Explore the nuances of credit card debt management as we delve into strategies for understanding and effectively handling your financial obligations. Discover essential tips for navigating the complexities of credit card debt and regaining control of your financial well-being.

Understanding Credit Card Debt

Credit card debt is a type of revolving debt, meaning you have a credit limit you can spend from and repay on a monthly basis. While convenient, it’s easy to fall into a cycle of debt if you’re not careful. Here’s what you need to understand:

How Credit Card Debt Works

When you use a credit card, you’re essentially borrowing money from the credit card issuer to make a purchase. You then have a grace period (usually around 21 days) to pay back the borrowed amount in full. If you don’t pay the balance in full by the due date, you’ll be charged interest on the unpaid balance.

The Dangers of High Interest Rates

Credit cards typically come with high interest rates, often much higher than other types of loans. This is one of the most dangerous aspects of credit card debt. The longer you carry a balance, the more you’ll pay in interest charges, making it harder to get out of debt.

Impact on Your Credit Score

Your credit card debt also affects your credit score. A high credit utilization ratio (the amount of credit you’re using compared to your total available credit) can lower your score, making it harder to qualify for loans, rent an apartment, or even get a job in some cases.

Creating a Repayment Plan

Once you have a clear picture of your credit card debt, it’s time to formulate a strategic repayment plan. This involves several key steps:

1. Prioritize Your Debts:

List all your credit cards and their outstanding balances, APRs, and minimum payments. Consider using the debt avalanche or debt snowball methods:

- Debt Avalanche: Focus on paying down the card with the highest APR first, while making minimum payments on others. This saves money on interest in the long run.

- Debt Snowball: Start by paying off the card with the smallest balance first, regardless of interest rate. This provides a psychological boost and motivates continued progress.

2. Explore Debt Consolidation Options:

If you have multiple cards with high interest rates, consider consolidating your debt through:

- Balance Transfer Cards: Transfer high-interest balances to a card with a 0% introductory APR period. This provides temporary relief to focus on repayment.

- Personal Loans: Secure a personal loan with a lower interest rate than your credit cards and use it to pay off your balances.

3. Negotiate with Credit Card Companies:

Don’t hesitate to contact your credit card companies and explore potential options like:

- Lower Interest Rates: Negotiate a lower APR to reduce your overall interest charges.

- Hardship Plans: If facing financial difficulties, inquire about temporary reduced payments or waived fees.

4. Budget for Extra Payments:

Identify areas in your budget where you can cut back on expenses and allocate those funds towards extra debt payments. Even small additional payments can significantly shorten your repayment timeline.

5. Track Your Progress and Stay Consistent:

Regularly monitor your progress and celebrate milestones achieved. Maintaining consistency with your repayment plan is crucial for achieving debt-free living.

Reducing Interest Rates

High interest rates are a major contributor to credit card debt becoming unmanageable. Lowering your interest rate can save you significant money and help you pay off your debt faster. Here are some strategies:

Negotiate with Your Current Creditor

Don’t hesitate to reach out to your credit card company and request a lower rate. Explain your payment history and any hardships you’ve experienced. They may be willing to work with you, especially if you’re a long-time customer.

Balance Transfer Credit Cards

Explore balance transfer credit cards that offer a 0% introductory APR period. This allows you to transfer your existing balance and pay it down interest-free for a set period, typically 12-21 months. Be mindful of balance transfer fees and ensure you can pay off the balance before the introductory period ends.

Debt Consolidation Loans

A debt consolidation loan allows you to combine multiple debts into one with a potentially lower interest rate. This simplifies payments and can make managing your debt more affordable. Shop around for the best rates and terms.

Credit Counseling Agencies

Consider contacting a reputable credit counseling agency. They can negotiate with your creditors on your behalf to lower interest rates or develop a debt management plan. However, be aware of potential fees and research the agency thoroughly.

Consolidating Your Debt

Debt consolidation is a strategy to simplify multiple debts into a single, manageable monthly payment. This can be particularly helpful for credit card debt, where you might be juggling various interest rates and due dates. Here’s how debt consolidation works and how it can benefit you:

Methods of Debt Consolidation:

- Balance Transfer Credit Cards: These cards offer a promotional period with 0% APR, allowing you to transfer balances from high-interest cards and save on interest charges while you focus on paying down the principal. Be mindful of balance transfer fees and ensure you can pay off the balance before the promotional period ends.

- Personal Loans: You can secure a personal loan for the total amount of your credit card debt and use it to pay off your cards. This consolidates your debt into one fixed monthly payment with a potentially lower interest rate. Shop around for the best interest rates and loan terms.

- Home Equity Loans or Lines of Credit (HELOC): If you’re a homeowner, you might consider tapping into your home equity. However, remember that this uses your home as collateral, and defaulting on the loan could lead to foreclosure.

Benefits of Consolidating Debt:

- Simplified Finances: Manage one payment instead of multiple, making tracking and budgeting easier.

- Potential Interest Savings: Secure a lower interest rate, reducing the overall cost of your debt and allowing you to pay it off faster.

- Improved Credit Score: By lowering your credit utilization ratio and demonstrating responsible debt management, consolidation can potentially improve your credit score over time.

Using Balance Transfer Offers

A balance transfer offer allows you to move your existing credit card debt from one or more cards to another card, often with a promotional 0% APR period. This can be a powerful tool for saving money on interest and paying down your debt faster.

How Balance Transfers Work

Here’s the basic process:

- Find a suitable balance transfer credit card. Look for cards offering a 0% introductory APR on balance transfers, ideally for 12 months or longer. Pay attention to the balance transfer fee, which is typically a percentage of the amount transferred (e.g., 3%).

- Apply for the new card. You’ll need to provide your credit history and financial information, just like a regular credit card application.

- Initiate the balance transfer. Once approved, you’ll receive instructions on how to transfer balances from your old cards to the new one. This usually involves providing your old account numbers and the amounts you want to transfer.

- Pay down your balance during the promotional period. Aim to pay as much of the transferred balance as possible before the 0% APR expires. This will maximize your savings and help you become debt-free faster.

Benefits of Balance Transfers

- Interest savings: The 0% introductory APR allows you to temporarily pause interest accrual and put more of your payments towards the principal balance.

- Debt consolidation: Combining multiple card balances into one can simplify your payments and make it easier to manage your debt.

- Improved credit score: Lowering your credit utilization ratio (the amount of credit you use compared to your total credit limit) by transferring balances can potentially boost your credit score over time.

Potential Drawbacks of Balance Transfers

- Balance transfer fees: These fees can offset some of the interest savings, so factor them into your calculations when comparing offers.

- Limited-time offer: The 0% APR period is temporary. If you don’t pay off the balance before it ends, you’ll start accruing interest at the regular rate, which could be higher than your previous cards.

- Temptation to overspend: Opening a new credit card can tempt some people to overspend, potentially adding to their debt instead of reducing it.

Avoiding New Debt

While you’re working on paying down your existing credit card debt, it’s crucial to avoid accumulating more. This requires careful budgeting, disciplined spending habits, and a shift in mindset towards financial responsibility. Here are some strategies to help you avoid new debt:

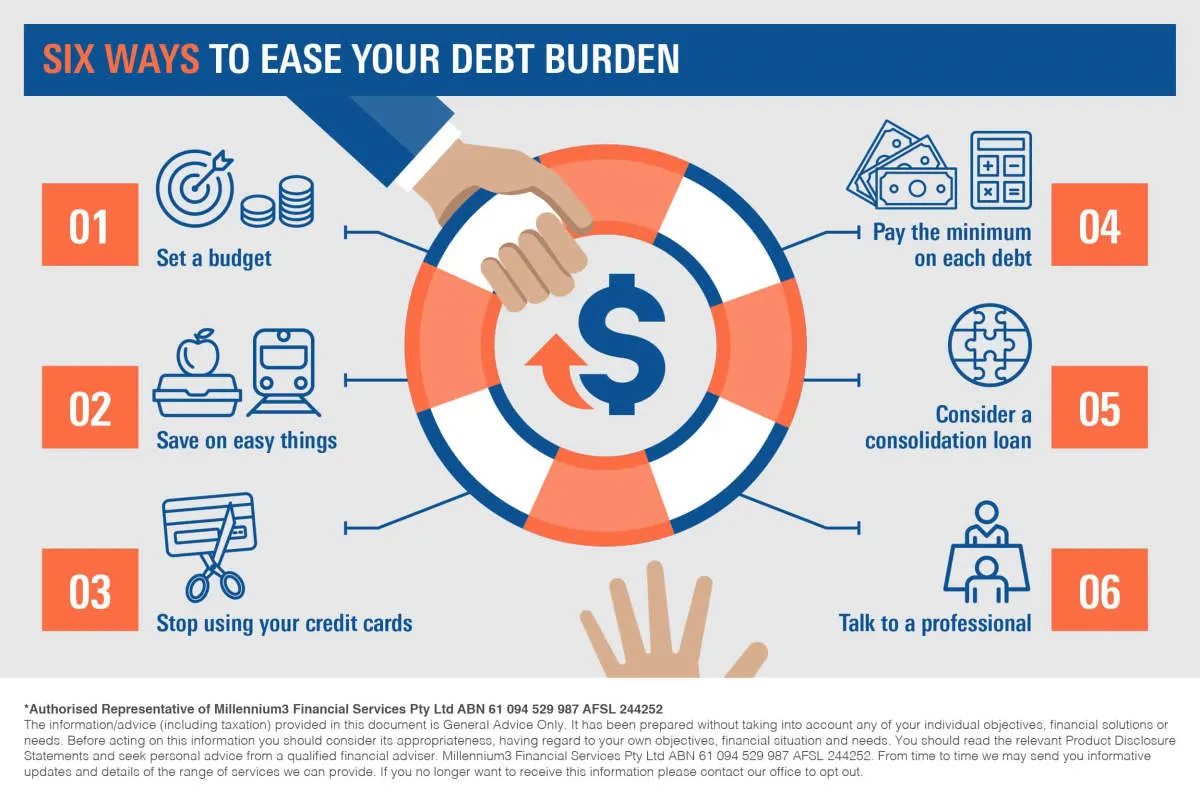

1. Create a Realistic Budget

Understanding where your money goes is the first step towards controlling your finances. Create a detailed budget that tracks your income and all your expenses. Identify areas where you can cut back on discretionary spending and allocate more towards debt repayment.

2. Track Your Spending

Use budgeting apps, spreadsheets, or even a simple notebook to monitor your spending diligently. This helps you stay conscious of your financial habits and identify potential areas where you might be overspending.

3. Live Within Your Means

Avoid the temptation to live beyond your means. Differentiate between “needs” and “wants.” Before making a purchase, ask yourself if it’s essential or if you can delay it until you’re in a better financial position.

4. Build an Emergency Fund

Unexpected expenses like medical bills or car repairs can derail your progress in paying down debt. Having an emergency fund can cushion these financial shocks and prevent you from relying on credit cards to cover them.

5. Explore Alternative Payment Methods

Whenever possible, opt for cash, debit cards, or pre-paid cards instead of credit cards. This will help you stay within your budget and avoid accruing new interest charges.

6. Seek Professional Financial Advice

If you’re struggling to manage your debt or need help creating a budget, consider consulting a financial advisor. They can provide personalized guidance and strategies tailored to your specific situation.

Building an Emergency Fund

While managing existing credit card debt is crucial, preventing further debt is equally important. This is where an emergency fund comes in. An emergency fund acts as a financial safety net, allowing you to cover unexpected expenses without resorting to credit cards. This prevents accruing additional debt and keeps your finances on track.

How does it help with credit card debt?

- Covers unexpected costs: Car repairs, medical bills, or sudden job loss can quickly derail your finances. An emergency fund helps you manage these situations without relying on credit cards.

- Reduces temptation: Having a financial cushion can reduce the temptation to use credit cards for non-essential expenses, preventing further debt accumulation.

- Breaks the cycle of debt: By covering emergencies with savings, you avoid accruing high-interest debt, helping you break free from the cycle of credit card reliance.

How to build an emergency fund:

- Set a savings goal: Aim for 3-6 months’ worth of living expenses. Start small and gradually increase your savings over time.

- Automate your savings: Set up automatic transfers from your checking account to your emergency fund each month.

- Find extra money in your budget: Cut back on unnecessary expenses and redirect those funds towards your emergency savings.

- Consider a side hustle: Explore ways to earn extra income and dedicate those earnings towards your emergency fund.

Increasing Your Income

While managing expenses is crucial for tackling credit card debt, increasing your income can significantly accelerate the process. Bringing in more money means you can allocate more funds towards paying down your balances faster, reducing the overall interest you accrue.

Explore These Income-Boosting Options:

- Negotiate a Raise or Promotion: Assess your value at your current job. Have you taken on new responsibilities or consistently exceeded expectations? If so, now might be the time to negotiate a raise or explore promotion opportunities.

- Seek a Higher-Paying Job: Be open to exploring job opportunities in your field that offer better compensation. Update your resume and leverage online job boards and networking to see what’s available.

- Develop In-Demand Skills: Identify skills in high demand within your industry or areas you’re interested in. Taking online courses, workshops, or earning certifications can increase your earning potential.

- Turn a Hobby into a Side Hustle: Are you passionate about something you do in your free time? Explore ways to monetize your hobbies, whether it’s crafting, writing, photography, or something else you enjoy.

- Freelancing and Gig Work: The gig economy offers numerous opportunities to earn extra income on your own terms. Consider freelancing platforms, delivery services, or other gig work that aligns with your skills and schedule.

Remember: It’s essential to find a balance between increasing your income and managing your time effectively. Evaluate each opportunity carefully and choose options that align with your long-term goals and overall well-being.

Using Financial Tools

Managing credit card debt can feel overwhelming, but various financial tools can help you regain control and work towards a debt-free future. These tools can simplify repayment, potentially save you money, and provide a clearer picture of your overall financial health. Here are some powerful options to consider:

1. Budgeting Apps and Software:

Budgeting apps like Mint, YNAB (You Need a Budget), and Personal Capital offer features specifically designed to track spending, create budgets, and manage debt. These apps can help you:

- Visualize your cash flow and identify areas where you can cut back on expenses.

- Set spending limits and receive alerts when you’re approaching your budget.

- Track your credit card balances and interest charges in one central location.

- Set up payment reminders to avoid late fees.

2. Debt Consolidation Loans:

If you have multiple credit cards with high interest rates, a debt consolidation loan might be a good option. This involves taking out a new loan with a lower interest rate and using the funds to pay off your existing credit card balances. Debt consolidation can simplify your debt repayment by combining multiple payments into one monthly payment with a potentially lower overall interest cost.

3. Balance Transfer Credit Cards:

Some credit cards offer introductory periods with 0% APR (Annual Percentage Rate) on balance transfers. This means you won’t accrue interest on the transferred balance for a specific duration (usually 12-21 months). Transferring high-interest balances to a card with a 0% APR introductory period can help you save on interest and pay down your debt faster.

4. Credit Counseling Agencies:

Reputable, non-profit credit counseling agencies can provide guidance and support in managing your debt. They can help you explore options like a debt management plan (DMP), where the agency negotiates with your creditors to lower interest rates or monthly payments.

5. Online Debt Calculators:

Many free online calculators can help you understand your debt better and make informed repayment decisions. Use these calculators to:

- Determine how long it will take to pay off your debt with your current payments.

- Estimate how much interest you will pay over the life of the loan.

- Compare the impact of making different payment amounts.

Remember: It’s essential to thoroughly research and compare different financial tools and options before making any decisions. Carefully review terms and conditions, fees, and interest rates to choose the most beneficial strategy for your specific financial situation.

Seeking Professional Advice

If you’re struggling to manage your credit card debt, don’t hesitate to seek professional advice. There are many resources available to help you get back on track.

Credit Counseling Agencies can provide guidance on budgeting, debt management, and credit repair. They can also help you negotiate with creditors to lower interest rates or waive fees.

Financial Advisors can provide personalized advice based on your specific financial situation. They can help you create a debt management plan, explore debt consolidation options, and develop a long-term financial strategy.

Bankruptcy Attorneys can provide legal advice if you’re considering filing for bankruptcy. They can explain the different types of bankruptcy, the eligibility requirements, and the potential consequences.

Remember that seeking professional advice is a sign of strength, not weakness. It shows that you’re taking control of your finances and seeking the help you need to achieve your financial goals.

Conclusion

In conclusion, understanding and managing credit card debt is crucial for financial well-being. By budgeting wisely, making timely payments, and avoiding unnecessary expenses, individuals can effectively control their debt and build a secure financial future.

{kind=link}