Planning for retirement is essential for a secure future. Explore expert tips and advice on investments, savings, and financial strategies to ensure a comfortable retirement.

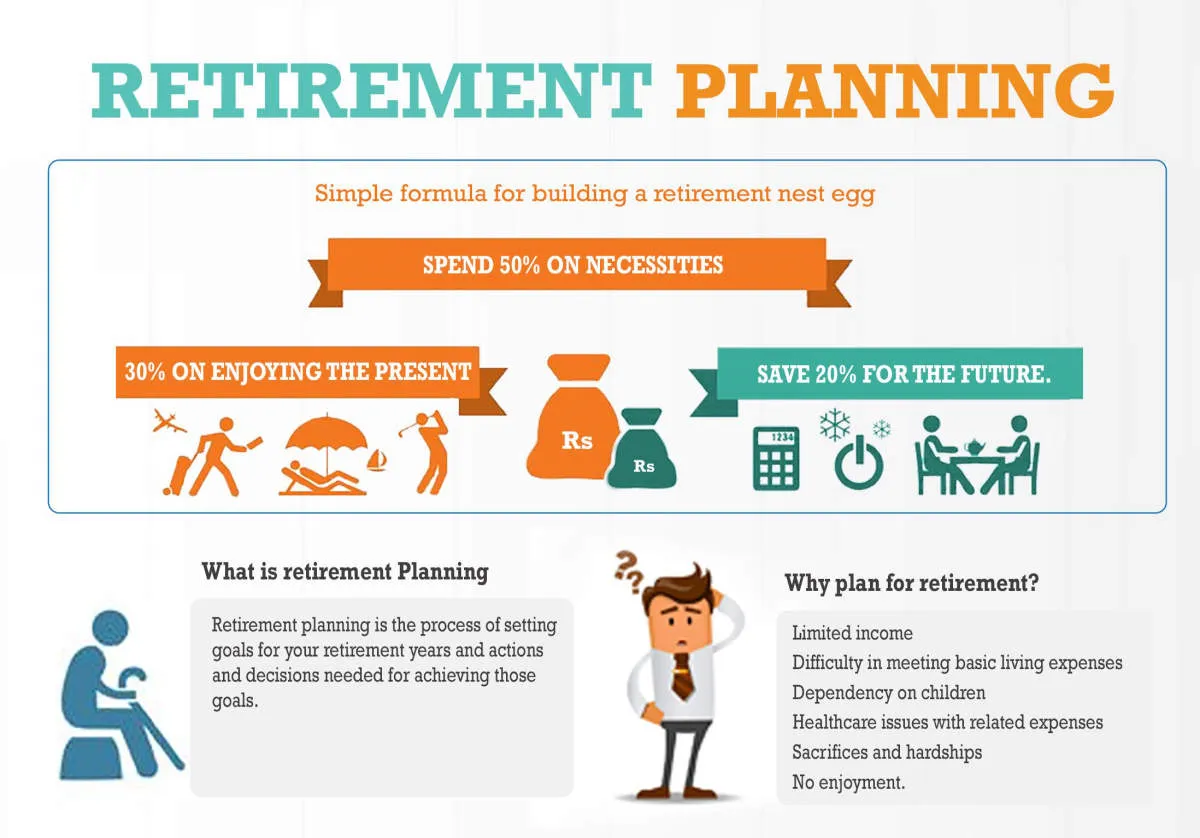

Setting Retirement Goals

Retirement might seem far off, but establishing clear goals today is crucial for a financially secure tomorrow. Without goals, it’s easy to underestimate how much money you’ll actually need and end up falling short.

Start by envisioning your ideal retirement lifestyle. Do you picture yourself traveling the world, pursuing hobbies, or spending time with loved ones? Consider these factors:

- Desired lifestyle: Will you be living modestly or indulging in more luxurious experiences?

- Health considerations: Factor in potential healthcare costs and long-term care needs.

- Living arrangements: Do you plan to stay in your current home, downsize, or relocate?

Once you have a clear vision, translate those aspirations into concrete financial goals. Determine how much annual income you’ll need to maintain your desired lifestyle. Don’t forget to account for inflation, which can significantly erode your purchasing power over time.

Having specific, measurable, achievable, relevant, and time-bound (SMART) goals will keep you motivated and provide a roadmap for your financial planning journey.

Understanding Retirement Accounts

Retirement accounts are specialized financial accounts designed to help you save and invest for your post-career years. They come with significant tax advantages and, in some cases, employer contributions, making them powerful tools for retirement planning. Here’s a breakdown of the most common types:

1. Employer-Sponsored Plans

These plans are offered through your employer and often come with valuable matching contributions.

- 401(k) Plans: Available to employees of for-profit companies. You contribute pre-tax dollars, lowering your current taxable income. Your investments grow tax-deferred, and you pay taxes when you withdraw funds in retirement.

- 403(b) Plans: Similar to 401(k)s but designed for employees of non-profit organizations, such as schools and hospitals.

- Thrift Savings Plan (TSP): A retirement savings and investment plan offered to federal employees and members of the uniformed services.

2. Individual Retirement Accounts (IRAs)

These accounts offer tax advantages for retirement savings and can be opened by anyone with earned income.

- Traditional IRA: Contributions may be tax-deductible, reducing your current tax liability. Your investments grow tax-deferred, and you pay taxes upon withdrawal in retirement.

- Roth IRA: Contributions are made with after-tax dollars, meaning you won’t receive an upfront tax deduction. However, your investments grow tax-free, and qualified withdrawals in retirement are tax-free.

3. Self-Employed Retirement Plans

If you’re self-employed or own a small business, several retirement plan options are available:

- Solo 401(k): Allows you to contribute as both an employee and an employer, potentially maximizing your contributions.

- SEP IRA: A simplified retirement plan for small business owners and self-employed individuals, allowing for larger contributions than a Traditional or Roth IRA.

- SIMPLE IRA: A savings incentive match plan for employees, typically used by small businesses with 100 or fewer employees.

Building an Emergency Fund

While retirement may seem far off, a crucial aspect of planning for it involves preparing for the unexpected today. An emergency fund acts as a financial cushion, protecting your long-term goals from being derailed by life’s inevitable surprises. Imagine facing a sudden job loss, medical emergency, or major home repair – without an emergency fund, you might be forced to dip into your retirement savings, derailing years of careful planning.

How much should you save? A good rule of thumb is to have three to six months’ worth of living expenses readily available. This ensures you can cover essential costs like rent or mortgage payments, utilities, groceries, and debt obligations for a period of time, providing financial stability and peace of mind.

Where should you keep your emergency fund? Accessibility is key. A high-yield savings account or money market account is typically the best place to store your emergency fund. These options offer easy access to your funds while still earning a modest amount of interest.

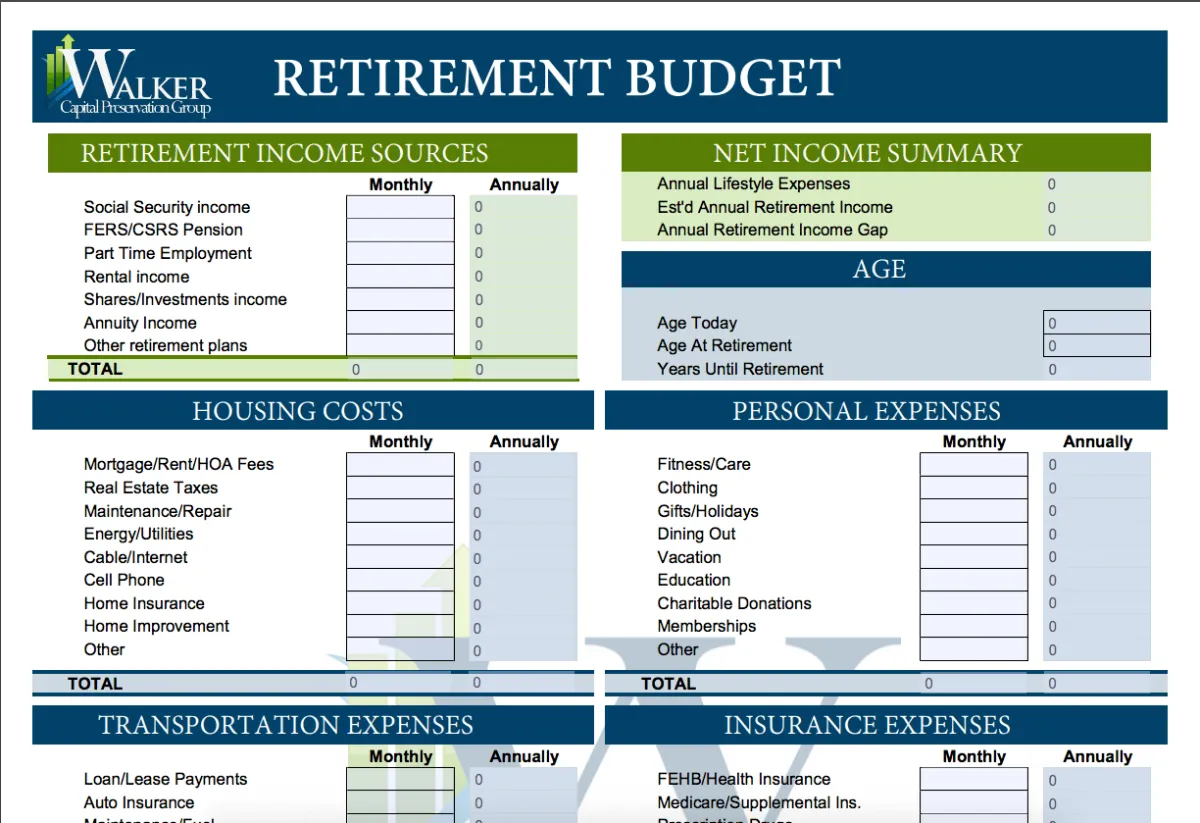

Creating a Retirement Budget

One of the most critical aspects of retirement planning is establishing a realistic budget that aligns with your desired lifestyle and financial resources. Retirement budgets differ significantly from working budgets because your income stream changes and you need to make your savings last for potentially several decades.

Here’s a step-by-step guide to creating your retirement budget:

1. Estimate Your Retirement Expenses

Start by outlining all your anticipated expenses in retirement. Consider these categories:

- Housing: Mortgage or rent, property taxes, insurance, maintenance

- Healthcare: Premiums, deductibles, out-of-pocket costs

- Living Expenses: Groceries, transportation, utilities, clothing

- Leisure & Travel: Hobbies, entertainment, vacations

- Debt Payments: Any outstanding loans or credit card balances

2. Factor in Inflation

The cost of goods and services generally increases over time due to inflation. It’s crucial to factor in an estimated inflation rate (historically around 3%) when projecting your retirement expenses. This means if something costs $100 today, in 10 years it might cost $134.

3. Determine Your Retirement Income Sources

List all your expected sources of income during retirement. Common sources include:

- Social Security benefits

- Pension payments

- Retirement account withdrawals (401(k), IRA)

- Part-time work or business income

- Investment income (dividends, interest)

4. Calculate Your Retirement Income Gap

Compare your estimated monthly/annual expenses (from Step 1 & 2) with your projected income sources (Step 3). If your expenses exceed your income, you have a retirement income gap. This gap needs to be addressed by increasing savings, reducing expenses, or delaying retirement.

5. Make Adjustments and Review Regularly

Creating a retirement budget is an ongoing process. Your needs and circumstances will likely change over time. Review and adjust your budget annually or as needed to reflect changes in your health, lifestyle, inflation, or market conditions.

Investing for Retirement

Investing is a cornerstone of retirement planning. It allows you to put your money to work by growing it over the long term, outpacing inflation and building a nest egg for your golden years.

Here’s what to consider when investing for retirement:

1. Start Early and Be Consistent

The power of compounding, where your earnings generate even more earnings, is maximized over time. The earlier you start investing, the more you benefit from this. Even small, consistent contributions can grow significantly over decades.

2. Determine Your Risk Tolerance

Your risk tolerance is your capacity to handle fluctuations in the value of your investments. Generally, younger investors can afford to take on more risk, as they have a longer time horizon to recover from potential losses. Older investors may prefer more conservative approaches to protect their accumulated savings.

3. Choose the Right Investments

There’s no one-size-fits-all approach to retirement investing. Consider these popular options:

- Retirement Accounts: Utilize tax-advantaged accounts like 401(k)s and IRAs to maximize your savings.

- Stocks: Offer potential for high growth but come with higher volatility.

- Bonds: Typically less risky than stocks, providing income and stability.

- Mutual Funds and ETFs: Offer instant diversification by pooling money from multiple investors to invest in a basket of assets.

- Real Estate: Can provide rental income and potential appreciation.

4. Diversify Your Portfolio

Don’t put all your eggs in one basket! Spreading your investments across different asset classes can help mitigate risk. If one investment performs poorly, others may cushion the blow.

5. Review and Adjust Regularly

As you move closer to retirement, your investment strategy might need adjustments. Rebalance your portfolio periodically to ensure it aligns with your risk tolerance and retirement goals. Life events like marriage, having children, or receiving an inheritance should also prompt a review of your plan.

Understanding Social Security

Social Security is a cornerstone of retirement planning for many Americans, providing a source of income after you stop working. It’s crucial to understand how Social Security works to plan effectively for your retirement. Here are key points to consider:

How Social Security Works

Social Security is a federal program funded through payroll taxes. When you work, you and your employer contribute a percentage of your earnings to the Social Security system. This money then funds benefits for current retirees, people with disabilities, and eligible survivors of deceased workers.

Eligibility for Benefits

To be eligible for Social Security retirement benefits, you generally need to have earned at least 40 “credits” throughout your working life. You earn credits based on your income, and you can earn a maximum of four credits per year.

When You Can Start Receiving Benefits

While you can start receiving Social Security retirement benefits as early as age 62, your benefits will be permanently reduced if you claim them before your full retirement age (FRA). Your FRA varies depending on your birth year. Waiting until after your FRA to claim benefits will result in a higher monthly payment.

Calculating Your Benefit Amount

Your Social Security benefit amount is based on your lifetime earnings history. The Social Security Administration (SSA) calculates your benefit using a formula that considers your 35 highest-earning years, adjusted for inflation. The higher your earnings, the higher your potential benefit.

Importance of Social Security Planning

Understanding how Social Security factors into your retirement income is essential. While Social Security can provide a foundation for your retirement income, it is rarely enough to cover all your expenses. Therefore, it’s crucial to explore other retirement savings options, such as 401(k)s, IRAs, and other investments, to supplement your Social Security benefits.

Managing Debt Before Retirement

Entering retirement with a significant amount of debt can put a strain on your finances and limit your options. Managing and minimizing debt before retirement is crucial for a secure and enjoyable post-work life. Here’s how:

1. Create a Debt Reduction Plan

Start by listing all your debts, including credit card balances, loans, and mortgages. Prioritize them based on interest rates or payoff timelines. Consider using strategies like the debt snowball method (paying off the smallest debts first) or the debt avalanche method (tackling high-interest debts first) to gain momentum.

2. Explore Debt Consolidation Options

If you have multiple debts with varying interest rates, consolidating them into a single loan with a lower rate can simplify payments and potentially save money on interest. Explore options like balance transfer credit cards or personal loans.

3. Negotiate with Creditors

Don’t hesitate to reach out to your creditors and try to negotiate lower interest rates or monthly payments. Explain your financial situation and retirement goals. They might be willing to work with you, especially if it means avoiding default.

4. Downsize and Cut Expenses

Consider downsizing your home or reducing unnecessary expenses to free up cash flow for debt repayment. Evaluate your spending habits and identify areas where you can cut back without drastically impacting your lifestyle.

5. Increase Your Income

Explore opportunities to supplement your income before retirement. This could involve taking on a part-time job, starting a side hustle, or finding ways to monetize your skills and hobbies. The extra income can be directed towards debt repayment.

6. Seek Professional Financial Advice

Consider consulting with a certified financial planner who can provide personalized guidance on debt management, retirement planning, and other financial matters. They can help you develop a comprehensive strategy tailored to your specific circumstances.

Using Financial Tools

Retirement planning can feel like navigating a maze, but luckily there are tools to illuminate the path. Utilizing the right financial tools is crucial to building a secure retirement. These resources can help you project future needs, make informed decisions about your savings, and manage your investments effectively.

Here are some essential tools to consider:

- Retirement Calculators: Freely available online, these calculators let you input your financial information, retirement goals, and projected expenses to estimate how much you need to save.

- Budgeting Apps: Understanding your cash flow is vital. Budgeting apps help track income and expenses, identify areas for saving, and ensure you’re on track to reach your retirement goals.

- Investment Tracking Tools: Whether you prefer hands-on management or robo-advisors, various platforms help monitor your investments, track performance, and make adjustments based on your risk tolerance and time horizon.

- Financial Advisor Consultations: Consider seeking guidance from a certified financial planner. They can provide personalized advice, create a comprehensive retirement plan, and offer expertise on investment strategies, tax optimization, and estate planning.

Reviewing and Adjusting Your Plan

Retirement planning isn’t a “set it and forget it” endeavor. As you move closer to retirement, and even during retirement itself, it’s crucial to periodically review and adjust your plan. Life is dynamic, and your financial plan needs to adapt to the changes.

Here’s what to consider during your reviews:

1. Life Events:

Major life events can significantly impact your financial situation and retirement goals. Marriage, divorce, the birth of a grandchild, unexpected home repairs, or caring for an elderly parent are just a few examples. When these events occur, reassess your retirement plan to ensure it aligns with your new circumstances.

2. Market Performance:

Market fluctuations are inevitable. Your investment portfolio’s performance will experience ups and downs. Regularly review your asset allocation and risk tolerance. If necessary, rebalance your portfolio to stay on track with your long-term goals.

3. Health and Longevity:

Healthcare costs and life expectancy are important factors. As you age, your healthcare expenses may increase. Additionally, consider the possibility of a longer lifespan than initially anticipated, which necessitates a larger retirement nest egg.

4. Inflation:

The purchasing power of money erodes over time due to inflation. Your retirement plan needs to account for this. Ensure your investments and savings are growing at a rate that outpaces inflation to maintain your living standards during retirement.

5. Withdrawal Strategy:

As you approach retirement, think about your withdrawal strategy. Determine how much you can safely withdraw from your savings each year to avoid outliving your assets. Consider consulting a financial advisor to develop a sustainable withdrawal plan.

Seeking Professional Advice

While there’s plenty of information available online, every individual’s financial situation is unique. Seeking guidance from a qualified financial advisor can be invaluable in creating a retirement plan tailored to your specific needs and goals.

Here’s why professional advice is crucial:

- Personalized Strategies: A financial advisor will assess your current assets, risk tolerance, retirement goals, and projected expenses to create a personalized roadmap.

- Investment Management: They can help you navigate the complexities of investment options, diversifying your portfolio for optimal growth potential while managing risk.

- Tax Optimization: Retirement income is taxed, and a financial advisor can help you implement strategies to minimize your tax burden, maximizing your after-tax income.

- Estate Planning: Planning for the distribution of your assets after your lifetime is a crucial part of retirement planning. An advisor can guide you through wills, trusts, and other estate planning tools.

- Ongoing Adjustments: Life throws curveballs. A financial advisor provides ongoing support, adjusting your plan as needed based on market fluctuations, life changes, and evolving goals.

Choosing the Right Advisor:

Look for a Certified Financial Planner (CFP) or a similar credential, indicating their expertise. Ask about their experience, fees, and communication style to ensure a good fit.

Conclusion

In conclusion, strategic retirement planning is essential for a secure future. By starting early, diversifying investments, and seeking professional advice, individuals can build a solid financial foundation for their retirement years.

{kind=link}