Planning for retirement is essential for a secure financial future. Learn valuable tips on budgeting, savings, investments, and more to ensure a comfortable retirement lifestyle in our exclusive guide on Financial Planning Tips for Retirement.

Setting Retirement Goals

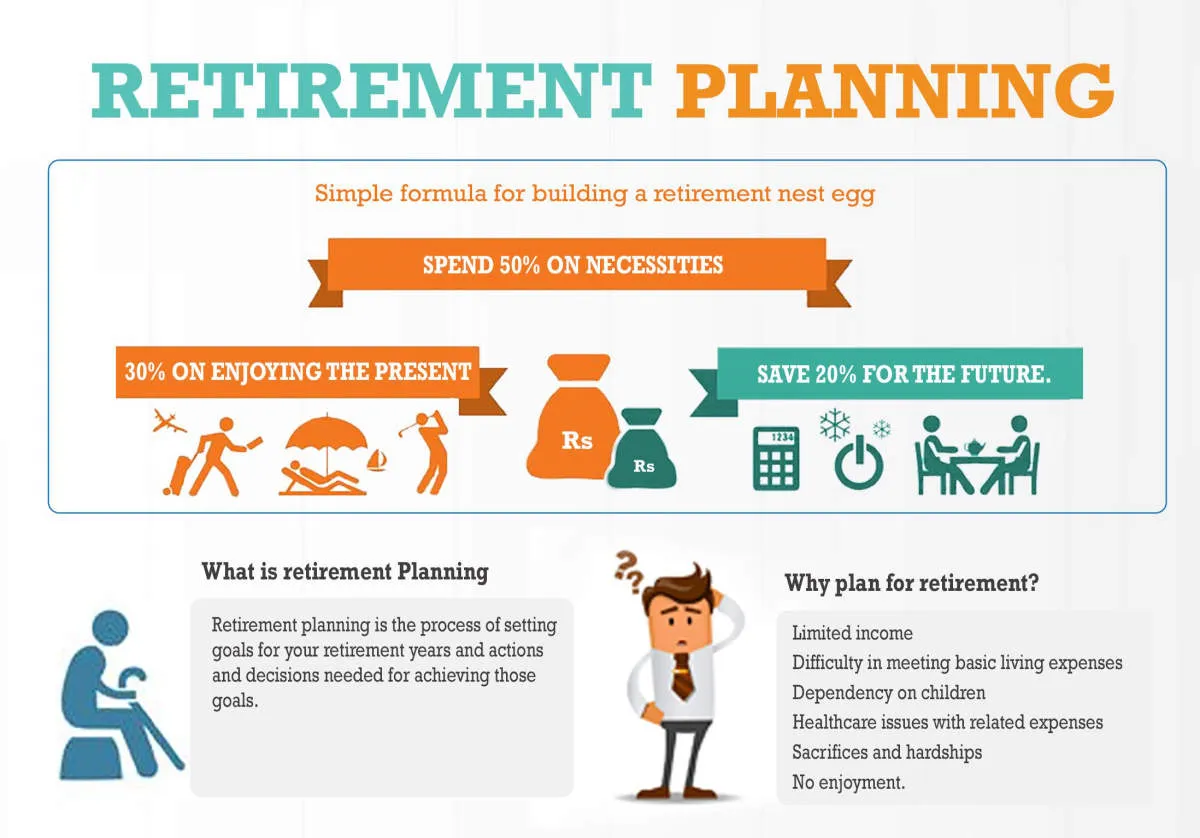

Retirement planning is not just about saving money; it’s about designing your ideal future. To make that future a reality, you need clear retirement goals. These goals provide a roadmap for your financial planning journey, helping you determine how much to save, how to invest, and when you can comfortably retire.

Start by envisioning your ideal retirement lifestyle. Consider these factors:

- Where do you want to live? Will you stay in your current home, downsize, or relocate to a new city or country?

- How do you want to spend your time? Travel, hobbies, volunteering, spending time with family – what brings you joy?

- What are your healthcare needs and expectations? Factor in potential healthcare costs and long-term care needs.

- Do you plan to work part-time in retirement? If so, what type of work interests you, and how much income do you hope to earn?

Once you have a clear picture of your desired retirement lifestyle, translate those aspirations into concrete financial goals. Be specific about how much money you’ll need to support your chosen lifestyle. Online retirement calculators can be helpful tools for estimating these costs.

Remember that retirement goals are not set in stone. Regularly review and adjust them as your circumstances change, your priorities evolve, or you gain a clearer understanding of your financial needs in retirement.

Understanding Retirement Accounts

Retirement accounts are specialized financial accounts designed to help you save and invest for retirement. These accounts come with tax advantages and sometimes employer contributions, making them powerful tools for long-term financial planning.

Here are some key types of retirement accounts:

Employer-Sponsored Plans:

- 401(k): This plan is offered through private employers. You contribute pre-tax income, lowering your taxable income. Some employers offer matching contributions, essentially free money towards your retirement.

- 403(b): Similar to a 401(k) but offered by non-profit organizations like schools and hospitals.

- Thrift Savings Plan (TSP): This is the retirement savings plan for federal employees.

Individual Retirement Accounts (IRAs):

- Traditional IRA: Allows for pre-tax contributions, offering tax advantages in the present. You pay taxes on withdrawals in retirement.

- Roth IRA: You contribute after-tax dollars, meaning your withdrawals in retirement are tax-free.

Other Retirement Accounts:

- SEP IRA: Designed for self-employed individuals and small business owners.

- SIMPLE IRA: A simplified plan for small businesses with fewer than 100 employees.

Contribution Limits: Each type of retirement account has annual contribution limits set by the IRS. These limits can change, so it’s essential to stay informed.

Investment Options: Retirement accounts typically offer a variety of investment options, such as stocks, bonds, and mutual funds. The right investments for you will depend on your risk tolerance, time horizon, and financial goals.

Understanding the rules and benefits of different retirement accounts is crucial for maximizing your retirement savings. Consider consulting with a financial advisor to determine the best options for your individual circumstances.

Building an Emergency Fund

Retirement might seem far off, but establishing healthy financial habits now, like building an emergency fund, is crucial for long-term financial security. While you’re diligently saving for retirement, an unexpected event shouldn’t derail your future plans.

An emergency fund acts as a safety net, covering unforeseen expenses like medical bills, car repairs, or job loss. Without one, you risk tapping into your retirement savings, incurring debt, or facing difficult financial choices.

How Much to Save?

Aim for 3-6 months’ worth of living expenses in your emergency fund. This amount provides a buffer while you navigate unexpected situations without jeopardizing your retirement goals.

Where to Keep Your Emergency Fund

Choose a liquid and easily accessible account for your emergency fund. A high-yield savings account or money market account are suitable options, offering modest growth while keeping your funds readily available.

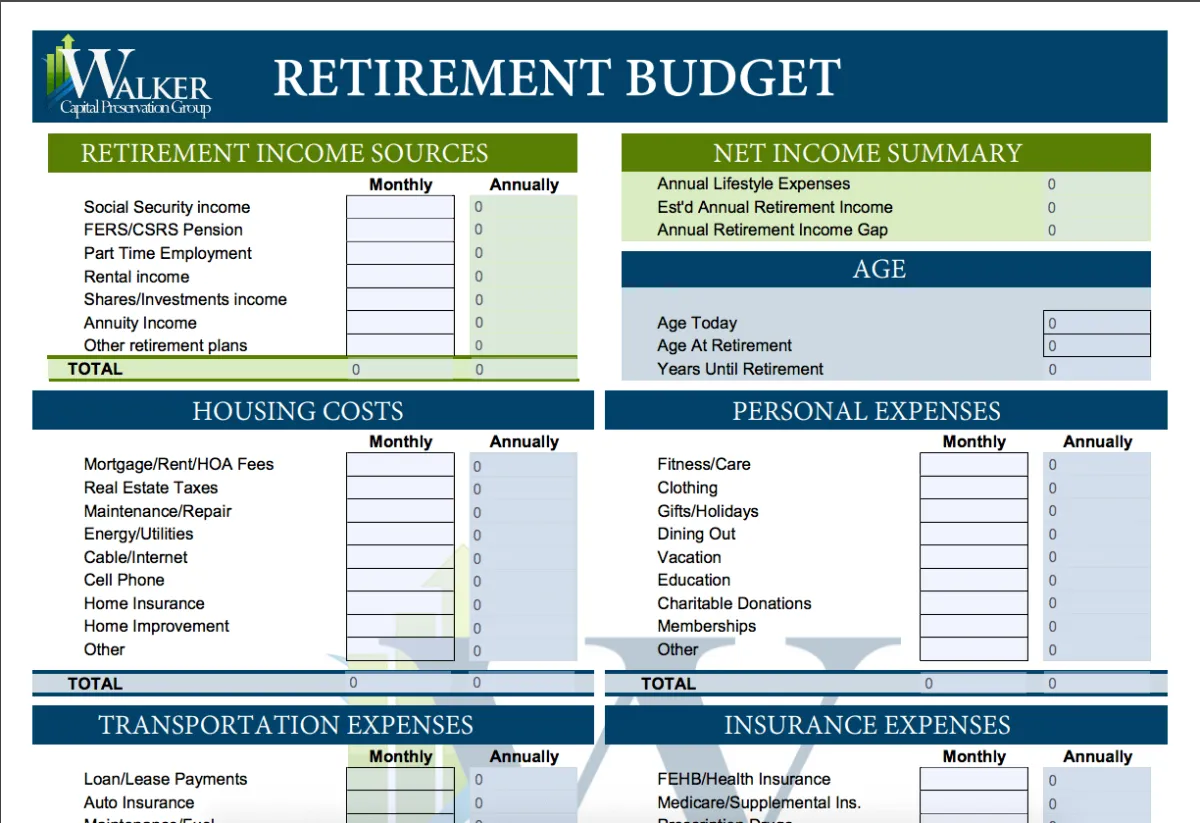

Creating a Retirement Budget

Retirement budgeting requires a thoughtful assessment of your anticipated income and expenses. It’s about understanding how much money you’ll need to maintain your desired lifestyle without a regular paycheck. Here’s a step-by-step approach:

1. Estimate Your Retirement Expenses

Begin by listing your current expenses and categorize them. Consider which expenses might decrease or increase during retirement. For example:

- Housing: Will you stay in your current home or downsize? Factor in property taxes, insurance, and potential maintenance costs.

- Healthcare: As you age, healthcare expenses tend to rise. Account for insurance premiums, deductibles, and potential out-of-pocket costs.

- Transportation: Will you continue driving or rely more on public transportation? Include car payments, insurance, gas, and maintenance or public transport costs.

- Food: Your eating habits may change in retirement. Estimate your grocery and dining out expenses.

- Leisure and Travel: Retirement can offer more time for hobbies, travel, and entertainment. Budget for these activities realistically.

2. Calculate Your Retirement Income

Identify your sources of income during retirement. This may include:

- Social Security: Visit the Social Security Administration website to get an estimate of your benefits.

- Pensions: If you have a pension plan, contact your plan provider for an estimate of your benefits.

- Retirement Savings: Determine how much you can withdraw annually from your 401(k), IRA, or other retirement accounts.

- Part-Time Work: Consider if you plan to work part-time and factor in that potential income.

3. Analyze and Adjust

Compare your estimated retirement expenses with your projected income. If your expenses exceed your income, you may need to consider:

- Reducing expenses: Identify areas where you can cut back.

- Delaying retirement: Working a few more years can significantly boost your savings and delay withdrawals.

- Increasing savings rate: If possible, contribute more to your retirement accounts while still employed.

4. Review and Revise Regularly

Your retirement budget is a living document. Review and adjust it annually or whenever significant life changes occur. Market fluctuations, inflation, and unexpected expenses can impact your financial plan.

Investing for Retirement

Investing is a crucial aspect of retirement planning. It allows you to grow your savings over time and potentially outpace inflation. Here are some key considerations for investing for retirement:

Start Early and Be Consistent

The earlier you start investing, the more time your money has to grow. Even small contributions made consistently over a long period can make a significant difference. Take advantage of compounding, where your earnings generate even more earnings over time.

Determine Your Risk Tolerance

Your risk tolerance refers to your ability to handle fluctuations in the value of your investments. Generally, younger investors have a longer time horizon and can afford to take on more risk, while older investors may prefer more conservative investments.

Choose the Right Investments

There are numerous investment options available, including stocks, bonds, and mutual funds. Diversify your portfolio by investing in a mix of asset classes to manage risk. Consider your time horizon, risk tolerance, and financial goals when making investment decisions.

Consider Retirement Accounts

Retirement accounts, such as 401(k)s and IRAs, offer tax advantages that can boost your savings. Contribute the maximum amount allowed to these accounts to maximize your tax benefits.

Regularly Review and Adjust

As you approach retirement, it’s important to review your investment portfolio and make adjustments as needed. Rebalance your portfolio to ensure it aligns with your changing risk tolerance and time horizon.

Understanding Social Security

Social Security is a crucial component of retirement planning for most Americans. It provides a foundation of income that you can generally rely on for the rest of your life. However, there are many misconceptions surrounding Social Security, and it’s essential to have a clear understanding of how it works to plan effectively.

How Social Security Works

Social Security is essentially a pay-as-you-go system. Your payroll taxes, along with your employer’s contributions, fund benefits for current retirees. When you retire, you’ll receive benefits based on your lifetime earnings. The more you earn (up to a certain limit), the higher your potential benefits.

Factors Affecting Your Benefits

Several factors influence how much you’ll receive from Social Security:

- Your Earnings History: Your benefit amount is calculated based on your 35 highest-earning years (adjusted for inflation).

- Your Full Retirement Age: This is the age at which you qualify for 100% of your calculated benefit amount. The full retirement age varies depending on your birth year.

- Claiming Age: You can start receiving benefits as early as age 62, but your benefits will be permanently reduced. Delaying your claim beyond your full retirement age can increase your benefits.

Why Understanding Social Security Matters for Retirement Planning

Having a clear picture of your potential Social Security benefits is essential for several reasons:

- Budgeting: Knowing how much you can expect from Social Security helps you create a realistic retirement budget.

- Savings Strategy: You can determine how much you need to save in other retirement accounts based on the gap between your expected expenses and your Social Security income.

- Claiming Strategy: Understanding how claiming age affects your benefits empowers you to make informed decisions about when to start receiving payments to maximize your lifetime income.

Managing Debt Before Retirement

Entering retirement with debt can add significant stress to your golden years. It’s important to prioritize debt management as part of your overall retirement planning strategy. Here’s how:

1. Create a Debt Reduction Plan

Start by listing all your debts, including mortgages, credit cards, loans, and any other outstanding payments. Note the interest rates, minimum payments, and loan terms for each. Prioritize your debts, focusing on high-interest ones first, as they accumulate faster and cost you more over time.

2. Explore Debt Consolidation

If you have multiple debts, consider consolidating them into one loan with a lower interest rate. This can simplify your payments and potentially save money on interest. A financial advisor can help you determine if debt consolidation is right for you.

3. Downsize and Cut Expenses

Look for ways to reduce your monthly expenses and free up cash flow to put towards debt repayment. Consider downsizing your home, selling a vehicle, or cutting back on discretionary spending.

4. Increase Your Income

Explore opportunities to boost your income, such as taking on a part-time job, freelancing, or monetizing a hobby. Directing extra earnings towards debt will accelerate your progress.

5. Negotiate with Creditors

Don’t hesitate to reach out to your creditors and explain your financial goals. They may be willing to work with you by lowering interest rates, reducing monthly payments, or creating a more manageable repayment plan.

Using Financial Tools

Managing your finances for retirement can feel like navigating a maze. Thankfully, numerous financial tools are available to illuminate the path. These tools can help you budget effectively, analyze investment opportunities, and make informed decisions about your financial future.

Budgeting and Expense Tracking:

Several apps and software programs can help you track your income and expenses. These tools often provide visualizations of your spending habits, allowing you to identify areas for potential savings.

Retirement Calculators:

These handy tools allow you to input your current financial information, estimated retirement expenses, and desired retirement age. The calculator then estimates how much you need to save and what rate of return you’ll need to achieve your retirement goals.

Investment Platforms:

From robo-advisors to online brokerage accounts, several platforms offer access to a wide range of investment options. These platforms often provide educational resources and tools to help you make informed investment decisions.

Financial Advisor Consultation:

While not strictly a “tool,” consulting with a certified financial advisor can provide invaluable guidance. An advisor can assess your financial situation, understand your goals, and develop a personalized financial plan. They can also provide ongoing support and advice as you navigate the complexities of retirement planning.

Reviewing and Adjusting Your Plan

Retirement planning isn’t a “set it and forget it” endeavor. As you move closer to retirement, and even during retirement itself, it’s crucial to regularly review and adjust your plan. Here’s why:

Factors That May Require Adjustments

- Changes in Your Life Situation: Marriage, divorce, the birth of grandchildren, health changes, or caring for aging parents can all impact your financial needs and goals.

- Market Volatility: Economic downturns and market fluctuations can affect your investment portfolio and retirement income projections.

- Inflation: The rising cost of living erodes purchasing power, so you’ll need to account for inflation when projecting future expenses.

- Longevity: People are living longer, which means your retirement savings might need to last for several decades.

- Changes to Social Security and Medicare: Staying informed about any potential changes to these programs is vital for planning your retirement income.

How Often to Review

A good rule of thumb is to review your retirement plan at least annually. However, more frequent reviews may be necessary during times of significant market volatility or life changes.

What to Review

- Retirement Goals: Have your retirement goals changed? Do you need to adjust your savings rate or retirement date?

- Investment Portfolio: Is your asset allocation still appropriate for your risk tolerance and time horizon?

- Withdrawal Strategy: How will you withdraw money from your retirement accounts in a tax-efficient manner?

- Estate Planning Documents: Are your will, power of attorney, and healthcare directive up to date?

Seeking Professional Guidance

Reviewing and adjusting your retirement plan can be complex. Consider working with a qualified financial advisor who can provide personalized advice and help you stay on track to meet your retirement goals.

Seeking Professional Advice

While there’s plenty of information available online, navigating the complexities of retirement planning can be daunting. That’s where seeking guidance from a qualified financial advisor can be invaluable.

A financial advisor can provide personalized advice tailored to your specific circumstances, including:

- Assessing your current financial situation and identifying areas for improvement.

- Developing a comprehensive retirement plan that aligns with your goals and risk tolerance.

- Recommending suitable investment strategies and managing your portfolio.

- Navigating complex financial products and regulations.

- Providing ongoing support and adjustments as your needs evolve.

When choosing a financial advisor, look for someone who is:

- Fiduciary: This means they are legally obligated to act in your best interests.

- Experienced: Choose an advisor with a proven track record in retirement planning.

- Certified: Look for credentials such as Certified Financial Planner (CFP).

- Trustworthy: You should feel comfortable communicating openly with your advisor.

Remember, seeking professional advice is an investment in your financial future. A qualified advisor can provide the guidance and support you need to retire comfortably and securely.

{kind=link}