Learn important tips and strategies on how to effectively manage and reduce your credit card debt. Discover practical steps to take control of your finances and achieve financial freedom.

Understanding Credit Card Debt

Credit card debt is a type of revolving credit that allows you to borrow money up to a certain limit and make purchases on credit. It can be a convenient way to pay for things, but it’s important to use credit cards responsibly to avoid falling into debt.

When you use a credit card to make a purchase, you’re essentially borrowing money from the credit card issuer. You then have to repay the borrowed amount, plus any interest and fees that may apply. If you don’t pay off your balance in full each month, interest charges can accrue quickly, making it more difficult to get out of debt.

Factors that contribute to credit card debt:

- Overspending: It’s easy to overspend when you’re using a credit card because you’re not physically handing over cash.

- High Interest Rates: Credit cards typically have high-interest rates, which can make it costly to carry a balance.

- Minimum Payments: Making only the minimum payment each month can keep you in debt for years and result in significant interest charges.

- Unexpected Expenses: Emergencies and unexpected expenses can arise, leading to increased credit card use.

Understanding how credit card debt works, the factors contributing to its accumulation, and its potential impact is crucial for effective debt management and reduction.

Creating a Repayment Plan

Once you have a clear picture of your current credit card debt and spending habits, it’s time to create a realistic repayment plan. This plan will serve as your roadmap to becoming debt-free and should outline how you’ll allocate your finances to pay down your balances strategically. Here’s a step-by-step guide to creating an effective repayment plan:

1. Prioritize Your Debts

List all your credit cards, noting the outstanding balance, interest rate, and minimum payment for each. There are two main strategies for prioritization:

- Avalanche Method: Focus on paying down the card with the highest interest rate first, while making minimum payments on all others. This approach saves you the most money on interest charges in the long run.

- Snowball Method: Start by paying off the card with the smallest balance first, regardless of the interest rate, while maintaining minimum payments on the rest. This method provides quicker wins and motivation, as you see debts disappear faster.

Choose the strategy that best suits your personality and financial goals.

2. Explore Debt Consolidation Options

If you have multiple high-interest credit cards, consider consolidating your debt. This involves taking out a new loan with a lower interest rate and using it to pay off your existing credit card balances. Debt consolidation can simplify your payments and potentially save you money on interest. Options include:

- Balance Transfer Credit Cards: These cards offer a promotional period with 0% APR, allowing you to transfer your balances and pay them down without accruing interest for a specific time.

- Personal Loans: These loans typically come with lower interest rates than credit cards and offer fixed monthly payments, making budgeting easier.

Carefully research the terms and fees associated with each option before making a decision.

3. Negotiate with Your Credit Card Issuers

Don’t hesitate to contact your credit card companies and negotiate for better terms. Explain your financial situation and ask if they can lower your interest rates or waive certain fees. Many creditors are willing to work with you to find a solution, especially if you have a good payment history.

4. Create a Realistic Budget

Developing a detailed budget is crucial for successful debt repayment. Track your income and expenses meticulously, identifying areas where you can cut back on spending and allocate more money toward your credit card bills. Consider using budgeting apps or spreadsheets to help you stay organized.

5. Set Up Payment Reminders

Avoid late payment fees and potential damage to your credit score by setting up payment reminders. Most credit card issuers offer email or text message alerts, or you can use a budgeting app or online calendar to remind yourself when payments are due.

6. Automate Your Payments

Consider automating your credit card payments to ensure timely payment and avoid late fees. You can typically set up automatic payments through your online banking portal or credit card account. Choose to pay the minimum amount due or a fixed amount that aligns with your budget and repayment goals.

Reducing Interest Rates

High interest rates are a major contributor to growing credit card debt. Lowering your interest rate can help you save money and get out of debt faster. Here are some strategies to consider:

Negotiate with Your Credit Card Issuer

Believe it or not, your credit card company might be willing to lower your interest rate if you simply ask. Call them up, explain your financial situation, and inquire about the possibility of a lower rate. Be polite but persistent.

Transfer Your Balance

Consider transferring your balance to a credit card with a lower interest rate. Many cards offer 0% introductory APR periods for balance transfers, giving you a window of time to pay down debt interest-free. Be mindful of any balance transfer fees, and make sure to read the terms and conditions carefully.

Look for Credit Card Offers with Lower APRs

Keep an eye out for credit card offers that advertise low APRs, especially if you have good credit. Switching to a card with a more favorable interest rate can make a significant difference in your long-term debt repayment.

Consider a Debt Consolidation Loan

If you have good credit, you might qualify for a debt consolidation loan with a lower interest rate than your credit cards. This allows you to combine multiple debts into one monthly payment, potentially saving you money on interest charges.

Consolidating Your Debt

Debt consolidation is a strategy to simplify debt repayment by combining multiple debts into one new loan with a potentially lower interest rate. This can be a good option for managing credit card debt, especially if you have several high-interest cards.

Types of Debt Consolidation:

- Balance Transfer Credit Cards: These cards offer a low or 0% introductory APR for a set period, allowing you to transfer balances from high-interest cards and save on interest charges.

- Personal Loans: You can use a personal loan to pay off multiple credit cards and consolidate the debt into one monthly payment. Look for loans with lower interest rates than your current credit cards.

- Home Equity Loans or Lines of Credit: If you’re a homeowner, you might consider tapping into your home equity. However, this option uses your home as collateral, meaning you could risk foreclosure if you fail to repay the loan.

Benefits of Debt Consolidation:

- Simplified Repayment: Instead of juggling multiple payments, you’ll have one monthly payment.

- Potential Interest Savings: Consolidating to a lower interest rate can save you money over the life of the loan.

- Improved Credit Score: Consolidating and managing debt responsibly can lower your credit utilization ratio, potentially boosting your credit score over time.

Considerations Before Consolidating:

- Fees: Some consolidation methods come with fees, such as balance transfer fees or loan origination fees. Factor these costs into your decision.

- Interest Rates: Ensure the new interest rate is lower than your existing rates to achieve savings.

- Repayment Terms: Understand the new loan’s repayment period and monthly payment amount. A longer term might have lower payments but could mean paying more interest overall.

Using Balance Transfer Offers

A balance transfer can be a powerful tool to reduce your credit card debt faster. This involves moving your existing debt from one credit card to another that offers a lower interest rate, often as an introductory 0% APR period.

Here’s how balance transfers can help:

- Reduced Interest Payments: A lower interest rate means more of your monthly payment goes towards paying down the principal balance, rather than just interest.

- Faster Debt Payoff: With less interest accruing, you can potentially eliminate your debt faster.

- Simplified Finances: Consolidating multiple credit card balances onto one card can streamline your finances, making it easier to track payments and due dates.

Things to consider before opting for a balance transfer:

- Balance Transfer Fees: Most balance transfer cards charge a fee, typically a percentage of the amount you’re transferring (e.g., 3% or 5%). Factor this fee into your calculations to ensure the savings outweigh the cost.

- Introductory Period Length: 0% APR offers are usually temporary. Make note of the introductory period’s duration and plan to pay off as much debt as possible before the regular interest rate kicks in.

- Credit Score Requirements: Balance transfer offers with the best terms are often reserved for applicants with good to excellent credit scores.

Avoiding New Debt

While you’re working hard to pay down your existing credit card balances, it’s crucial to avoid accumulating new debt. Here are some strategies to help you steer clear of falling back into the credit card trap:

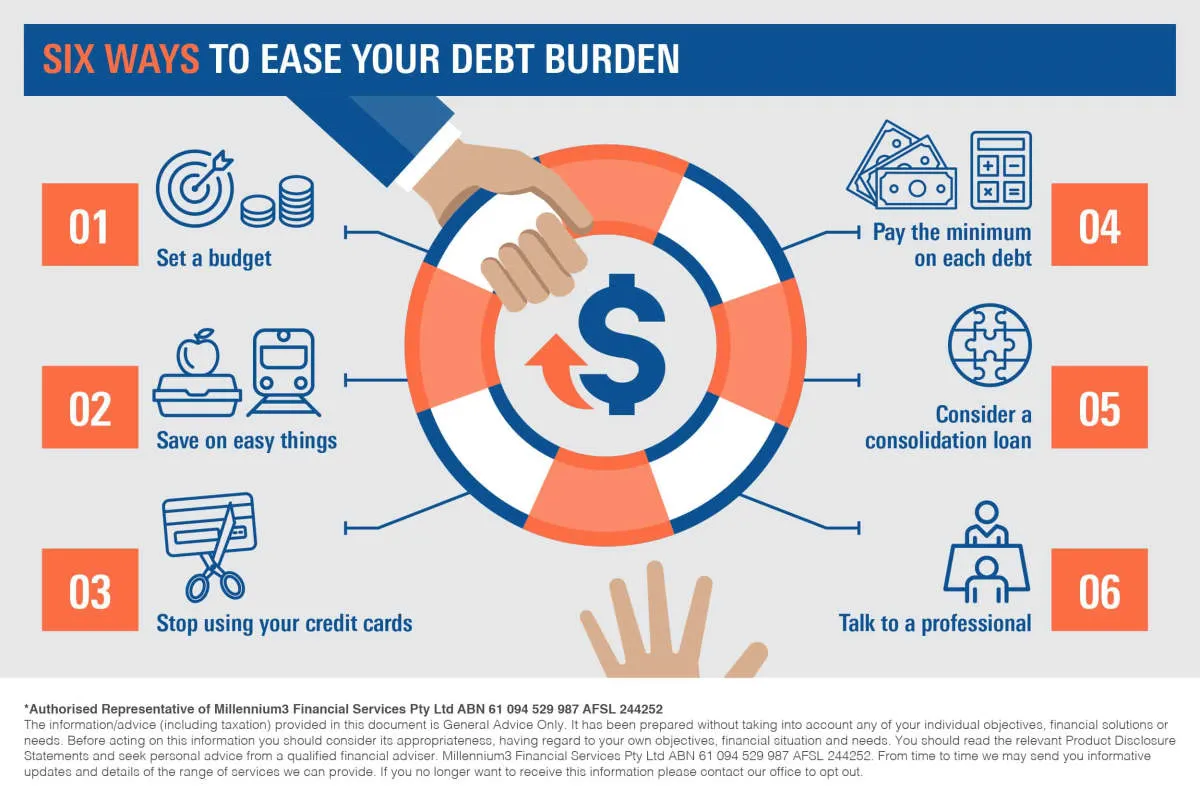

1. Create a Budget and Stick to It

One of the most effective ways to avoid new debt is to create a realistic budget that tracks your income and expenses. Identify areas where you can cut back on unnecessary spending and allocate those funds towards debt repayment or savings. Track your spending diligently to ensure you’re staying within your budget limits.

2. Build an Emergency Fund

Unexpected expenses, like medical bills or car repairs, can quickly derail your progress in becoming debt-free. Establish an emergency fund to cover these unforeseen costs without relying on credit cards. Aim to save three to six months’ worth of living expenses.

3. Use Cash or Debit Cards

Credit cards can make it easy to overspend, as you’re not directly seeing the money leave your account. Switch to using cash or debit cards for everyday purchases. This will help you stay conscious of your spending and prevent you from accumulating new debt.

4. Resist Impulse Purchases

Before making a purchase, especially a large one, take some time to consider if it’s truly necessary. Ask yourself if it aligns with your budget and financial goals. Often, delaying a purchase for a few days or weeks can help you avoid impulsive spending decisions.

5. Explore Alternative Financing Options

If you’re facing a large expense, research alternative financing options instead of immediately turning to credit cards. Explore options like personal loans, borrowing from family or friends, or using savings. Carefully compare interest rates and terms to make an informed decision.

6. Seek Professional Financial Guidance

If you’re struggling to manage your debt or avoid new spending, consider seeking guidance from a financial advisor. They can provide personalized advice, help you create a debt management plan, and offer strategies for achieving your financial goals.

Building an Emergency Fund

One of the most effective ways to avoid credit card debt (and dig yourself out if you’re already in it) is to have a financial safety net. An emergency fund is a savings account specifically for unexpected expenses or financial hardships such as:

- Job loss

- Medical bills

- Car repairs

- Home repairs

Having this fund acts as a buffer, preventing you from relying on credit cards to cover these costs. Without this safety net, unexpected events can quickly derail your finances and lead to increased debt.

How much should you save?

Ideally, your emergency fund should cover 3-6 months’ worth of living expenses. This may seem like a daunting amount, but start small. Even setting aside $50 a month is a step in the right direction.

Where should you keep your emergency fund?

It’s important to keep your emergency fund separate from your everyday spending account. This will help you avoid accidentally spending it. Consider a high-yield savings account, which typically offers a higher interest rate than a traditional savings account.

Prioritize your emergency fund

While paying down debt is crucial, it’s essential to strike a balance between debt repayment and building an emergency fund. If you don’t have any emergency savings, allocate a small portion of your budget towards building a starter fund before focusing solely on aggressive debt repayment.

Increasing Your Income

While creating a budget and cutting expenses are crucial for debt management, increasing your income can significantly accelerate the debt payoff process. Here’s how you can explore ways to boost your earnings:

1. Negotiate a Raise or Promotion:

Assess your current job performance, skills, and market value. If you’ve consistently exceeded expectations and gained valuable experience, don’t hesitate to negotiate a raise or explore opportunities for promotion within your company.

2. Seek Additional Income Streams:

Consider these options for supplementing your income:

- Freelancing: Utilize your skills in writing, editing, graphic design, web development, or other fields to offer freelance services.

- Gig Economy: Platforms like Uber, Lyft, DoorDash, and TaskRabbit offer flexible gig opportunities that fit your schedule.

- Online Surveys and Microtasks: While not highly lucrative, websites and apps that offer paid surveys and microtasks can provide a small income stream.

- Selling Unused Items: Declutter your home and sell unwanted clothing, electronics, or furniture online or at consignment shops.

3. Develop New Skills:

Investing in your education and acquiring new skills can open doors to higher-paying jobs or freelance opportunities. Consider online courses, workshops, or certifications in in-demand fields.

Using Financial Tools

Managing and reducing credit card debt often feels overwhelming, but numerous financial tools can provide structure and support your journey back to financial freedom. Here are some powerful options:

1. Budgeting Apps and Software:

These tools provide a clear picture of your income and expenses, helping you identify areas to cut back and free up money for debt repayment. Many apps offer features like expense tracking, budget creation, and goal setting, making it easier to stay organized and motivated.

2. Debt Consolidation Loans:

If you have multiple high-interest credit cards, consolidating them into a single loan with a lower interest rate can simplify payments and potentially save money on interest charges. This strategy can also accelerate your debt payoff timeline.

3. Balance Transfer Credit Cards:

These cards offer a promotional period with 0% APR, allowing you to transfer your existing balance and pay it down without accruing interest. Capitalizing on this introductory period can significantly reduce the overall cost of your debt.

4. Credit Counseling Agencies:

Non-profit credit counseling agencies provide guidance and support to individuals struggling with debt. They can help you create a personalized debt management plan, negotiate with creditors for lower interest rates or waived fees, and provide financial education resources.

5. Debt Snowball or Avalanche Method:

These popular debt repayment strategies provide frameworks for prioritizing and tackling your debts. The Debt Snowball method focuses on paying off the smallest debt first for motivation, while the Debt Avalanche method prioritizes high-interest debts to save money.

Remember to carefully research and compare different financial tools to determine which options best suit your individual circumstances and financial goals.

Seeking Professional Advice

Sometimes, managing credit card debt on your own can feel overwhelming. If you’re struggling to make progress, or if your debt feels unmanageable, seeking help from a professional is a smart move. Here are some experts who can provide guidance:

Credit Counselors

Non-profit credit counseling agencies offer a range of services, including:

- Budget Analysis: They’ll review your income and expenses to identify areas where you can cut back and free up more money to put towards debt.

- Debt Management Plans (DMPs): A DMP consolidates your debts and negotiates with your creditors for lower interest rates and waived fees. You make one monthly payment to the agency, and they distribute it to your creditors.

- Financial Education: Counselors can teach you about budgeting, saving, and responsible credit use.

Financial Advisors

While not all financial advisors specialize in debt management, they can offer personalized advice on your overall financial situation, including strategies for tackling debt, investing, and planning for the future.

Debt Relief Companies

Be cautious when considering debt relief companies. These for-profit companies negotiate with your creditors to try to reduce your debt, but they often charge high fees. Research thoroughly and understand all costs before signing up.

Conclusion

In conclusion, managing and reducing credit card debt requires discipline, budgeting, and consistent payments. By implementing effective strategies and seeking assistance when needed, individuals can take control of their finances and work towards a debt-free future.

{kind=link}