Managing finances as a freelancer can be daunting. In this article, discover essential tips to help freelancers navigate the world of financial management effectively.

Creating a Budget

Creating a budget is essential for financial stability as a freelancer. Without the regular paycheck of traditional employment, managing income and expenses requires careful planning and tracking.

Here’s a step-by-step guide to crafting a comprehensive freelancer budget:

1. Calculate Your Income

Start by estimating your monthly income. Factor in past earnings, current projects, and potential future work. Be realistic and avoid overestimating, as freelance income can fluctuate.

2. Track Your Expenses

Keep a detailed record of all your expenses, both business-related and personal. Categorize them for a clear understanding of your spending habits.

3. Differentiate Between Needs and Wants

Analyze your expenses and identify essential needs (rent, utilities, groceries) and discretionary wants (entertainment, dining out). Prioritize needs and allocate funds accordingly.

4. Set Financial Goals

Define short-term and long-term financial objectives. This could include building an emergency fund, saving for retirement, or investing in your business growth.

5. Allocate Funds Wisely

Based on your income, expenses, and goals, allocate funds to different categories. Consider using budgeting methods like the 50/30/20 rule or envelope system.

6. Monitor and Adjust Regularly

Regularly review your budget to track progress and make adjustments as needed. Unexpected expenses or changes in income might require adapting your spending plan.

Tracking Your Income and Expenses

As a freelancer, understanding where your money is coming from and where it’s going is crucial for effective financial management. This means diligently tracking both your income and expenses.

Why is Tracking Important?

Accurate Financial Picture: Tracking provides a clear picture of your financial health, allowing you to understand your profitability and make informed decisions.

Tax Preparation: Having organized records of income and expenses simplifies tax filing and helps you identify potential deductions, saving you money.

Budgeting and Planning: By understanding your spending patterns, you can create realistic budgets, manage cash flow, and plan for future financial goals.

How to Track Effectively:

Choose a Method: Numerous options are available, from spreadsheets to accounting software. Select a system that suits your needs and comfort level.

Separate Business and Personal Finances: Maintain separate bank accounts and credit cards for your freelance work to simplify tracking and avoid confusion.

Record Everything: Keep detailed records of all income and expenses, no matter how small. Include dates, descriptions, payment methods, and categorize transactions.

Review Regularly: Don’t wait until tax season! Regularly analyze your income and expense reports to identify trends, areas for improvement, and track your financial progress.

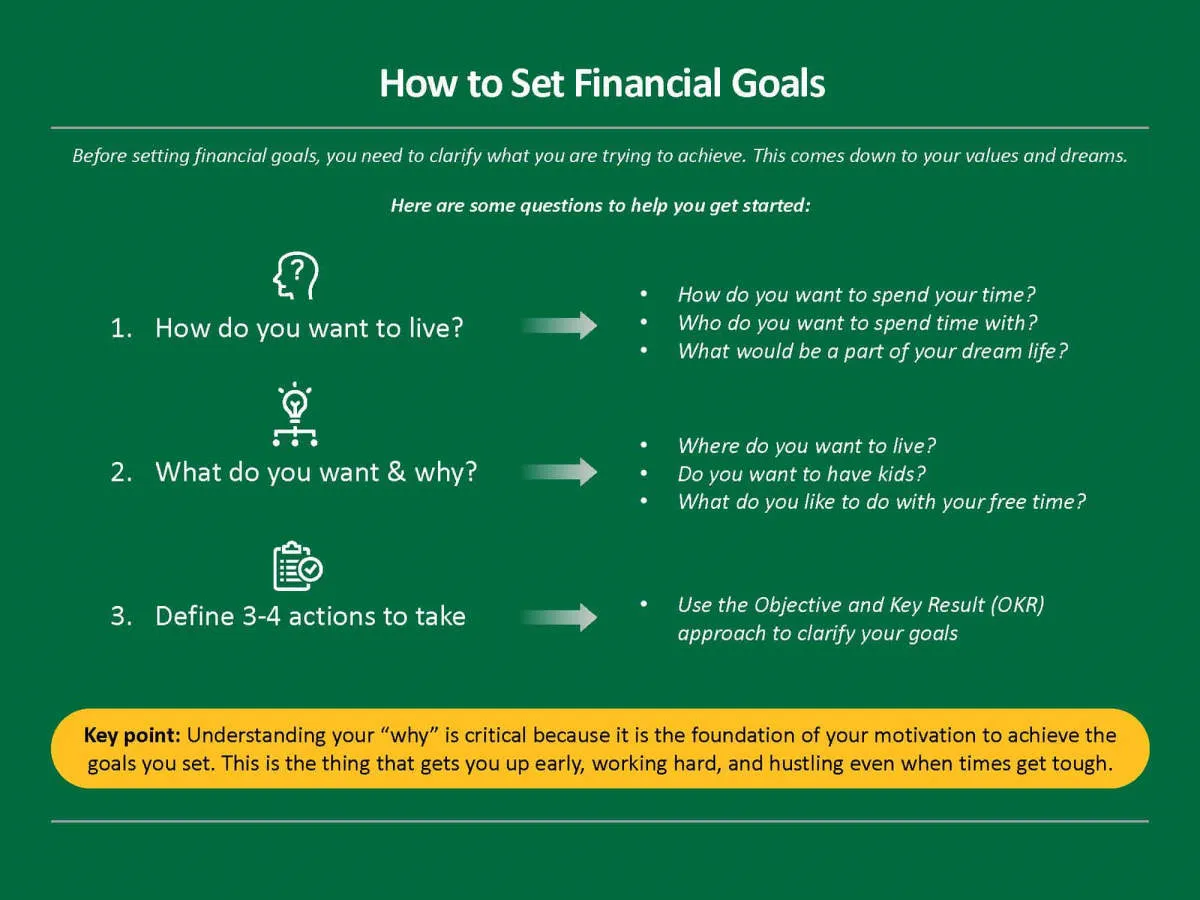

Setting Financial Goals

As a freelancer, having clear financial goals is crucial for staying afloat and planning for the future. Unlike traditional employment with a steady paycheck, freelance income can be unpredictable. Setting goals provides a roadmap for your finances, allowing you to manage your money effectively and work toward your aspirations.

Start by identifying your short-term and long-term goals.

- Short-term goals might include building an emergency fund, saving for a down payment, or paying off debt. These goals usually span a few months to a couple of years.

- Long-term goals typically encompass larger aspirations like buying a house, investing for retirement, or funding your children’s education. These goals generally take several years or even decades to achieve.

Once you have a vision for your goals, quantify them. Determine exactly how much money you need to save and establish a timeline for achieving each goal. This step adds a concrete element to your aspirations, making them feel more attainable.

Building an Emergency Fund

As a freelancer, experiencing unpredictable income is part and parcel of the job. That’s why having a safety net in the form of an emergency fund is crucial. This fund acts as a buffer to cover unexpected expenses or periods of low income, providing peace of mind and financial stability.

How much should you save? A good rule of thumb is to aim for 3-6 months’ worth of living expenses. This includes essential costs like rent/mortgage payments, utilities, groceries, and debt repayments.

Where to keep your emergency fund: Accessibility is key. Opt for a high-yield savings account or a money market account that allows for easy withdrawals while offering a decent return on your savings.

Tips for building your emergency fund:

- Set a budget: Track your income and expenses to identify areas where you can cut back and free up funds for saving.

- Automate your savings: Schedule regular transfers from your checking account to your emergency fund, even if it’s a small amount initially.

- Find extra income opportunities: Take on freelance projects, or explore side hustles to boost your savings rate.

- Replenish your fund after use: If you need to dip into your emergency savings, make it a priority to replenish it as soon as possible.

Investing for the Future

As a freelancer, your income might fluctuate, making it even more crucial to prioritize long-term financial security through investments. Here’s how to get started:

1. Establish an Emergency Fund:

Before diving into investments, secure a safety net of 3-6 months’ worth of living expenses in a high-yield savings account. This fund acts as a buffer during periods of low income.

2. Retirement Planning:

Don’t have an employer-sponsored retirement plan? No problem! Explore options like:

- SEP IRA: Ideal for self-employed individuals and small business owners, allowing for larger contributions.

- Traditional or Roth IRA: Offer tax advantages for retirement savings.

- Solo 401(k): Combines profit-sharing and 401(k) features for self-employed individuals.

3. Explore Investment Options:

Consider diversifying your portfolio with:

- Index Funds: Offer broad market exposure with lower fees compared to actively managed funds.

- ETFs: Similar to index funds, traded on stock exchanges, providing diversification and flexibility.

- Bonds: Fixed-income securities that can provide stability to your portfolio.

- Real Estate: Explore options like rental properties or REITs for potential long-term growth.

4. Automation is Key:

Set up automatic transfers to your investment accounts to make saving effortless and consistent. Even small, regular contributions can grow significantly over time thanks to the power of compound interest.

5. Seek Professional Advice:

Consider consulting with a financial advisor experienced in working with freelancers. They can provide personalized investment strategies based on your financial goals, risk tolerance, and time horizon.

Managing Taxes

One of the most significant differences between being a freelancer and a traditional employee is how you handle taxes. As a freelancer, you’re responsible for paying self-employment taxes and income taxes on your earnings. Here’s what you need to know:

Understanding Self-Employment Taxes

When you work as an independent contractor or freelancer, you’re essentially running your own business. This means you’re responsible for paying both the employer and employee portions of Social Security and Medicare taxes, commonly referred to as self-employment tax.

Quarterly Tax Payments

Unlike traditional employment where taxes are withheld from each paycheck, freelancers are generally required to make estimated tax payments quarterly to the IRS. These payments help you avoid penalties for underpaying your taxes throughout the year.

Tracking Income and Expenses

Meticulous record-keeping is crucial for freelancers. Keep thorough records of all income and business-related expenses. This will not only make tax time easier but also allow you to maximize deductions and potentially reduce your tax liability.

Tax Deductions for Freelancers

As a freelancer, you have access to various tax deductions that can lower your taxable income. Some common deductions include:

- Home office expenses

- Health insurance premiums

- Business-related travel

- Software and technology costs

- Education and professional development

Seeking Professional Tax Advice

Navigating the complexities of taxes as a freelancer can be challenging. Consulting with a qualified tax advisor who specializes in self-employment income is highly recommended. They can provide personalized guidance on tax planning, deductions, and help ensure you’re meeting all tax obligations.

Using Financial Tools

As a freelancer, staying organized is half the battle. Thankfully, there are tons of tools – many of them free – that can help you manage your income, track expenses, and plan for taxes. Here are a few categories to consider:

1. Budgeting and Expense Tracking Apps:

These tools help you monitor your income and expenses, categorize transactions, and even set financial goals. Some popular options include Mint, YNAB (You Need A Budget), and Personal Capital.

2. Invoicing and Payment Platforms:

Streamline your invoicing process and get paid faster with platforms like FreshBooks, Xero, or Wave. These tools allow you to create professional invoices, track payments, and even accept online payments.

3. Tax Software:

Tax time can be stressful for freelancers. Software like TurboTax Self-Employed or H&R Block Self-Employed can help you maximize deductions, file accurately, and minimize your tax liability.

4. Project Management Tools:

While not strictly financial, tools like Asana, Trello, or Monday.com can help you stay organized, manage deadlines, and track project income. This can be incredibly helpful for managing cash flow and ensuring timely payments.

5. Savings and Investment Apps:

Even if you’re freelancing, it’s essential to think long-term. Apps like Acorns, Stash, or Robinhood can help you automate savings, invest spare change, and grow your wealth over time.

Reviewing and Adjusting Your Plan

It’s not enough to create a financial plan; you need to revisit and revise it regularly. The freelance life is full of ebbs and flows, and your financial plan needs to be flexible enough to adapt.

Here’s how to approach the review process:

Set a Review Schedule:

Aim to review your plan at least quarterly, or more frequently if you experience significant changes in income or expenses.

Analyze Your Actuals:

Compare your planned income and expenses to what actually happened. This will highlight areas where you’re on track and where you might need adjustments.

Identify What’s Changed:

Consider any factors that have shifted your financial picture. Did you land a big project? Did your tax liability increase? Did you take on a new expense like health insurance?

Make Adjustments:

Based on your analysis, tweak your budget, savings goals, or even your income targets. Don’t be afraid to make significant changes if needed.

Stay Flexible:

Remember, your financial plan is a living document. Be prepared to adapt and adjust as your freelance career evolves.

Building Good Financial Habits

As a freelancer, having solid financial habits is crucial for navigating the uncertainties of inconsistent income and ensuring long-term financial stability. Here’s how you can build good financial practices:

1. Budgeting and Tracking

Start by understanding your income and expenses. Track your income sources and categorize your expenses. Utilize budgeting apps or spreadsheets to monitor your cash flow effectively. Knowing where your money goes allows for better financial planning and control.

2. Emergency Fund

Freelancing often comes with income fluctuations. Building an emergency fund is essential. Aim for 3-6 months’ worth of living expenses. This fund acts as a safety net during lean periods or unexpected events, providing financial security and peace of mind.

3. Separate Business and Personal Finances

Maintain separate bank accounts and credit cards for business and personal use. This separation simplifies accounting, makes tax filing easier, and provides a clearer picture of your business’s financial health.

4. Consistent Savings

Treat savings like a regular expense. Establish a savings goal, whether for retirement, investments, or future projects. Set up automatic transfers to your savings account to ensure consistent savings even during busy months.

5. Regular Invoicing and Payment Follow-Up

Timely payments are crucial for maintaining a healthy cash flow. Invoice clients promptly upon project completion and implement a system for tracking invoices. Don’t hesitate to follow up on overdue payments politely but persistently.

6. Tax Planning

As a freelancer, you’re responsible for your taxes. Set aside a portion of your income regularly for tax payments. Consult with a tax professional to understand your tax obligations and optimize your tax strategy.

7. Skill Development and Networking

Invest in your professional development. Update your skills, attend industry events, and network with other freelancers. Staying relevant and expanding your network can lead to more opportunities and higher earning potential.

Seeking Professional Advice

Navigating the world of freelance finances can be complex. While this guide offers a good starting point, seeking advice from qualified professionals is invaluable. Consider consulting with:

- Accountants: An accountant specializing in freelance or small business finances can guide you on tax obligations, expense tracking, and financial planning tailored to your situation.

- Financial Advisors: A financial advisor can help you set long-term financial goals, create a budget, plan for retirement, and manage investments – all crucial aspects for freelancers with fluctuating income.

- Tax Professionals: Tax laws can be intricate, especially for freelancers with multiple income streams. A tax professional can ensure you are maximizing deductions, understanding self-employment taxes, and filing correctly to avoid any penalties.

Remember, investing in professional advice is an investment in your financial well-being. Their expertise can save you money, reduce stress, and provide peace of mind as you navigate the world of freelancing.

Conclusion

In conclusion, implementing effective financial management practices is crucial for freelancers to maintain financial stability and reach their financial goals successfully.

{kind=link}