In the quest for financial stability, implementing effective strategies for personal financial management is crucial. This article delves into practical tips and techniques to maximize savings, budgeting, and investment for a secure financial future.

Creating a Financial Plan

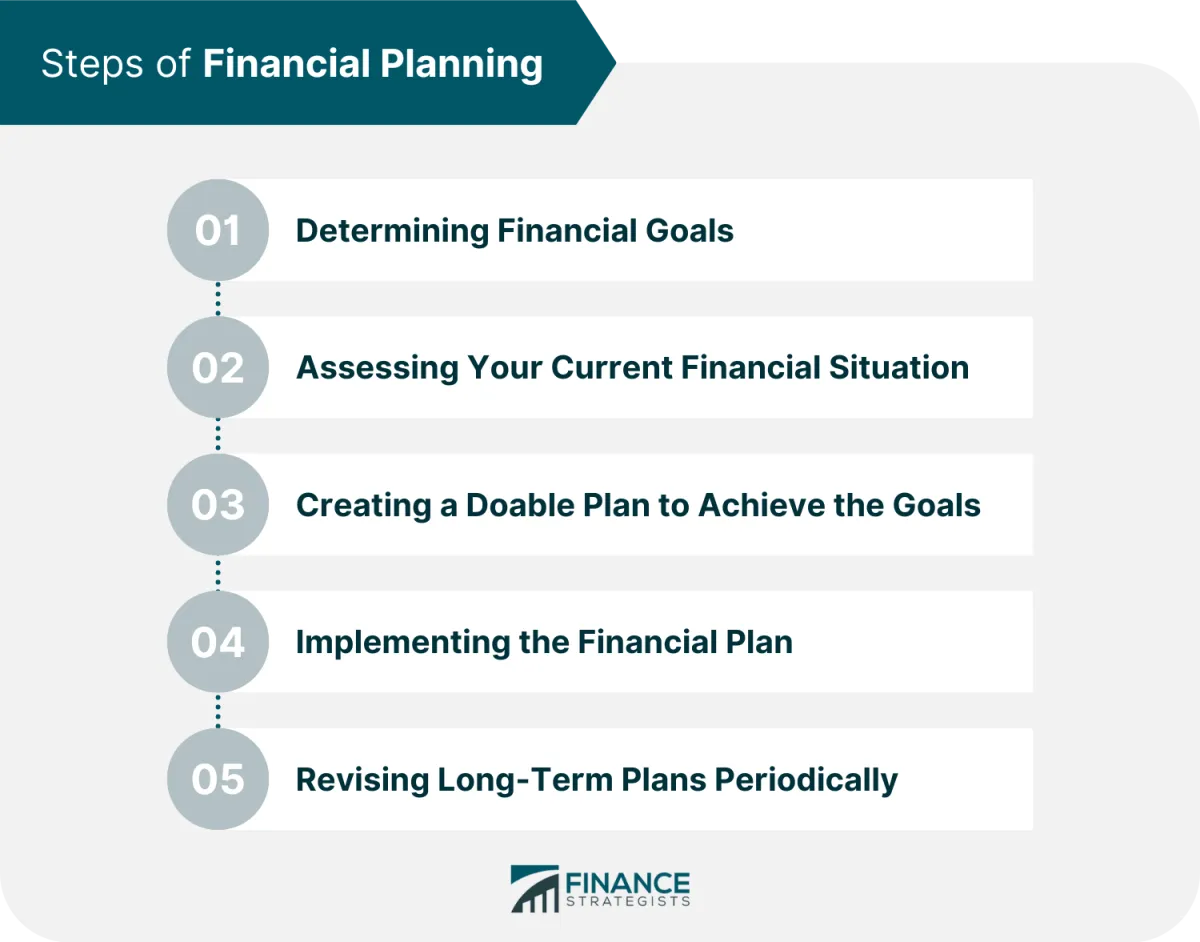

A comprehensive financial plan serves as a roadmap to achieving your financial goals. It provides a structured approach to managing your money, allowing you to make informed decisions and stay on track towards financial security.

Steps to Create a Financial Plan:

- Assess Your Current Financial Situation: Begin by gathering information about your income, expenses, assets, and liabilities. Calculate your net worth and cash flow to understand your financial standing.

- Set SMART Financial Goals: Define your short-term and long-term financial objectives. Ensure your goals are Specific, Measurable, Achievable, Relevant, and Time-bound.

- Develop a Budget: Track your income and expenses to identify areas where you can save and allocate funds effectively. Create a realistic budget that aligns with your financial goals.

- Manage Debt: Develop a strategy to manage and reduce existing debt. Prioritize high-interest debts and explore options such as debt consolidation or balance transfers.

- Establish an Emergency Fund: Set aside three to six months’ worth of living expenses in a readily accessible account to cover unexpected events like job loss or medical emergencies.

- Invest for the Future: Determine your investment goals and risk tolerance. Explore different investment options such as stocks, bonds, mutual funds, and real estate to grow your wealth over time.

- Plan for Retirement: Estimate your retirement expenses and determine how much you need to save. Contribute regularly to retirement accounts like 401(k)s or IRAs.

- Review and Adjust Regularly: Your financial plan should evolve as your circumstances change. Review and update it annually or whenever you experience significant life events.

Managing Cash Flow

Managing cash flow effectively is crucial for maintaining a healthy financial life. It involves understanding your income, tracking your expenses, and making adjustments to ensure you have enough money to cover your needs and goals.

1. Tracking Income and Expenses

Start by creating a budget to track where your money is coming from and where it’s going. You can use a spreadsheet, budgeting apps, or even a simple notebook. Be sure to include all sources of income and categorize your expenses for a clearer picture.

2. Differentiating Needs vs. Wants

Analyze your spending habits and differentiate between needs and wants. Needs are essential expenses like housing, food, and utilities, while wants are things you desire but can live without, like entertainment or dining out. Prioritizing needs over wants can free up significant cash flow.

3. Building an Emergency Fund

Unexpected expenses can arise at any time. Having an emergency fund with 3-6 months’ worth of living expenses can prevent you from going into debt when facing unexpected situations like job loss or medical emergencies.

4. Exploring Ways to Increase Income

Consider exploring ways to increase your income streams. This could involve asking for a raise, taking on a side hustle, or finding ways to monetize your hobbies. Increasing your income can provide more financial flexibility and help you reach your goals faster.

5. Reviewing and Adjusting Regularly

Financial situations can change, so it’s essential to review your cash flow regularly. Make adjustments to your budget as needed, track your progress, and celebrate small victories along the way.

Reducing Expenses

One of the most effective ways to gain control of your personal finances is to reduce your expenses. This doesn’t necessarily mean living a life of deprivation, but rather making conscious decisions about where your money goes and identifying areas where you can cut back without sacrificing your quality of life. Here are some practical strategies:

1. Track Your Spending

You can’t manage what you don’t measure. Start by tracking your expenses for at least a month, noting down every dollar you spend. You can use a spreadsheet, budgeting apps, or even a simple notebook. This will give you a clear picture of your spending habits and highlight areas where you can potentially save.

2. Differentiate Between Needs and Wants

Analyze your spending tracker and categorize each expense as either a need or a want. Needs are essentials like housing, groceries, and transportation, while wants are things you desire but can live without, like entertainment, dining out, or luxury items. Be honest with yourself and identify wants that you can reduce or eliminate.

3. Create a Realistic Budget

Based on your spending analysis and needs vs. wants assessment, create a practical and detailed budget. Allocate funds for essential expenses first and then determine how much you can realistically allocate to wants without overspending. A budget serves as a roadmap for your financial goals.

4. Explore Cost-Cutting Measures

There are numerous ways to cut expenses without drastically impacting your lifestyle. Consider these strategies:

- Negotiate Bills: Contact service providers for internet, cable, and insurance to negotiate better rates or explore more affordable alternatives.

- Reduce Energy Consumption: Lower your electricity and water bills by being mindful of usage. Unplug unused appliances, switch to energy-efficient bulbs, and take shorter showers.

- Shop Smart: Compare prices, use coupons, and look for sales and discounts on groceries, clothing, and other purchases. Consider buying generic brands when applicable.

- Limit Dining Out: Eating out frequently can be costly. Explore cooking more meals at home and packing lunches instead.

- Find Free or Low-Cost Entertainment: Explore free or inexpensive entertainment options like parks, museums, libraries, or community events instead of expensive outings.

5. Review and Adjust Regularly

Your financial situation and needs can change over time, so it’s crucial to review your budget and expenses regularly. Make adjustments as needed to ensure you stay on track with your financial goals.

Investing for the Future

Investing is a crucial aspect of personal financial management that focuses on growing your wealth over time. It involves putting your money to work in assets that have the potential to generate returns and outpace inflation. By investing wisely, you can secure your financial future and work towards your long-term financial goals, such as retirement or buying a home.

Here are key considerations for investing for the future:

1. Define Your Financial Goals:

Before investing, identify your short-term and long-term financial objectives. Are you saving for retirement, a down payment on a house, or your child’s education? Defining your goals will help determine your investment timeline and risk tolerance.

2. Understand Your Risk Tolerance:

Risk tolerance refers to your ability to withstand fluctuations in the value of your investments. Younger investors with a longer time horizon may be comfortable with higher-risk investments, while older individuals nearing retirement may prefer more conservative options.

3. Diversify Your Investments:

Don’t put all your eggs in one basket. Diversifying your portfolio by investing in a mix of asset classes, such as stocks, bonds, and real estate, can help mitigate risk. When one asset class is performing poorly, others may cushion the impact.

4. Start Early and Be Consistent:

The power of compounding is significant in investing. Starting early allows your investments more time to grow, and even small, consistent contributions can accumulate substantial returns over time.

5. Consider Retirement Accounts:

Employer-sponsored retirement plans, such as 401(k)s, and individual retirement accounts (IRAs), offer tax advantages and can help you save for retirement effectively.

6. Seek Professional Advice:

If you’re unsure about investing or need personalized guidance, consult with a qualified financial advisor who can assess your financial situation, goals, and risk tolerance to provide tailored recommendations.

Using Financial Tools

Managing your personal finances effectively goes beyond basic budgeting. Leveraging financial tools can significantly enhance your ability to track, analyze, and optimize your financial decisions. Here are some essential tools to consider:

1. Budgeting Apps and Software

These tools have revolutionized personal finance management. They allow you to:

- Create and track budgets effortlessly

- Monitor your income and expenses across multiple accounts

- Set financial goals and track your progress

- Receive personalized insights and recommendations

Popular options include Mint, Personal Capital, YNAB (You Need a Budget), and EveryDollar.

2. Expense Tracking Tools

If you prefer a more focused approach to managing expenses, expense tracking apps can be beneficial. They help you:

- Log your spending on the go

- Categorize expenses for better analysis

- Set spending limits and receive alerts

Consider using apps like Expensify, PocketGuard, or Spending Tracker.

3. Investment Platforms

For those looking to grow their wealth, online investment platforms offer accessibility and convenience. They provide:

- Access to a wide range of investment options (stocks, bonds, mutual funds, ETFs)

- Portfolio tracking and analysis tools

- Educational resources and research

- Automated investing features (robo-advisors)

Popular platforms include Fidelity, Vanguard, Charles Schwab, and Robinhood.

4. Credit Monitoring Services

Protecting your credit score is crucial for financial well-being. Credit monitoring services offer:

- Regular updates on your credit reports from major credit bureaus

- Alerts for suspicious activity or potential fraud

- Tools for understanding and improving your credit score

Reputable options include Credit Karma, Experian CreditWorks, and myFICO.

5. Financial Calculators

Various online financial calculators can assist you with specific financial decisions, such as:

- Mortgage calculators

- Retirement planning calculators

- Loan amortization calculators

- College savings calculators

These calculators simplify complex financial projections and help you make informed choices. Many financial websites and reputable financial planning resources offer free financial calculators.

Reviewing Financial Statements

Reviewing your financial statements is a crucial aspect of effective personal financial management. It provides valuable insights into your financial health, enabling you to make informed decisions about your money. Here’s a breakdown of the key financial statements and how to review them:

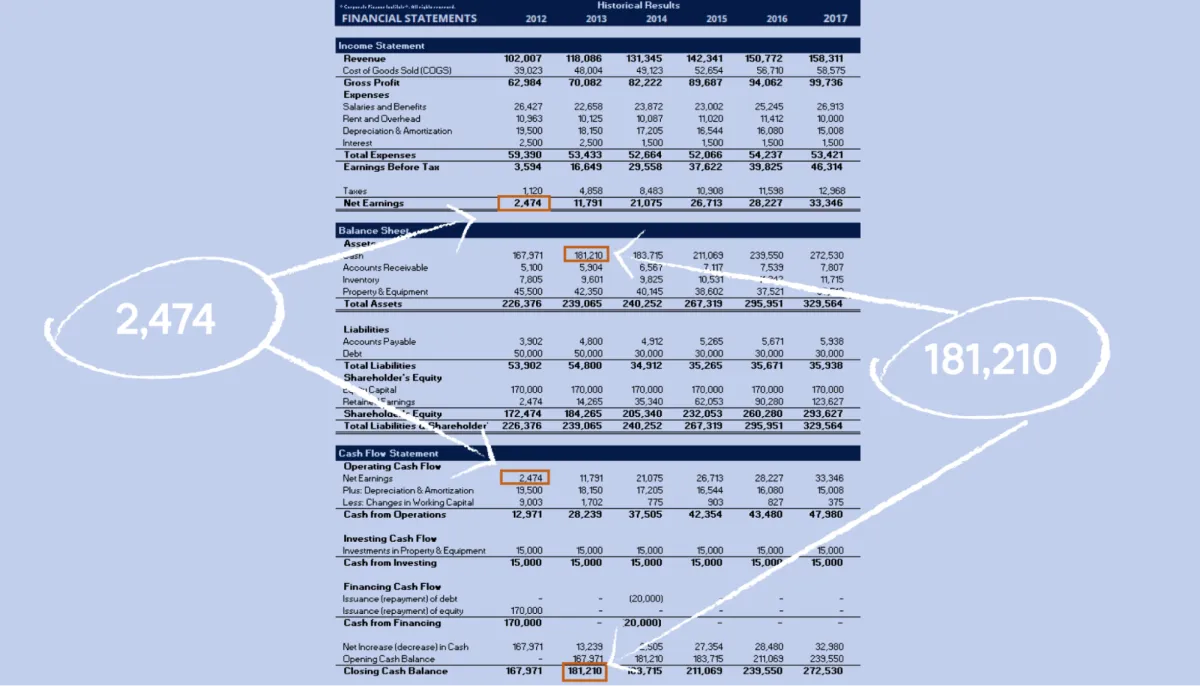

1. Personal Balance Sheet (Net Worth Statement)

Your balance sheet provides a snapshot of your financial position at a specific point in time. It consists of three main components:

- Assets: What you own (e.g., cash, investments, property)

- Liabilities: What you owe (e.g., loans, credit card debt)

- Net Worth: The difference between your assets and liabilities (Assets – Liabilities = Net Worth)

Review your balance sheet regularly to track changes in your net worth over time. An increasing net worth indicates financial progress, while a decreasing net worth may signal potential issues to address.

2. Income Statement (Profit and Loss Statement)

Your income statement summarizes your income and expenses over a specific period, such as a month or a year. It reveals:

- Income: Money coming in (e.g., salary, investments, side hustles)

- Expenses: Money going out (e.g., rent, groceries, utilities)

- Net Income: The difference between your income and expenses (Income – Expenses = Net Income)

Analyzing your income statement helps you understand your spending patterns, identify areas for improvement, and track your progress toward financial goals.

3. Cash Flow Statement

Your cash flow statement tracks the movement of cash both into and out of your accounts over a period. It highlights:

- Operating Cash Flow: Cash generated from your primary activities (e.g., salary, business income)

- Investing Cash Flow: Cash used for investments or generated from selling investments

- Financing Cash Flow: Cash related to borrowing or repaying debt

Monitoring your cash flow statement is essential for ensuring you have enough liquidity to meet short-term obligations and make informed financial decisions.

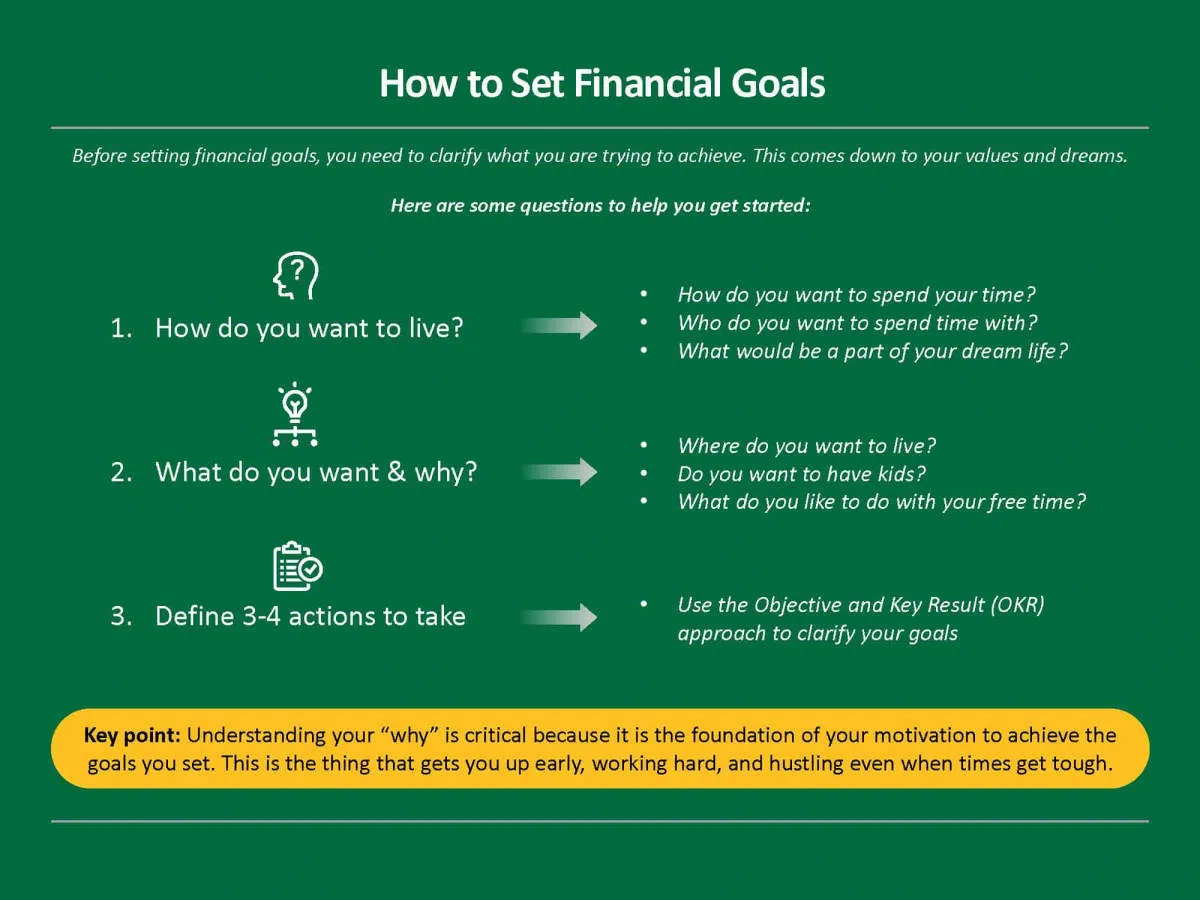

Setting Financial Goals

Setting clear and specific financial goals is the crucial first step in effective personal financial management. These goals provide a roadmap for your finances and motivate you to make sound financial decisions.

Identify Your Goals: Start by determining what matters most to you financially. Your goals might include:

- Building an emergency fund

- Saving for a down payment on a home

- Investing for retirement

- Paying off debt (credit cards, student loans, etc.)

- Funding your children’s education

- Traveling

Make Goals SMART: Ensure your financial goals are SMART:

- Specific: Clearly define each goal (e.g., “Save $10,000 for a down payment”).

- Measurable: Quantify your goals (e.g., “Save $500 per month”).

- Achievable: Set realistic goals within your means.

- Relevant: Align your goals with your values and priorities.

- Time-Bound: Establish a target date for achieving each goal.

Prioritize Your Goals: It’s unlikely you can achieve all your financial goals simultaneously. Prioritize them based on their importance to you and tackle them strategically.

Write Down Your Goals: The act of writing down your goals makes them more tangible and increases your commitment to achieving them.

Review and Adjust: Regularly review your financial goals, at least annually or when your circumstances change. Adjust your savings and spending plans as needed to stay on track.

Building an Emergency Fund

An emergency fund is a safety net of money set aside to cover unexpected expenses or financial hardships. This could include job loss, medical emergencies, car repairs, or unexpected home repairs.

Why is an Emergency Fund Important?

Having an emergency fund provides a financial cushion to help you navigate unexpected events without going into debt. It provides peace of mind and financial security knowing you can handle most unexpected financial challenges. Without an emergency fund, you might be forced to rely on credit cards or loans, potentially leading to a cycle of debt.

How Much Should You Save?

A good rule of thumb is to have three to six months’ worth of living expenses saved in your emergency fund. This ensures you have enough to cover your essential needs for a period if your income is interrupted.

How to Build Your Emergency Fund:

- Create a Budget: Track your income and expenses to identify areas where you can cut back and save more effectively.

- Set Realistic Savings Goals: Start small and gradually increase your savings rate as you become more comfortable.

- Automate Your Savings: Set up automatic transfers from your checking account to your emergency fund each month.

- Find Ways to Boost Your Income: Consider a side hustle, selling unwanted items, or finding ways to increase your income.

Where to Keep Your Emergency Fund:

It is best to keep your emergency fund in a separate, easily accessible account, such as a high-yield savings account or money market account.

Seeking Professional Advice

While there are many resources available to help you manage your finances independently, sometimes seeking professional advice can provide invaluable support and expertise. Financial advisors can provide personalized guidance tailored to your specific financial situation, goals, and risk tolerance.

Here are some instances where seeking professional advice can be particularly beneficial:

- Complex financial situations: If you have a complex financial situation, such as significant investments, multiple income streams, or estate planning needs, a financial advisor can help you navigate these complexities effectively.

- Major life changes: Life events like marriage, divorce, the birth of a child, or retirement often come with significant financial implications. A financial advisor can help you adjust your financial plan accordingly.

- Lack of time or expertise: Managing your finances effectively takes time and knowledge. If you lack either, a financial advisor can handle the intricacies of financial planning while you focus on other priorities.

- Objective perspective: It can be challenging to remain objective when making financial decisions, especially during emotionally charged situations. A financial advisor can offer an unbiased perspective and help you make rational choices.

When choosing a financial advisor, it’s crucial to select a qualified and trustworthy professional. Look for advisors with relevant certifications, such as Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA). Additionally, consider their experience, fee structure, and whether their approach aligns with your financial philosophy.

Understanding Personal Taxes

Taxes are a crucial aspect of personal financial management. Having a solid understanding of how personal taxes work is essential for making informed financial decisions and optimizing your financial well-being. This involves understanding the different types of taxes, tax brackets, deductions, credits, and how they apply to your specific financial situation.

Types of Taxes

There are various types of taxes that individuals may encounter, including:

- Income Tax: Levied on earnings from employment, investments, and other sources of income.

- Property Tax: Based on the value of owned real estate, such as land and buildings.

- Sales Tax: Applied to the purchase of goods and services, varying by location.

- Capital Gains Tax: Levied on profits earned from the sale of assets, such as stocks or real estate.

Tax Brackets and Deductions

Tax brackets determine the percentage of income paid in taxes. These brackets are progressive, meaning higher income earners typically pay a larger proportion of their income in taxes. Tax deductions reduce taxable income, lowering the overall tax liability. Common deductions include expenses related to homeownership, education, healthcare, and charitable contributions.

Tax Credits

Tax credits directly reduce the amount of tax owed, offering a dollar-for-dollar reduction in tax liability. They are typically tied to specific activities or expenses, such as child tax credits for families with qualifying children or education credits for tuition expenses. Understanding eligible tax credits can significantly impact tax savings.

Impact on Financial Planning

Effective personal financial management requires integrating tax planning into overall financial strategies. This includes:

- Investment Decisions: Considering the tax implications of investment choices, such as capital gains taxes and tax-advantaged retirement accounts.

- Retirement Planning: Understanding the tax treatment of retirement savings and withdrawals.

- Charitable Giving: Optimizing charitable contributions for maximum tax benefits.

Seeking Professional Advice

Navigating the complexities of the tax system can be challenging. Consulting with a qualified tax advisor or financial planner can provide personalized guidance and ensure compliance with tax laws.

Conclusion

In conclusion, adopting effective strategies for personal financial management is crucial for long-term stability and growth.

{kind=link}