understanding Credit Card Terms

Navigating the world of credit cards can feel like learning a new language. To make informed decisions about which card is right for you, it’s crucial to understand the terminology. Here are some key credit card terms you should know:

General Terms

- APR (Annual Percentage Rate): This is the yearly interest rate charged on your credit card balance. It reflects the cost of borrowing money. There are often different APRs for purchases, balance transfers, and cash advances.

- Credit Limit: The maximum amount of money you can charge to your credit card.

- Minimum Payment: The minimum amount you need to pay each month to avoid late fees and keep your account in good standing.

- Grace Period: The time you have to pay your balance in full before interest is charged.

- Balance Transfer: Moving a balance from one credit card to another, often to secure a lower interest rate.

- Cash Advance: Withdrawing cash from an ATM using your credit card. This usually comes with a higher APR and fees.

- Foreign Transaction Fee: A charge applied to purchases made outside your home country.

Fees

- Annual Fee: A yearly charge for having the credit card.

- Balance Transfer Fee: Charged when transferring a balance from another credit card.

- Late Payment Fee: Penalty for not making the minimum payment by the due date.

- Over-the-Limit Fee: Charged if your balance exceeds your credit limit.

Other Important Terms

- Credit Score: A numerical representation of your creditworthiness, influencing your ability to obtain credit and interest rates.

- Rewards Program: Offers points, miles, or cash back for purchases made with the card.

- Introductory Rate: A temporary, typically lower interest rate offered to new cardholders for a limited time.

By familiarizing yourself with these credit card terms, you’ll be better equipped to compare different cards, understand your statements, and manage your credit responsibly.

Interest Rates and Fees

Interest rates and fees are crucial aspects of credit cards that significantly impact their overall cost. Understanding these factors is vital for selecting a card that aligns with your spending habits and financial goals.

Interest Rates

Credit card interest rates, often expressed as Annual Percentage Rates (APRs), represent the cost of borrowing money on your card. When you carry a balance on your credit card, interest is charged on the outstanding amount.

- Purchase APR: This rate applies to purchases made with your credit card.

- Balance Transfer APR: This rate applies to balances transferred from other credit cards.

- Cash Advance APR: This rate applies to cash withdrawals made using your credit card.

Credit card interest rates can be fixed or variable. Fixed rates remain constant over time, while variable rates fluctuate based on market conditions, typically tied to a benchmark rate like the prime rate.

Fees

Credit cards often come with various fees that can add to the overall cost of card ownership.

- Annual Fees: Some credit cards charge an annual fee for the benefits and perks they offer. These fees are typically charged once a year.

- Balance Transfer Fees: Transferring a balance from one credit card to another may incur a balance transfer fee, usually a percentage of the transferred amount.

- Cash Advance Fees: Withdrawing cash from an ATM or bank using your credit card typically incurs a cash advance fee, which can be either a flat fee or a percentage of the amount withdrawn.

- Late Payment Fees: Failing to make your minimum payment by the due date can result in a late payment fee.

- Foreign Transaction Fees: Using your credit card for purchases in a foreign currency may result in foreign transaction fees, usually a percentage of the transaction amount.

Credit Card Rewards Programs

Many credit cards come with enticing rewards programs designed to incentivize card usage. These programs typically fall into a few main categories:

1. Cash Back

Cash back programs are straightforward. You earn a percentage of your spending back as cash. Some cards offer a flat rate on all purchases, while others provide higher rates in specific spending categories like groceries or gas.

2. Points

Points programs are incredibly versatile. You accumulate points for every dollar spent, which can later be redeemed for various rewards such as travel, merchandise, gift cards, or even statement credits. The value of each point varies depending on the card and how you choose to redeem them.

3. Miles

Travel enthusiasts often gravitate towards miles cards. These cards reward your spending with miles, typically redeemable for flights, hotel stays, car rentals, and other travel-related expenses. Some cards partner with specific airlines or hotel chains, offering bonus miles for bookings made through their platforms.

4. Other Perks and Benefits

Besides the primary rewards structure, many credit cards offer additional perks, such as airport lounge access, travel insurance, purchase protection, extended warranties, and exclusive discounts with partner merchants. These benefits can enhance the overall value proposition of the card beyond the core rewards program.

Choosing the Right Rewards Program

The best credit card rewards program depends entirely on your spending habits and personal preferences. Carefully evaluate your needs and spending patterns to determine which program aligns best with your lifestyle. Consider factors like:

- Spending categories: Do you spend heavily on groceries, travel, or dining out?

- Redemption options: Are you looking for cash back, travel rewards, or merchandise?

- Annual fees: Some premium rewards cards come with annual fees. Ensure the potential rewards outweigh the cost.

How to Apply for a Credit Card

Applying for a credit card is a relatively straightforward process, but it’s important to be prepared. Here’s a step-by-step guide to help you through it:

1. Check Your Credit Score

Before you apply for a credit card, it’s crucial to know where your credit stands. Your credit score is a significant factor in determining whether your application gets approved and what interest rates you’ll be offered. You can obtain a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually at AnnualCreditReport.com.

2. Research and Compare Cards

With countless credit cards available, each catering to different needs and financial situations, take time to research and compare various options. Consider factors like:

- Annual Percentage Rate (APR): This is the cost of borrowing money on your credit card. Lower APRs are generally better.

- Fees: Check for annual fees, balance transfer fees, foreign transaction fees, and late payment fees.

- Rewards: Some cards offer cash back, travel points, or other incentives for spending. Choose a rewards program that aligns with your spending habits.

- Credit Limit: Your credit limit is the maximum amount you’re allowed to borrow on the card.

3. Choose the Right Card and Gather Your Information

Once you’ve narrowed your choices, select the credit card that best suits your financial goals and spending patterns. Be prepared to provide the following information during the application process:

- Social Security number

- Date of birth

- Current address

- Annual income

- Employment information

4. Complete the Application

You can typically apply for a credit card online, over the phone, or in person at a bank or credit union. Fill out the application completely and accurately. Be prepared to answer questions about your credit history and income.

5. Wait for a Decision

After submitting your application, the credit card issuer will review your information and make a decision. You’ll typically receive a response within a few days or weeks. If you’re approved, you’ll receive your card in the mail along with the terms and conditions.

Using Credit Cards Responsibly

While credit cards offer convenient purchasing power and the potential for rewards, responsible usage is crucial. Misusing credit can lead to debt and damage your credit score. Here are key tips for responsible credit card use:

Budgeting and Tracking

Track your spending. Utilize budgeting apps or maintain a spreadsheet to monitor your credit card purchases. This helps you stay aware of your spending habits and avoid overspending.

Making Timely Payments

Pay on time, every time. Late payments result in late fees and can harm your credit score. Set up payment reminders or consider automating payments to ensure timeliness.

Managing Credit Utilization

Keep credit utilization low. Aim to use no more than 30% of your available credit limit. High credit utilization can negatively impact your credit score. Consider requesting a credit limit increase if needed, but avoid increasing your spending proportionally.

Resisting Impulse Purchases

Avoid impulse purchases. Before using your credit card, ask yourself if you truly need the item and if it aligns with your budget. Delaying gratification and planning purchases can prevent unnecessary debt.

Understanding Fees and Interest

Review your credit card agreement. Be aware of interest rates, annual fees, late payment fees, and other charges. Choose a card with fees and terms that align with your spending habits and financial goals.

Protecting Your Information

Practice credit card safety. Safeguard your card information by keeping it secure, being cautious about online transactions, and regularly reviewing your statements for unauthorized charges.

Managing Credit Card Debt

Having and using credit cards responsibly can be a powerful tool for building credit and managing your finances. However, it’s easy to overspend and fall into credit card debt. If you’re struggling to manage your credit card debt, here are a few tips:

Create a Budget and Stick to It

The first step to getting out of credit card debt is to understand where your money is going. Create a budget that tracks your income and expenses, so you can see how much money you have coming in and going out each month. This will help you identify areas where you can cut back on spending and free up more money to put towards your debt.

Make More Than the Minimum Payment

Making only the minimum payment on your credit card each month can keep you in debt for years and cost you thousands of dollars in interest. Whenever possible, try to make more than the minimum payment to pay down your debt faster and save on interest charges. Even an extra $50 or $100 each month can make a big difference over time.

Consider a Balance Transfer

If you have a high-interest rate on your credit card, consider transferring your balance to a card with a lower interest rate. This can save you money on interest charges and help you pay off your debt faster. Be sure to factor in any balance transfer fees when comparing offers.

Negotiate With Your Credit Card Issuer

If you are struggling to make your payments, don’t be afraid to negotiate with your credit card issuer. They may be willing to work with you to lower your interest rate, waive fees, or create a more manageable payment plan.

Seek Help From a Credit Counseling Agency

If you’re feeling overwhelmed by your credit card debt, a non-profit credit counseling agency can provide you with free or low-cost guidance and support. They can help you create a budget, negotiate with creditors, and explore different debt relief options.

Protecting Your Credit Card Information

While credit cards offer incredible convenience and security for transactions, protecting your credit card information is paramount to prevent fraud and unauthorized access.

Here are key measures to safeguard your credit card information:

- Be vigilant online: When making online purchases, ensure the website uses secure encryption (look for “https://” and a padlock icon in the address bar). Avoid using public Wi-Fi networks for financial transactions, as they are often unsecured.

- Monitor your statements regularly: Review your credit card statements each month for any suspicious activity. Contact your issuer immediately if you notice any unauthorized transactions.

- Use strong passwords and enable two-factor authentication: Create complex passwords for your online credit card accounts and enable two-factor authentication whenever available. This adds an extra layer of security, requiring a unique code sent to your phone or email in addition to your password.

- Be wary of phishing scams: Phishing attempts often come in the form of emails or text messages that appear to be from a legitimate source. They may ask for your credit card details or direct you to fake websites designed to steal your information. Never click on suspicious links or provide personal or financial information through unsolicited requests.

- Report lost or stolen cards immediately: If your credit card is lost or stolen, report it to your issuer as soon as possible. They can deactivate your card and prevent fraudulent charges. Keep a record of your issuer’s contact information readily accessible for emergencies.

By following these security practices, you can significantly reduce the risk of credit card fraud and enjoy peace of mind knowing your financial information is protected.

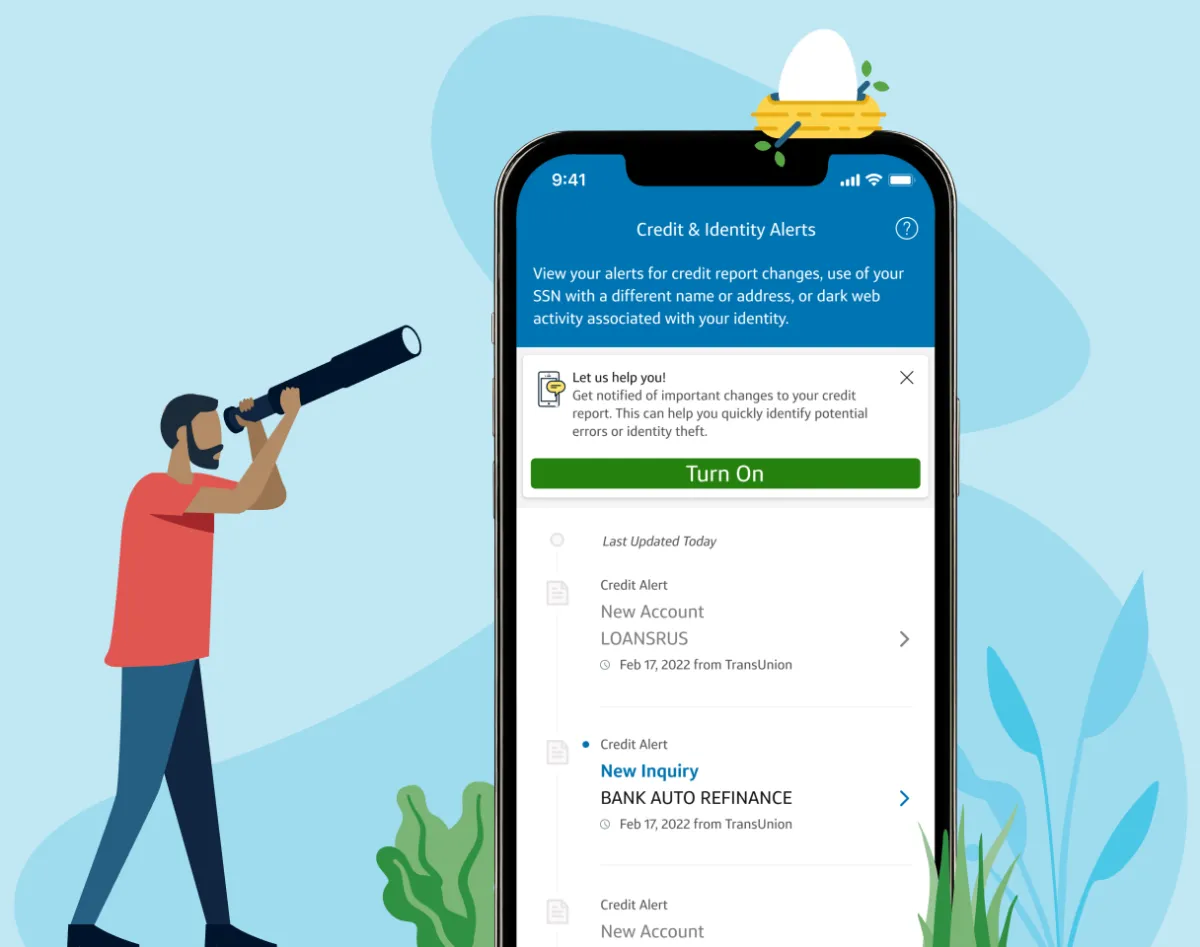

Monitoring Your Credit Card Activity

Regularly monitoring your credit card activity is crucial for maintaining good financial health and protecting yourself from fraud. Here’s why it’s so important and how to do it effectively:

Why It’s Essential:

- Early Fraud Detection: Catching unauthorized transactions quickly minimizes your liability and prevents further damage.

- Error Identification: Spotting billing errors, such as double charges or incorrect amounts, ensures you’re not paying more than you should.

- Spending Awareness: Tracking your spending habits helps you stay within budget and identify areas where you might be overspending.

- Credit Score Protection: Unpaid or fraudulent charges can negatively impact your credit score. Monitoring helps you address issues promptly and maintain a good score.

How to Monitor Your Activity:

- Online Account Access: Most credit card issuers provide online portals or mobile apps for real-time account access. You can view recent transactions, check your balance, and set up alerts.

- Review Statements Carefully: Examine your monthly statement for any discrepancies or unfamiliar charges. Don’t just look at the total amount due.

- Set Up Account Alerts: Many banks offer alerts for transactions above a certain amount, international purchases, or when your balance is low. These alerts can help you catch fraudulent activity immediately.

- Utilize Credit Monitoring Services: Consider subscribing to a credit monitoring service that provides alerts about changes to your credit report, including new accounts or inquiries.

Conclusion

It is important to understand the various types of credit cards available to make informed financial decisions. From rewards cards to secured cards, choosing the right one can help you build credit and maximize benefits.

{kind=link}