Managing finances as a new parent can be overwhelming. Learn essential tips to budget effectively and prepare for the future while balancing the needs of your growing family.

Creating a Family Budget

Having a new baby brings so much joy, and also a lot of new expenses! Creating a family budget is more important than ever to navigate these financial changes. Here’s how to get started:

1. Track Your Spending:

Before you can create a budget, you need to know where your money is going. Track all your expenses for a month – groceries, diapers, utilities, everything. Apps or spreadsheets can be helpful for this.

2. Identify Needs vs. Wants:

Separate your expenses into “needs” (essentials like housing, food, and healthcare) and “wants” (things you enjoy but aren’t strictly necessary, like takeout or subscriptions). This helps you see where you can potentially cut back.

3. Set Realistic Goals:

What are your financial priorities? Saving for your child’s education? Paying off debt? Setting clear goals will help guide your budget decisions.

4. Build Your Budget:

There are various budgeting methods (50/30/20, envelope system, etc.). Choose one that works for you and allocate your income to different categories based on your tracked spending and goals. Remember to factor in those new baby expenses!

5. Make Adjustments as Needed:

Life with a newborn is unpredictable. Don’t be afraid to adjust your budget as needed. Regularly review and tweak your plan to ensure it still aligns with your changing financial situation and priorities.

6. Communicate and Cooperate:

If you have a partner, make sure you’re both on the same page about the budget. Open communication about finances is essential for a less stressful financial journey together.

Tracking Your Expenses

Having a baby brings a whole wave of new expenses. From diapers and formula to clothes they quickly outgrow, it’s easy to lose track of where your money is going. That’s why tracking expenses is essential for new parents.

Here’s how to effectively track your expenses:

- Use Budgeting Apps: There are many user-friendly budgeting apps available that can help you monitor your spending and categorize your expenses, making it easy to see where your money is going.

- Spreadsheets: If you prefer a more hands-on approach, create a spreadsheet to track your income and expenses. This allows for customization and detailed analysis of your finances.

- Review Bank and Credit Card Statements: Regularly examine your statements to identify spending patterns and areas where you can potentially cut back.

- Categorize Expenses: Divide your spending into categories like diapers, formula, clothing, healthcare, etc. This will give you a clearer picture of your essential expenses versus discretionary spending.

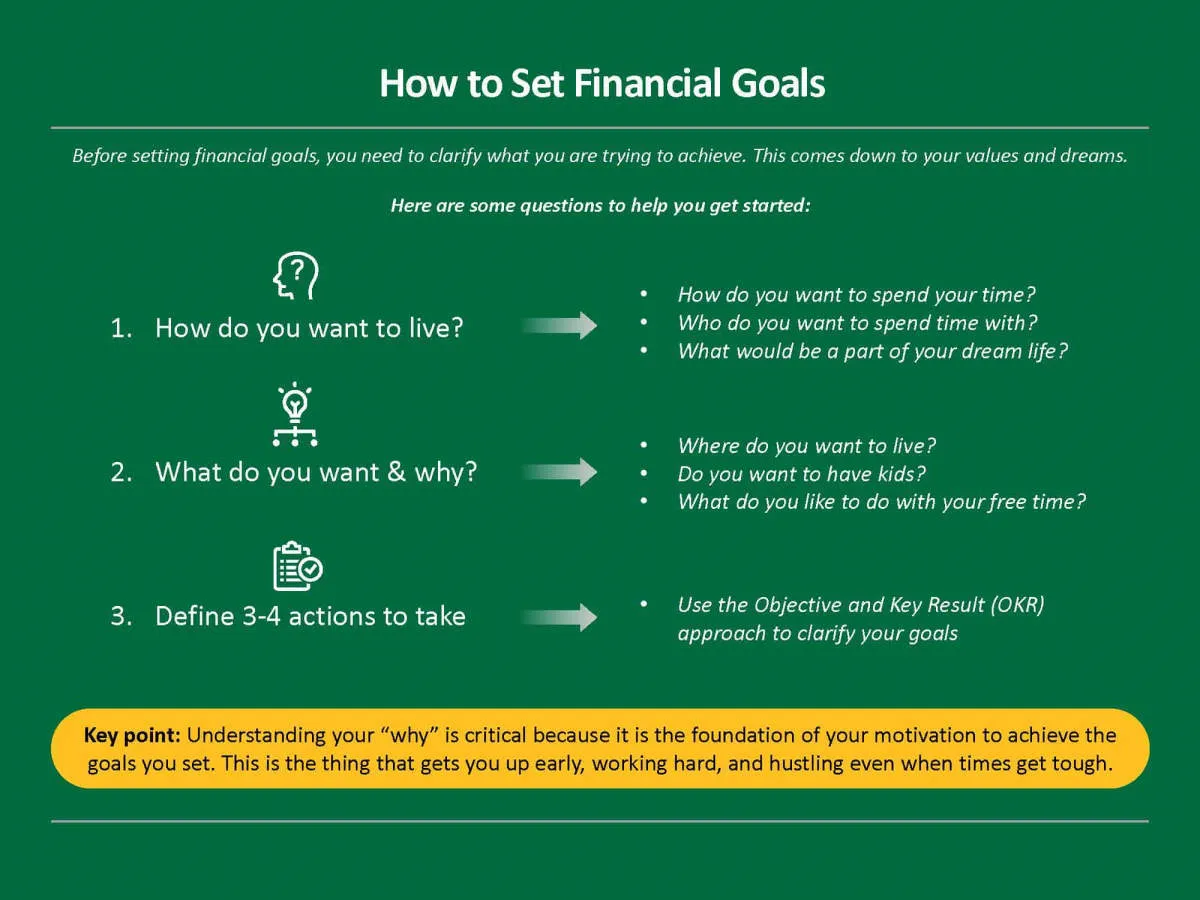

Setting Financial Goals

Becoming a parent comes with a whole new set of financial responsibilities. Setting clear financial goals can help you navigate these changes and build a secure future for your family.

Short-Term Goals:

- Building an Emergency Fund: Aim for 3-6 months’ worth of living expenses in an easily accessible account. This provides a safety net for unexpected events like medical bills or job loss.

- Managing Day-to-Day Expenses: Create a budget that incorporates the added costs of diapers, formula/food, and childcare. Track your spending to identify areas for potential savings.

- Tackling Existing Debt: Prioritize paying down high-interest debts like credit cards to free up more money in your budget.

Long-Term Goals:

- Saving for College: It’s never too early to start! Research different college savings plans and contribute regularly, even if it’s a small amount.

- Planning for Retirement: Having a child doesn’t mean putting your retirement on hold. Continue contributing to retirement accounts to ensure your financial security in the future.

- Protecting Your Family: Look into life insurance policies to provide financial support for your family in case the unexpected happens.

Remember, financial goals are personal. The key is to identify what’s most important for your family’s well-being and create a plan to achieve it. Regular review and adjustments are essential as your family grows and your financial situation evolves.

Building an Emergency Fund

Having a baby is a joyous occasion, but it also comes with a whole new set of financial responsibilities. One of the smartest things you can do to protect your family’s financial well-being is to establish a solid emergency fund. This fund serves as a safety net for unexpected expenses, helping you avoid going into debt when life throws curveballs.

Why is an emergency fund crucial for new parents?

- Unforeseen medical bills: From unexpected complications to regular check-ups, medical expenses can add up quickly, especially with a newborn.

- Job loss or income reduction: Parental leave or changes in your work situation can impact your income. An emergency fund provides a buffer during such transitions.

- Childcare costs: Emergencies related to your childcare provider might require you to find alternative arrangements, potentially at a higher cost.

- Home and car repairs: Just like with medical expenses, unexpected repairs can pop up, requiring immediate financial attention.

How to build your emergency fund:

- Set a savings goal: Aim for 3-6 months’ worth of essential living expenses. This will provide a comfortable cushion in case of emergencies.

- Start small: Even small contributions add up over time. Set up automatic transfers to your emergency fund, even if it’s just $10 or $20 per week.

- Cut back on non-essential spending: Analyze your budget and identify areas where you can reduce expenses, redirecting those savings to your emergency fund.

- Find extra income opportunities: Explore side hustles or freelance work to boost your savings rate and reach your emergency fund goal faster.

Investing for the Future

Having a child is a huge financial responsibility, but it’s also an important time to start thinking about the future. Investing for your child’s education or your own retirement might feel overwhelming, but even small contributions can make a big difference over time.

Here are some investing ideas to consider:

529 Plan:

This is a tax-advantaged savings plan specifically designed for education expenses. You can contribute to any state’s plan, and the money grows tax-free when used for qualified education costs like tuition, room and board, and even K-12 expenses.

Roth IRA:

While primarily for retirement, a Roth IRA offers flexibility. You contribute after-tax dollars, but withdrawals in retirement are tax-free. Plus, you can withdraw contributions (but not earnings) at any time without penalty, making it a good option for unexpected expenses or even a down payment on a house.

Brokerage Account:

For more investment options, consider a brokerage account. You can invest in stocks, bonds, mutual funds, and ETFs. While this offers more potential for growth, it also comes with higher risk.

Start Small, Stay Consistent:

You don’t need a lot of money to start investing. Even small, regular contributions can add up significantly over time thanks to the power of compound interest. Consider setting up automatic transfers to your chosen investment account each month.

Managing Debt

Bringing a child into the world comes with immense joy, and also, inevitably, increased expenses. If you’re already carrying debt, this new phase of life can feel financially overwhelming. Here’s how to proactively manage debt as a new parent:

Create a Budget – and Stick to It

Having a clear picture of your income and expenses is crucial. Factor in new baby costs like diapers, formula/food, and healthcare. Identify areas where you can cut back to make room for these expenses and debt payments.

Prioritize High-Interest Debts

Focus on paying down debts with the highest interest rates first. This typically includes credit card debt. Even small additional payments towards these debts can make a significant difference in the long run.

Explore Debt Consolidation Options

If you’re juggling multiple debts, look into consolidating them into one loan with a lower interest rate. This can simplify your payments and potentially save you money on interest.

Communicate with Your Creditors

Don’t hesitate to reach out to your creditors and explain your situation. Many lenders are willing to work with new parents, offering options like temporary hardship plans or adjusted payment schedules.

Seek Professional Guidance

Consider consulting with a financial advisor. They can help you create a personalized debt management plan tailored to your specific circumstances and goals as a new parent.

Using Financial Tools

Managing your finances as a new parent can feel overwhelming, but utilizing financial tools can provide structure and clarity. Here are some tools to consider:

1. Budgeting Apps:

Budgeting apps like Mint, YNAB (You Need a Budget), or EveryDollar can help you track income and expenses, set financial goals, and identify areas for savings. Many of these apps link directly to your bank accounts for real-time updates.

2. Savings Accounts:

Open a dedicated savings account for your child’s future expenses, like education or a first car. Consider a high-yield savings account to maximize interest earned over time.

3. Investment Accounts:

Starting early with investments is key to building long-term wealth. Consider a 529 plan for education savings or a custodial account to invest on your child’s behalf. Consult with a financial advisor to determine the best options for your situation.

4. Online Calculators:

Utilize online calculators to estimate future costs, such as college tuition or childcare expenses. This can help you plan and save accordingly.

5. Expense Tracking Tools:

Track your spending habits using spreadsheets or expense tracking apps. Identifying unnecessary expenses can free up funds for savings or other financial goals.

Remember: Every family’s financial situation is unique. Choose the tools that best align with your specific needs and goals.

Reviewing and Adjusting Your Plan

Having a financial plan is great, but it’s not a “set it and forget it” kind of thing, especially with a new little one changing the game. Life with a baby is full of surprises, and your finances need to be flexible enough to handle them. That’s where regular check-ins come in.

When to Review

Aim to review your budget and financial goals at least every three to six months. Major life changes, like a new job or a move, also call for a review.

What to Look For

- Spending Habits: Are you sticking to your budget? Have your needs changed? Track your expenses to see where your money is going.

- Emergency Fund: Is it still enough to cover 3-6 months of expenses? Life with a baby can be unpredictable.

- Savings Goals: Are you on track to reach your goals, like college savings or retirement?

- Debt Management: How are you managing any existing debt? Are there opportunities to pay it down faster?

Making Adjustments

Don’t be afraid to make changes to your plan as needed. You might need to:

- Adjust your budget categories (e.g., increase the grocery budget as your baby grows).

- Find ways to cut expenses (e.g., cook at home more often, explore cheaper diaper options).

- Re-evaluate your financial priorities.

- Seek professional financial advice if needed.

Planning for Education Expenses

Having a child is a joyous occasion, but it also comes with significant financial responsibilities. One of the biggest expenses you’ll face as a new parent is your child’s education. The cost of education has been steadily increasing, and it’s never too early to start planning. Here are some tips for planning for your child’s education expenses:

Start Early

The earlier you start saving, the better. Even small contributions can add up over time thanks to the power of compound interest.

Set Up a College Fund

There are several types of college savings accounts available, such as a 529 plan or a Coverdell Education Savings Account. These accounts offer tax advantages that can help you save more for your child’s education.

Estimate Future Costs

Research the potential future costs of college, considering factors such as tuition, room and board, books, and other expenses. Keep in mind that college costs tend to increase each year.

Explore Financial Aid Options

Familiarize yourself with financial aid options such as grants, scholarships, and loans. Research eligibility criteria and application processes in advance.

Consider Your Child’s Interests and Abilities

Encourage your child’s interests and talents. Supporting their passions can lead them to scholarship opportunities or career paths that align with their skills.

Involve Your Child in the Planning

As your child grows older, involve them in discussions about saving for college. Teach them about financial responsibility and the importance of planning for their future.

Seeking Professional Advice

Navigating the world of finances as a new parent can be overwhelming. While this guide provides helpful tips, remember that every family’s situation is unique. Consulting with a financial advisor can provide personalized guidance tailored to your specific circumstances.

Here’s why seeking professional advice is beneficial:

- Creating a Personalized Plan: A financial advisor can help you develop a budget, establish financial goals (like college savings or retirement planning), and create a roadmap to achieve them, all while considering your family’s needs and future aspirations.

- Investment Guidance: They can offer advice on investing for your child’s future education or building a secure financial future for your growing family.

- Insurance Planning: Protecting your family with life insurance, health insurance, and disability insurance is crucial. A financial advisor can help you navigate the options and choose the right coverage.

- Tax Optimization: Having a child often comes with tax benefits. A financial advisor can help you maximize deductions and credits to keep more money in your pocket.

Remember, financial advisors can be valuable resources at any stage of life, but especially during significant transitions like welcoming a new child.

Conclusion

Effective money management is crucial for new parents. By setting up a budget, saving for emergencies, and prioritizing needs over wants, you can secure your family’s financial future.

{kind=link}