Building and maintaining a good credit history is crucial for financial stability. Learn valuable tips and strategies to establish and nurture a positive credit profile to secure future financial endeavors.

Understanding Credit History

Your credit history is essentially a financial report card that lenders use to assess your creditworthiness. It’s a detailed record of your borrowing and repayment habits, showcasing your financial responsibility over time. Lenders rely heavily on this information to determine your eligibility for loans, credit cards, and even services like renting an apartment or securing insurance.

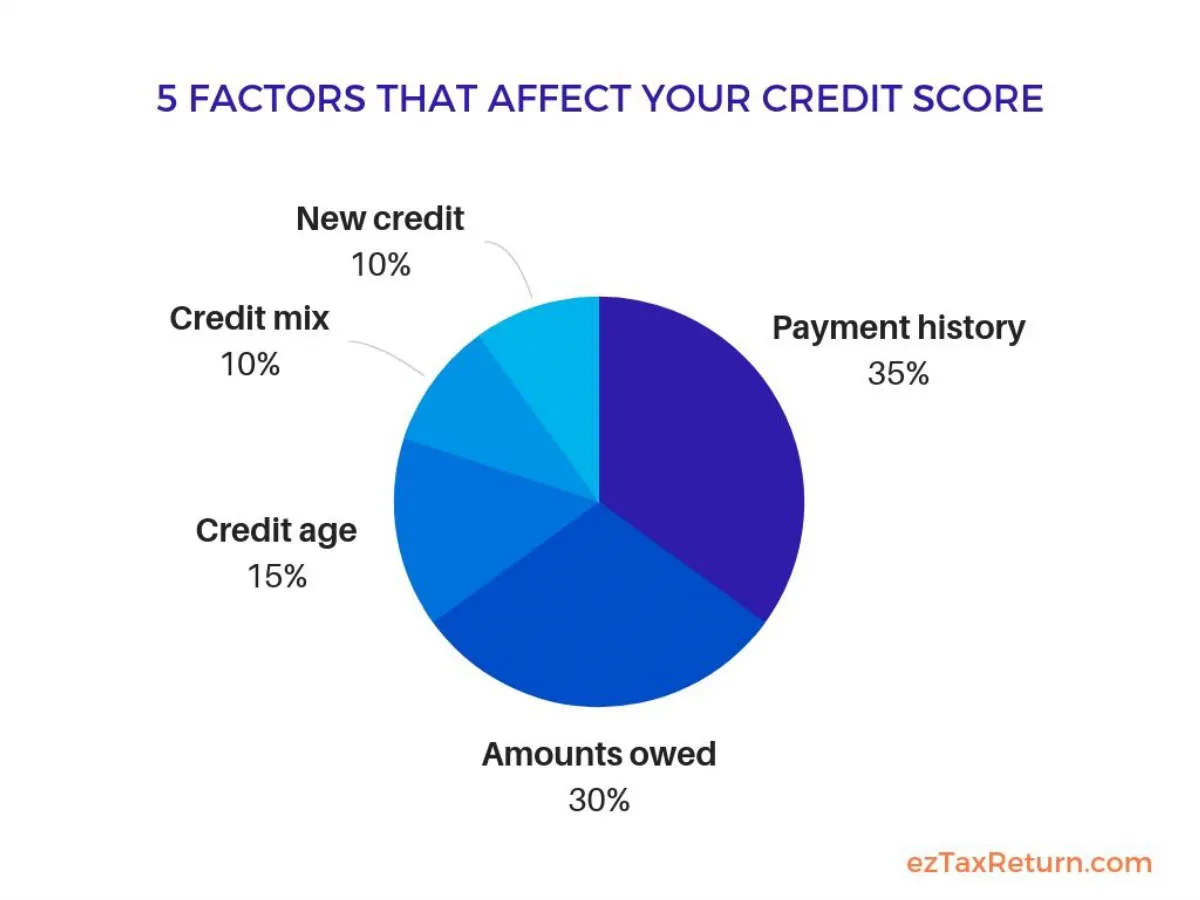

Key components of your credit history typically include:

- Payment history: This is the most crucial aspect, reflecting whether you’ve paid your bills on time. Late payments can significantly damage your credit score.

- Credit utilization: This refers to how much of your available credit you’re currently using. Keeping your credit utilization low is important for a good credit score.

- Length of credit history: A longer credit history generally indicates lower risk for lenders, as it demonstrates a more established pattern of financial behavior.

- Credit mix: Having a diverse mix of credit accounts, such as credit cards, installment loans, and mortgages, can positively impact your credit score.

- New credit inquiries: Each time you apply for credit, a “hard inquiry” is recorded on your report. Too many inquiries in a short period can raise red flags for lenders.

Opening Your First Credit Account

Building a good credit history from scratch starts with opening your first credit account. This can feel like a catch-22: you need credit to build credit, but how do you get that initial credit line? Thankfully, there are several accessible options for first-timers:

1. Secured Credit Card

A secured credit card is a great starting point. With this type of card, you put down a security deposit that typically equals your credit limit. This minimizes the risk for the lender, making them more likely to approve you even with no prior credit history. Your payment activity is reported to the credit bureaus, helping you establish a positive track record.

2. Credit-Builder Loan

Another option is a credit-builder loan. These loans are specifically designed for building credit. You borrow a small amount of money that’s held in a savings account. You make regular payments on the loan, and once it’s paid off, you get access to the funds. Like secured cards, these loans help demonstrate your ability to manage debt responsibly.

3. Become an Authorized User

If you have a trusted friend or family member with good credit, ask if you can become an authorized user on their credit card account. This means you’ll receive a card in your name, and their account activity will be reported to the credit bureaus under your name as well. It’s crucial to choose someone who manages their credit responsibly, as any negative activity on their part will also impact your credit score.

4. Student Credit Cards

If you’re a student, you might qualify for a student credit card. These cards often have lower credit limits and higher interest rates compared to regular credit cards, but they can be easier to get approved for as a student with limited credit history.

Whichever option you choose, remember: opening your first credit account is a significant step towards building a healthy financial future. Be sure to research and compare different offers before making your decision. Pay close attention to interest rates, fees, and terms and conditions to find the best fit for your needs.

Using Credit Responsibly

Responsibly using credit is the cornerstone of building a good credit history. It’s not just about making on-time payments, though that is crucial. It’s about demonstrating a pattern of managing debt effectively and making sound financial choices.

Key Principles of Responsible Credit Use:

- Live within your means: Avoid charging more than you can comfortably repay by the due date. Create a realistic budget to track your income and expenses, ensuring your credit card charges align with your financial capacity.

- Pay your bills on time, every time: Late payments can severely damage your credit score. Set reminders or automate payments to avoid missing due dates.

- Maintain a low credit utilization ratio: Ideally, keep your credit utilization (the amount of credit you use compared to your total available credit) below 30%. High credit utilization can signal to lenders that you’re relying heavily on credit.

- Avoid opening too many accounts in a short period: Each new credit application can result in a hard inquiry on your credit report, potentially lowering your score. Only apply for credit when you genuinely need it.

- Review your credit report regularly: Check your credit report from all three credit bureaus (Equifax, Experian, and TransUnion) at least annually to monitor for errors and signs of potential fraud. You can access your reports for free from AnnualCreditReport.com.

Paying Bills on Time

One of the most crucial factors in building and maintaining good credit is paying your bills on time, every time. Payment history is the most significant factor influencing your credit score, and late payments can have a negative impact that lingers for years.

Here’s why on-time payments are so important:

- Demonstrates Responsibility: Lenders see on-time payments as a sign that you are a responsible borrower who will likely repay debts as agreed.

- Builds Positive Credit History: Each on-time payment adds a positive entry to your credit report, gradually building a strong track record.

- Avoids Late Fees and Penalties: Paying late often results in late fees, which can add up quickly and damage your financial stability. Additionally, some lenders may increase your interest rate after repeated late payments.

Here are some tips for ensuring you pay your bills on time:

- Set Reminders: Utilize calendar reminders, phone alerts, or financial apps to notify you of upcoming due dates.

- Consider Autopay: Many lenders offer automatic payment options, ensuring bills are paid on time without needing to remember each month.

- Create a Budget: A well-structured budget helps you track income and expenses, making it easier to allocate funds for bills and ensure you have the money available when payments are due.

Keeping Balances Low

A key factor in building and maintaining a good credit history is keeping your credit card balances low. This demonstrates responsible credit management and positively influences your credit utilization ratio, a significant component of your credit score.

What is credit utilization ratio? Your credit utilization ratio is the percentage of available credit you are currently using. For example, if you have a credit card with a $1,000 limit and a balance of $300, your credit utilization ratio is 30%.

Why is a low credit utilization ratio important? A lower credit utilization ratio indicates to lenders that you are not overly reliant on credit and are managing your finances responsibly. Generally, a good credit utilization ratio is 30% or lower. Keeping it lower is even better, showcasing excellent credit management.

Tips for keeping balances low:

- Pay your bills on time, every time: Late payments can lead to penalty fees and increased interest rates, pushing your balances higher.

- Make more than the minimum payment: Paying only the minimum keeps your balance high and accrues more interest, making it harder to pay down debt.

- Track your spending: Be mindful of your credit card purchases and avoid overspending. Utilize budgeting apps or tools to track your expenses effectively.

- Consider increasing your credit limit: Requesting a credit limit increase can instantly lower your credit utilization ratio. However, only do this if you are confident in managing the higher limit responsibly.

Avoiding Too Much Debt

A major factor in building and maintaining good credit is managing your debt responsibly. High levels of debt can be a red flag to lenders, indicating potential risk. Here are some tips for keeping your debt levels manageable:

- Live within your means: This age-old advice holds true. Create a realistic budget that tracks your income and expenses. Prioritize spending on necessities and avoid unnecessary purchases, especially on credit, that can quickly accumulate debt.

- Limit credit card use: While credit cards can be useful tools for building credit, it’s essential to use them responsibly. Try to keep your credit utilization rate (the amount of credit you use compared to your total available credit) low, ideally below 30%.

- Strategize debt repayment: If you have existing debt, develop a plan for paying it down efficiently. Consider strategies such as the debt snowball method (paying off the smallest debts first) or the debt avalanche method (tackling debts with the highest interest rates first).

- Emergency fund is key: Unexpected expenses can arise, leading to increased debt if you’re not prepared. Establish an emergency fund with 3-6 months’ worth of living expenses to cover unforeseen costs without relying heavily on credit.

- Borrow only what you need: Before taking on any new debt, carefully consider whether it’s truly necessary. Avoid borrowing for non-essential items and be mindful of the long-term financial implications of taking on debt.

Checking Your Credit Report

Regularly checking your credit report is crucial for maintaining good credit health. It allows you to:

- Identify any errors or inaccuracies: Mistakes happen, and incorrect information on your credit report can negatively impact your score.

- Detect potential fraud: Monitoring your report helps you spot unauthorized activity, such as accounts opened in your name without your knowledge.

- Track your progress: Checking your report periodically allows you to see how your credit-building efforts are reflected in your score.

You are entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) every 12 months through AnnualCreditReport.com.

When reviewing your report, pay close attention to:

- Personal Information: Ensure your name, address, and Social Security number are accurate.

- Account History: Verify that all accounts listed belong to you and that the information is correct (balances, payment history, etc.).

- Inquiries: Review the list of inquiries made on your credit report. Hard inquiries, such as those made when you apply for credit, can slightly lower your score.

Disputing Errors

Sometimes, errors can creep into your credit report, negatively impacting your credit score. It’s crucial to regularly review your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) for any inaccuracies. Common errors include:

- Incorrect personal information (name, address, social security number)

- Accounts that don’t belong to you

- Inaccurate account balances or payment history

- Duplicate accounts

If you find an error, you have the right to dispute it. Here’s how:

1. Contact the Credit Bureau

Contact the credit bureau reporting the error. You can typically dispute errors online, by mail, or by phone. Provide specific details about the error, including supporting documentation (e.g., account statements, bills).

2. Contact the Creditor

It’s also a good idea to contact the creditor (e.g., lender, credit card issuer) that provided the inaccurate information. They can investigate the issue from their end and potentially correct the error with the credit bureau.

3. Follow Up

Credit bureaus are legally required to investigate disputes within 30 days (45 days in some cases). After the investigation, they will notify you of the outcome. If the error is corrected, ensure the updated information is reflected in your credit report.

Building Credit Through Different Accounts

Establishing a diverse credit mix is beneficial for building a robust credit history. Credit scoring models consider various types of credit accounts when calculating your score. Here are some common types of credit accounts that can help you build credit:

1. Credit Cards

Credit cards are a widely accessible type of revolving credit. Responsible credit card usage, such as making on-time payments and maintaining a low credit utilization ratio, demonstrates your ability to manage credit effectively.

2. Installment Loans

Installment loans involve borrowing a fixed amount of money and repaying it in scheduled installments over a predetermined period. Examples include auto loans, personal loans, and student loans. Successfully managing installment loans shows lenders your ability to handle larger credit amounts and make consistent payments.

3. Retail Credit Accounts

Retail credit accounts, such as store credit cards or charge accounts, can help you build credit, especially when starting. However, be mindful of potentially high-interest rates and aim to pay off balances in full each month.

4. Secured Credit Cards

Secured credit cards are designed for individuals with limited or no credit history. These cards require a security deposit, which typically serves as the credit limit. Using a secured credit card responsibly can help establish credit and transition to unsecured credit options in the future.

5. Credit-Builder Loans

Credit-builder loans are specifically designed to help individuals build or improve their credit scores. These loans typically involve a small loan amount deposited into a savings account, which you repay over time. The lender reports your payments to the credit bureaus, allowing you to establish a positive credit history.

Note: It’s important to borrow responsibly and only apply for credit when needed. Opening too many accounts in a short period can negatively impact your credit score.

Monitoring Your Credit Regularly

Keeping a close eye on your credit reports is crucial for maintaining good credit health. Regular monitoring allows you to:

- Catch errors and inaccuracies: Mistakes happen. Regularly reviewing your reports helps you spot and correct any inaccuracies that could be dragging down your score.

- Detect potential fraud: Unusual activity or accounts you don’t recognize could be a sign of identity theft. Prompt detection is key to minimizing damage.

- Track your progress: Monitoring your credit allows you to see the impact of your financial habits and measure your progress toward your financial goals.

You can access your credit reports for free from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually. Consider staggering your requests throughout the year to have more frequent updates on your credit status.

Conclusion

In conclusion, building and maintaining a good credit history is vital for financial stability and future opportunities. Consistent timely payments and responsible credit utilization are key for a healthy credit profile.

{kind=link}