Learn valuable insights on effective financial planning tailored for young professionals. Discover smart strategies to manage your income, savings, and investments for a secure financial future.

Set Financial Goals

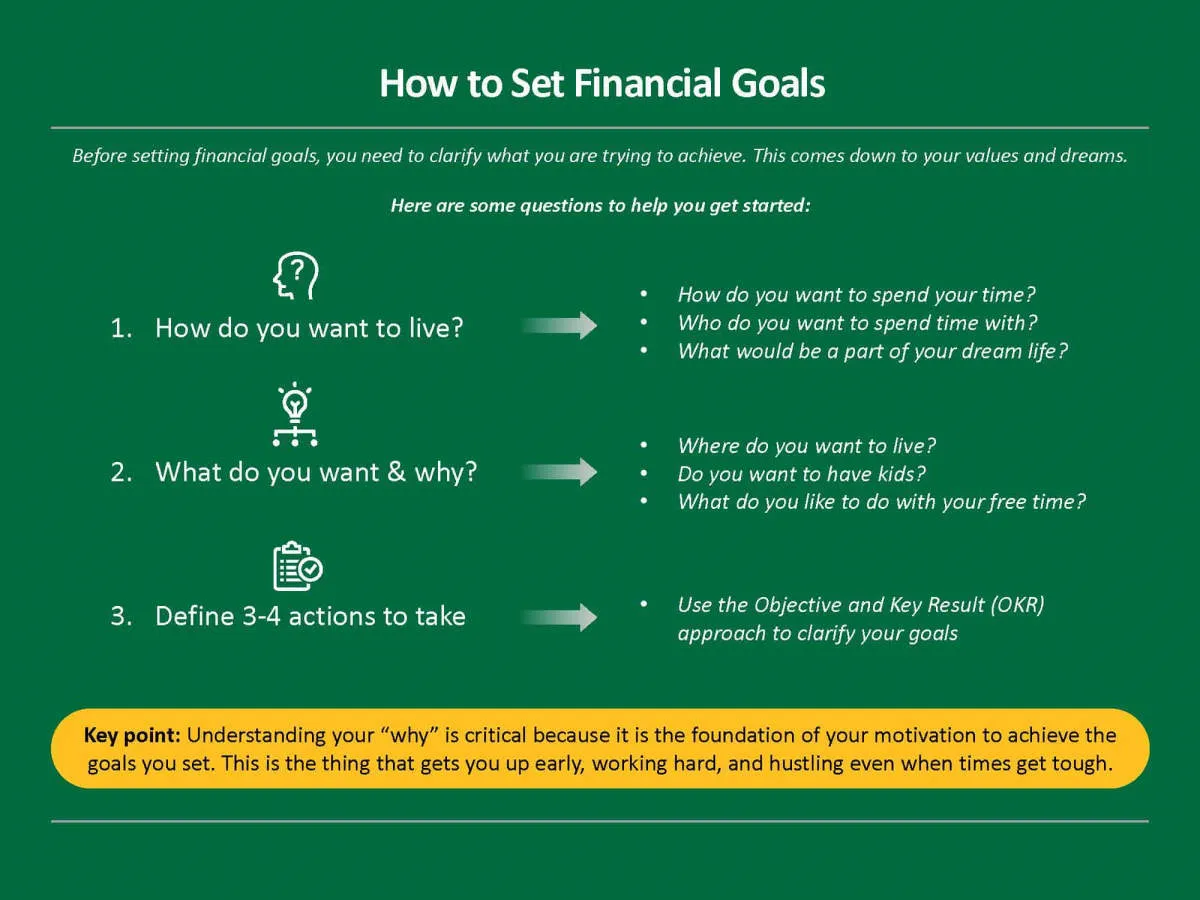

One of the most crucial aspects of financial planning is setting clear and achievable financial goals. Without defined objectives, it’s easy to lose track of your finances and make impulsive decisions. Ask yourself: What do you want to achieve with your money?

Start by identifying both short-term and long-term goals:

Short-Term Goals (within 1-2 years):

- Build an emergency fund

- Pay off high-interest debt (credit cards)

- Save for a down payment on a car

- Take a dream vacation

Long-Term Goals (5+ years):

- Save for retirement

- Purchase a home

- Invest in your education or a career change

- Start a family

Be Specific: Instead of just saying “save more,” quantify your goals. For example, “Save $5,000 for an emergency fund within the next year.” Having specific targets will make your goals seem more tangible and motivate you to stay on track.

Prioritize: You likely have multiple financial goals, so prioritize them based on their importance to you. This will help you allocate your resources effectively and focus on achieving the most critical objectives first.

Review and Adjust: Life is dynamic, and your financial goals may need to change over time. Review your goals periodically (e.g., annually or when significant life events occur) and make adjustments as needed to keep them aligned with your current situation and aspirations.

Create a Budget

Creating a budget is the cornerstone of sound financial planning, especially for young professionals starting their careers. It’s about understanding where your money goes and making informed decisions about your spending and saving habits.

Here’s a step-by-step guide to creating a budget:

- Track your income and expenses. Use a budgeting app, spreadsheet, or a notebook to record all sources of income and every expense for a month or two. This will give you a clear picture of your cash flow.

- Categorize your spending. Divide your expenses into categories like rent/mortgage, utilities, groceries, transportation, entertainment, etc. This helps identify areas where you might be overspending.

- Set realistic financial goals. Determine your short-term and long-term goals (e.g., saving for a down payment, investing, paying off debt). Having clear goals will motivate you to stick to your budget.

- Distinguish between needs and wants. Prioritize essential expenses (needs) over discretionary spending (wants). This will help you allocate your money more effectively.

- Establish spending limits. Set a realistic budget for each expense category based on your income, goals, and spending habits.

- Automate your savings. Set up automatic transfers to your savings account each month. Treat savings like a non-negotiable expense.

- Review and adjust regularly. Your budget is a living document. Track your progress, make adjustments as needed, and don’t be afraid to revisit and refine it periodically. Life changes, and your budget should adapt accordingly.

Build an Emergency Fund

Life is unpredictable, and unexpected expenses can pop up at any time. A car repair, medical bill, or sudden job loss can throw your finances into a tailspin if you’re not prepared. That’s where an emergency fund comes in.

An emergency fund is a stash of money set aside specifically to cover unexpected costs. It acts as a financial safety net, providing peace of mind and preventing you from going into debt when life throws a curveball.

How much should you save?

Aim to save at least three to six months’ worth of living expenses in your emergency fund. This should cover essential costs like rent, utilities, groceries, and transportation. If you have dependents or unstable income, consider saving closer to six to twelve months’ worth.

Where to keep your emergency fund

Keep your emergency fund in a separate, easily accessible account. A high-yield savings account or money market account are good options as they offer easy access to your funds while earning a bit of interest.

Tips for building your emergency fund:

- Start small: Even if you can only save $20 or $50 per week, it adds up over time.

- Automate your savings: Set up automatic transfers from your checking account to your emergency fund each month.

- Cut back on unnecessary expenses: Identify areas where you can reduce spending and redirect that money towards your savings goal.

- Make saving a priority: Treat your emergency fund contributions like non-negotiable expenses.

Invest in Your Future

Investing at a young age is one of the smartest financial moves you can make. The power of compound interest means that even small contributions made early can grow significantly over time. Here’s how to get started:

Determine Your Risk Tolerance

Your risk tolerance refers to how much volatility you’re comfortable with in your investments. Younger investors generally have a longer time horizon, allowing them to take on more risk if they choose. Higher-risk investments have the potential for higher returns but also come with a greater chance of short-term losses.

Explore Different Investment Options

- Retirement Accounts (401(k), Roth IRA): These offer tax advantages and should be a priority for young professionals.

- Index Funds and ETFs: These funds provide broad market exposure and are generally considered lower risk than individual stocks.

- Real Estate: If owning a home is a goal, consider starting to save for a down payment.

Start Small, Be Consistent

You don’t need a large sum of money to begin investing. Start with what you can comfortably afford and focus on consistently contributing to your investments over time.

Manage Debt Wisely

Debt is a fact of life for many young professionals. Student loans, car payments, and mortgages can quickly add up. However, it’s crucial to manage debt responsibly to prevent it from derailing your financial future.

Prioritize High-Interest Debts

Not all debt is created equal. High-interest debts, such as credit card balances, can quickly snowball. Prioritize paying down these debts first to minimize the amount of interest you accrue.

Explore Debt Consolidation or Refinancing

If you have multiple debts, consider consolidating them into a single loan with a lower interest rate. Refinancing existing loans, such as student loans, can also help reduce your monthly payments.

Create a Realistic Budget and Stick to It

A budget is essential for managing debt. Track your income and expenses to identify areas where you can cut back and allocate more money towards debt repayment. Explore budgeting apps or tools for assistance.

Negotiate with Lenders

Don’t be afraid to negotiate with your lenders. If you’re facing financial hardship, they may be willing to work with you. You could potentially negotiate lower interest rates, waived fees, or a modified payment plan.

Avoid Taking on Unnecessary Debt

Before taking on new debt, carefully consider if it’s necessary. Avoid impulse purchases and prioritize saving for large expenses instead of relying on credit.

Understand Taxes

Taxes are a crucial aspect of financial planning, yet they often remain a mystery, especially for young professionals just starting their careers. Understanding how taxes work and how they impact your income is essential for making informed financial decisions.

Key areas to focus on:

- Income Tax: Learn about the tax brackets in your country or region and understand how your income is taxed. Familiarize yourself with deductions, exemptions, and credits that can potentially reduce your tax liability.

- Payroll Taxes: These are automatically deducted from your paycheck and fund social security, Medicare, and other government programs. Understand what these deductions are and how they affect your take-home pay.

- Sales Tax: This is added to the price of goods and services you purchase. While it might seem insignificant for individual purchases, it can add up over time. Be mindful of sales tax when budgeting.

- Property Tax: If you own property, you’ll be subject to property taxes. Understand how property taxes are calculated in your area and factor them into your housing expenses.

Seeking Professional Advice:

Navigating the complexities of the tax system can be challenging. Consider consulting with a qualified tax advisor who can provide personalized guidance based on your specific financial situation. They can help you optimize your tax strategies and ensure you comply with all regulations.

Use Financial Planning Tools

The digital age offers a wealth of financial planning tools that can significantly aid young professionals in managing their finances effectively. These tools come with various features and functionalities, making it easier to track expenses, create budgets, plan investments, and achieve financial goals.

Budgeting Apps: Numerous apps like Mint, Personal Capital, and YNAB (You Need a Budget) can link to your bank accounts and credit cards, automatically tracking income and expenses. These apps provide a clear picture of your spending habits and help identify areas for improvement. They also offer budgeting features to help you allocate funds wisely.

Investment Platforms: Robo-advisors like Betterment, Wealthfront, and Acorns offer automated investment management based on your risk tolerance and financial goals. These platforms require minimal investment knowledge, making them ideal for beginners. Additionally, online brokerage accounts like Fidelity, Schwab, and Vanguard provide access to a wide range of investment options for those who prefer a more hands-on approach.

Financial Calculators: Online financial calculators are readily available to assist with various financial planning aspects. You can find calculators for mortgage payments, retirement savings, loan amortization, and more. These tools offer valuable insights into different financial scenarios and help make informed decisions.

Personal Finance Websites and Blogs: Numerous websites and blogs offer a plethora of information on personal finance, investing, and money management. Reputable sources like NerdWallet, Investopedia, and The Balance provide articles, guides, and resources to enhance your financial literacy and provide valuable tips for young professionals.

By utilizing these financial planning tools, young professionals can gain better control over their finances, develop sound financial habits, and work towards achieving their short-term and long-term financial goals.

Protect Your Income

As a young professional, your income is your most valuable asset. It’s what allows you to build a secure financial future. That’s why it’s crucial to protect it from unexpected events.

Emergency Fund

Life throws curveballs. Having a robust emergency fund acts as a financial buffer, covering unexpected expenses like medical bills, car repairs, or sudden job loss. Aim for 3-6 months’ worth of living expenses in an easily accessible account.

Insurance Coverage

Don’t underestimate the importance of insurance. Consider these key types:

- Health Insurance: Safeguards you from potentially crippling medical expenses.

- Renter’s/Homeowner’s Insurance: Protects your belongings and provides liability coverage.

- Auto Insurance: Essential for covering car repairs and potential liabilities in case of accidents.

- Disability Insurance: Provides income replacement if you’re unable to work due to illness or injury.

Income Protection Strategies

Explore additional strategies to safeguard your income:

- Negotiate a Severance Package: In case of job loss, having a severance package can provide temporary financial support.

- Develop In-Demand Skills: Continuously upskilling yourself makes you a more competitive candidate, reducing the risk of unemployment.

- Consider Side Hustles: A side gig can provide extra income and act as a safety net if your primary income source is disrupted.

Save for Retirement

Retirement might seem ages away, but starting early is crucial for young professionals. The power of compound interest means your money has more time to grow. Here’s what to consider:

Start Now, No Matter How Small

Even small contributions to a retirement account add up over time. Don’t be discouraged if you can’t contribute a large amount right away. The most important thing is to establish the habit of saving early.

Explore Retirement Plans

- 401(k) or Similar: If your employer offers a 401(k) or similar plan, take advantage! Especially if there’s an employer match, which is essentially free money.

- Individual Retirement Account (IRA): IRAs offer tax advantages and allow you to choose your own investments.

Determine Your Risk Tolerance

As a young professional, you have a longer time horizon, which generally means you can tolerate more risk in your investments. Consider a more aggressive investment strategy that has the potential for higher returns over the long term.

Seek Professional Advice

While there are many resources available to help you plan your finances yourself, seeking advice from a certified financial planner (CFP) can provide personalized guidance and expertise. A CFP can help you:

- Assess your current financial situation: They will review your income, expenses, assets, and debts to get a clear picture of your financial standing.

- Define your financial goals: Whether it’s buying a home, saving for retirement, or investing for the future, a CFP will help you articulate your objectives.

- Develop a tailored financial plan: Based on your goals and risk tolerance, they will create a personalized roadmap to help you reach your objectives.

- Navigate complex financial products: From investment options to insurance policies, a CFP can explain complex financial products and help you make informed decisions.

- Stay on track and adjust as needed: Your financial plan should evolve as your life changes. A CFP can provide ongoing support and make necessary adjustments to keep you moving towards your goals.

Remember, investing in professional advice can save you time, money, and potential financial missteps in the long run.

Conclusion

In conclusion, young professionals can secure their financial future by implementing smart budgeting, investing early, managing debt effectively, and setting clear financial goals.

{kind=link}