Are you a new homeowner looking to manage your finances better? Discover practical tips and expert advice on how to navigate the world of homeownership and budgeting in this insightful article.

Creating a Home Budget

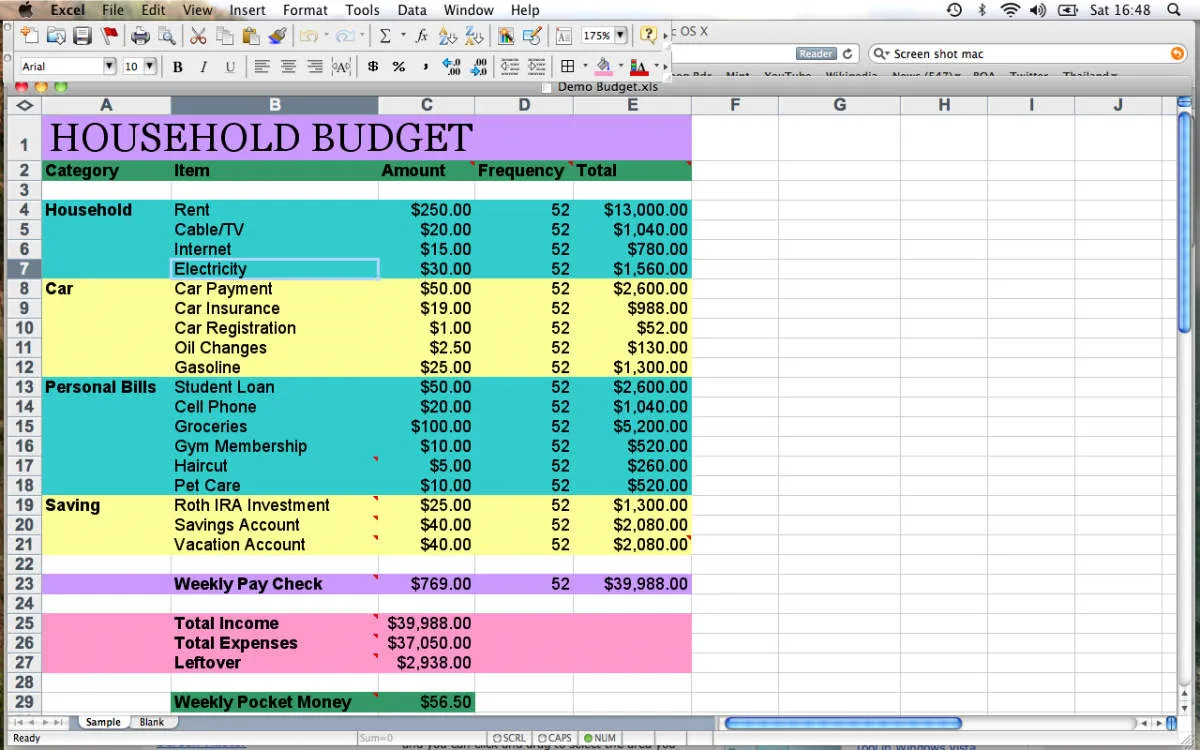

Crafting a realistic home budget is the cornerstone of responsible homeownership. It’s more than just knowing your income and expenses; it’s about planning for the unexpected and achieving your financial goals. Here’s a step-by-step guide to get you started:

1. Track Your Income and Expenses

Begin by listing all sources of income. Next, meticulously track your expenses, categorizing them as essential (mortgage/rent, utilities, groceries) and non-essential (entertainment, dining out). This will provide a clear picture of your current financial standing.

2. Identify Areas for Adjustment

Analyze your spending habits. Are there areas where you can cut back? Can you find more affordable alternatives for certain expenses? Small adjustments can make a big difference in the long run.

3. Set Realistic Financial Goals

Determine your short-term and long-term goals. Do you want to build an emergency fund? Save for renovations? Having clear objectives will guide your budgeting decisions.

4. Implement the 50/30/20 Rule (or Similar)

Consider budgeting frameworks like the 50/30/20 rule, where 50% of your income goes towards needs, 30% towards wants, and 20% towards savings and debt repayment. Adjust the percentages to fit your individual needs and goals.

5. Utilize Budgeting Tools

Explore budgeting apps or spreadsheets to simplify the process. These tools can help track spending, set reminders, and visualize your progress.

6. Review and Adjust Regularly

Your financial situation isn’t static. Make it a habit to revisit and adjust your budget as needed, especially after major life changes or unexpected expenses.

Understanding Mortgage Payments

Navigating the world of mortgages is a significant step in homeownership. Understanding your mortgage payments and how they work is crucial for managing your finances effectively.

Components of a Mortgage Payment

Your monthly mortgage payment typically consists of four main parts, often referred to as “PITI”:

- Principal: This is the portion of your payment that goes directly towards paying down the original amount of money you borrowed to purchase your home.

- Interest: This is the cost of borrowing the money. The interest rate will significantly impact the overall amount you pay back over the life of the loan.

- Taxes: Lenders often collect property taxes as part of your monthly payment and hold them in an escrow account. These funds are then paid to the local government on your behalf.

- Insurance: Similar to property taxes, your mortgage payment might include homeowners insurance premiums. This coverage protects you financially from damages to your home.

Amortization Schedule:

An amortization schedule is a table that outlines each mortgage payment over the life of the loan, showing how much goes towards principal, interest, taxes, and insurance. Reviewing this schedule helps you understand how your payments are applied and how much you’ll pay in total interest.

Additional Factors:

Beyond the core components, several factors can impact your mortgage payments, including:

- Loan Term: A shorter loan term (e.g., 15 years) typically means higher monthly payments but lower total interest paid over time. A longer term (e.g., 30 years) usually results in lower monthly payments but higher overall interest costs.

- Interest Rate Type: Fixed-rate mortgages have an interest rate that remains the same throughout the loan, providing payment predictability. Adjustable-rate mortgages (ARMs) have interest rates that can fluctuate over time, potentially leading to changes in your monthly payments.

Home Insurance Tips

Navigating the world of home insurance is essential for new homeowners. Here are key tips to consider:

Understand Your Coverage Needs

Assess the value of your home’s structure and belongings. Factor in potential risks specific to your location, such as floods, earthquakes, or wildfires. Ensure adequate coverage for rebuilding, replacement, and liability.

Shop Around for the Best Rates

Don’t settle for the first insurance quote. Obtain quotes from multiple insurance providers to compare coverage options and premiums. Look for discounts, such as bundling home insurance with auto insurance.

Review Your Policy Annually

As your life changes, so do your insurance needs. Review your policy annually to ensure adequate coverage for your current situation. Update coverage for renovations, new purchases, or changes in your family structure.

Maintain Detailed Home Inventory

Create a comprehensive inventory of your belongings, including photos or videos. This documentation will be invaluable in the event of a claim, helping to expedite the process.

Consider Additional Coverage Options

Explore additional coverage options like flood insurance, earthquake insurance, or valuable items insurance if your standard policy doesn’t cover them and they are relevant to your location or belongings.

Maintenance and Repair Costs

Owning a home isn’t just about mortgage payments. Unexpected maintenance and repair costs can pop up and surprise you, especially if you’re a new homeowner. Setting aside a budget specifically for these costs is essential.

Here’s what you need to consider:

- Regular Maintenance: This includes tasks like lawn care, gutter cleaning, HVAC servicing, and appliance upkeep. These costs are ongoing and vary depending on your home and location.

- Emergency Repairs: A burst pipe, a leaky roof, or a broken appliance can happen unexpectedly. Having an emergency fund for these situations will save you from financial stress.

- Long-Term Savings: While some repairs might seem small, addressing them promptly can prevent bigger, more expensive problems down the line.

Tips for Managing Maintenance Costs:

- Research typical costs: Familiarize yourself with average maintenance expenses in your area.

- Create a home maintenance schedule: Regular upkeep can prevent many major repairs.

- Get multiple quotes for repairs: Don’t hesitate to shop around for the best price from reputable contractors.

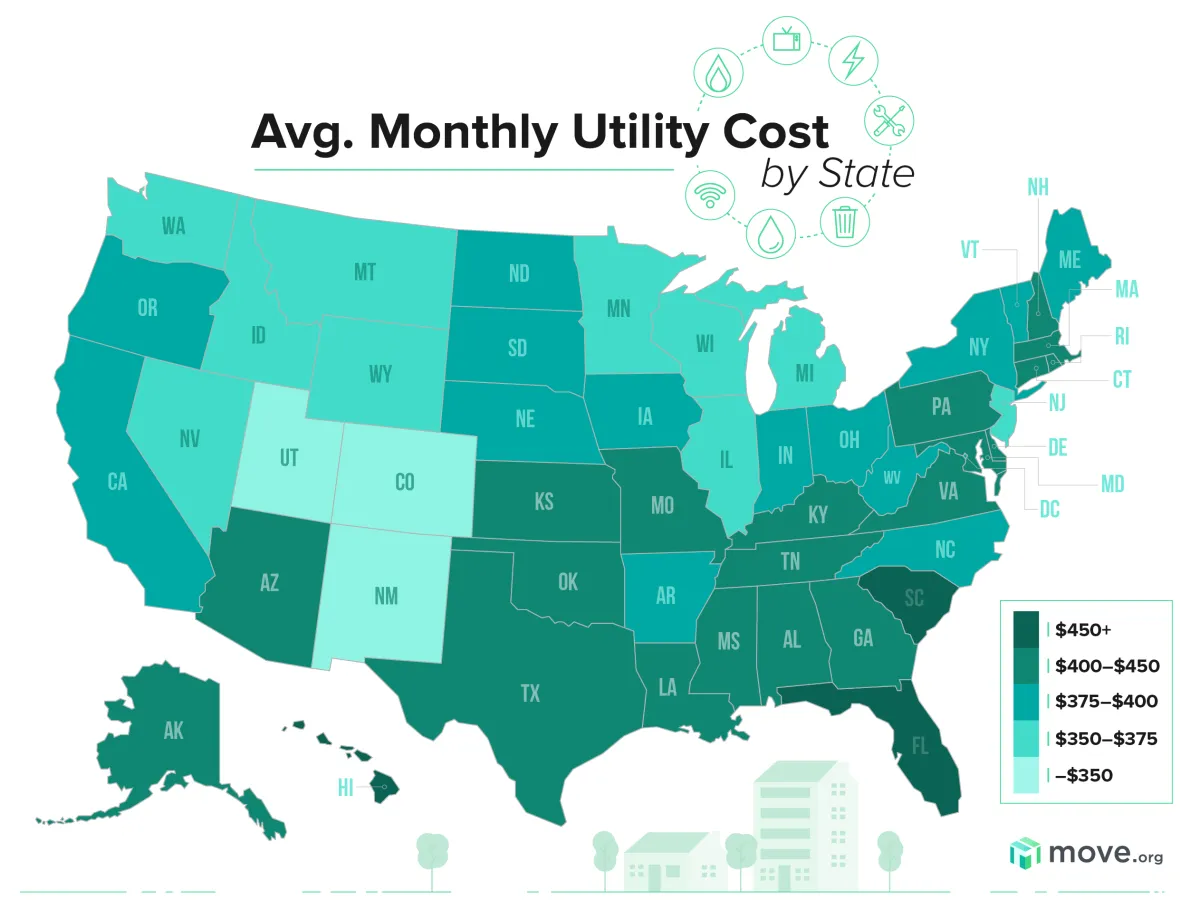

Utility Expenses

Moving into your new home comes with a wave of new financial responsibilities, and utility expenses are right up there. Here’s what you need to know to manage these costs effectively:

Understanding Your Utilities

Familiarize yourself with the specific utilities you’ll be responsible for. This typically includes:

- Electricity:

- Gas:

- Water and Sewer:

- Garbage and Recycling:

- Internet and Cable/Satellite:

Tips for Managing Utility Costs

- Energy Audit:

- Appliance Efficiency:

- Temperature Control:

- Water Conservation:

- Lighting Choices:

- Bundle Services:

- Track Your Usage:

Building an Emergency Fund

As a new homeowner, it’s more important than ever to have a financial safety net. Unexpected home repairs can pop up at any time, and you don’t want to be caught off guard without the funds to cover them. That’s where an emergency fund comes in.

What is an emergency fund? It’s a stash of money set aside specifically for unexpected expenses, like:

- Major home repairs (e.g., roof leak, plumbing issue)

- Appliance replacements (e.g., refrigerator, oven)

- Sudden job loss

- Medical bills

How much should you save? Aim to have 3-6 months’ worth of essential living expenses in your emergency fund. This includes costs like:

- Mortgage payments

- Property taxes

- Utilities

- Groceries

- Transportation

Where should you keep your emergency fund? Keep it in a separate, easily accessible savings account. This will prevent you from accidentally spending it and ensures it’s there when you need it most.

How do you build it? Start by setting a realistic savings goal, even if it’s just $50 or $100 a month. As you get comfortable, gradually increase that amount. Look for areas in your budget where you can cut back and redirect those funds to your emergency savings.

Investing in Home Improvements

Owning a home isn’t just about having a roof over your head; it’s also about making smart financial decisions. Home improvements are a prime example. While some upgrades are purely aesthetic, others can increase your home’s value and save you money in the long run.

Prioritize for Value and Savings:

Don’t go on a renovation spree just yet! Focus on improvements that offer the best return on investment or address immediate needs:

- Energy Efficiency: Upgrading insulation, windows, and appliances can significantly lower your utility bills.

- Kitchen and Bathrooms: These are big selling points. Even minor updates can make a huge difference.

- Curb Appeal: First impressions matter. Landscaping and a fresh coat of paint can boost your home’s value.

- Maintenance and Repairs: Addressing small issues promptly prevents them from becoming costly problems later.

Budget Wisely:

Before you start swinging a hammer, set a realistic budget. Consider these factors:

- Project Scope: Are you doing a DIY renovation or hiring contractors? Get multiple quotes if needed.

- Material Costs: Prices for lumber, fixtures, and other materials can fluctuate. Factor in potential increases.

- Unexpected Expenses: Always have a contingency fund for unforeseen issues that may arise.

Financing Options:

Large-scale renovations might require financing. Explore your options carefully:

- Home Equity Loans & Lines of Credit: Leverage your home’s equity to secure a loan, but borrow responsibly.

- Personal Loans: These can be useful for smaller projects, but interest rates may be higher.

- Savings: If possible, save up for renovations to avoid taking on debt.

Tax Benefits of Homeownership

One of the often-cited perks of homeownership is the potential for tax benefits. While it’s always wise to consult with a tax professional for personalized advice, here are some common tax advantages associated with owning a home:

Mortgage Interest Deduction

You might be able to deduct interest paid on your mortgage. This can be a significant tax break, especially in the early years of your mortgage when interest payments are typically higher.

Property Tax Deduction

In many cases, you can deduct property taxes you pay on your primary residence. This can provide additional tax savings on top of the mortgage interest deduction.

Capital Gains Exclusion

When you eventually sell your home, you might be eligible to exclude a portion of your capital gains from taxation. This means you could potentially keep more of the profit from the sale.

Important Note: Tax laws and regulations are subject to change. It’s crucial to stay informed about current tax policies and consult with a qualified tax advisor to understand how these benefits apply to your specific financial situation.

Avoiding Common Pitfalls

The excitement of owning a new home can sometimes lead to overlooking crucial financial aspects. Here are some common pitfalls to avoid:

1. Overestimating Your Budget

It’s easy to get caught up in the allure of a beautiful home and stretch your budget thin. Determine a realistic budget that includes not just the mortgage payment, but also property taxes, insurance, potential maintenance costs, and moving expenses. Factor in unexpected expenses that may arise.

2. Skipping the Home Inspection

While it might seem like an added cost, a thorough home inspection is crucial. It can reveal hidden problems like structural damage, plumbing issues, or electrical faults that could result in significant expenses down the line. Don’t skip this step, even if the house seems perfect at first glance.

3. Ignoring Closing Costs

Closing costs are often an unexpected expense for new homeowners. These can include loan origination fees, appraisal fees, title insurance, and more. Research and budget for closing costs upfront to avoid last-minute financial stress.

4. Taking on Too Much Debt

Just because you qualify for a certain loan amount doesn’t mean you need to borrow the maximum. Taking on too much debt can limit your financial flexibility. Carefully consider how much you’re comfortable borrowing and ensure the monthly payments fit comfortably within your budget.

5. Emptying Your Savings Account

While a down payment is important, don’t deplete your entire savings. Having an emergency fund is crucial for unexpected home repairs, medical expenses, or potential job loss. Aim for a balance between a healthy down payment and a comfortable safety net.

6. Forgetting About Home Maintenance

Owning a home comes with ongoing maintenance responsibilities. From landscaping to appliance upkeep, these costs can add up. Factor in a monthly or annual budget for home maintenance to avoid being caught off guard by unexpected repairs or replacements.

Seeking Professional Advice

Navigating the world of homeownership, especially as a first-timer, can feel overwhelming. While there are many resources available to help you manage your finances, seeking advice from qualified professionals can provide personalized guidance and peace of mind. Here are a few key areas where professional advice can be invaluable:

Mortgage Lenders and Brokers

Don’t just settle for the first mortgage you find. A mortgage broker can help you compare rates and loan products from multiple lenders, finding the best fit for your financial situation. They can also guide you through the often-complex mortgage application process.

Real Estate Agents

An experienced real estate agent can be an invaluable asset, not only in finding your dream home but also in negotiating the purchase price and navigating the legal intricacies of the transaction. They can also provide insights into the local housing market.

Financial Advisors

A financial advisor can help you create a comprehensive budget that incorporates your new mortgage payment, property taxes, and other homeownership expenses. They can also advise on strategies for long-term financial planning, such as saving for retirement or your children’s education, while managing your mortgage.

Insurance Agents

Don’t underestimate the importance of insurance! A knowledgeable insurance agent can help you secure the right coverage for your home, belongings, and liability. They can explain the different types of policies available and ensure you have adequate protection.

Home Inspectors

Before closing on your new home, hiring a qualified home inspector is crucial. They can identify any potential issues with the property, from structural problems to outdated electrical systems, giving you leverage to negotiate repairs with the seller or reconsider the purchase altogether.

Conclusion

In conclusion, implementing these practical financial tips can help new homeowners manage their finances efficiently and secure a stable future.

{kind=link}