Creating a solid financial plan as a couple is crucial for long-term financial stability and harmony. Explore essential tips for effective financial planning to achieve your shared goals and build a secure future together.

Setting Financial Goals Together

One of the most crucial aspects of successful financial planning as a couple is establishing shared financial goals. These goals should reflect your aspirations as a team and provide a clear direction for your financial journey.

Start by having open and honest conversations about your individual and shared dreams. Do you want to buy a house, retire early, travel the world, or invest in your children’s education? Once you have a list of potential goals, prioritize them based on importance and timeframe.

Important factors to consider when setting goals together:

- Timeframe: Are these short-term (within a year), mid-term (1-5 years), or long-term (5+ years) goals?

- Specificity: Instead of saying “save more,” define a specific amount you want to save each month or year.

- Actionable Steps: Break down each goal into smaller, manageable steps that you can start working towards.

- Regular Review: Life changes, and so do goals. Make it a habit to revisit and adjust your financial goals together at least annually.

By setting clear, specific, and shared financial goals, you and your partner can create a roadmap for financial success and work together towards achieving your dreams as a team.

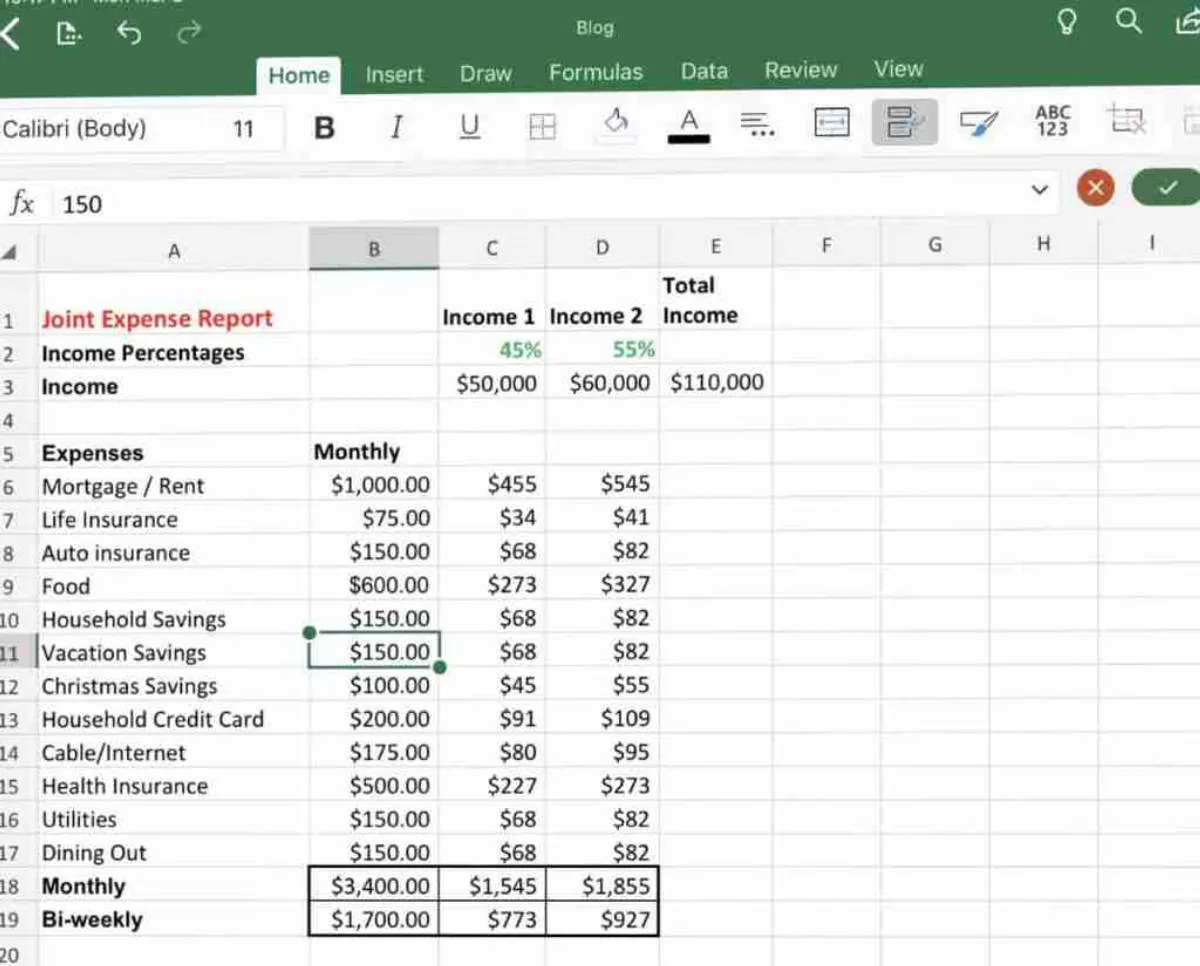

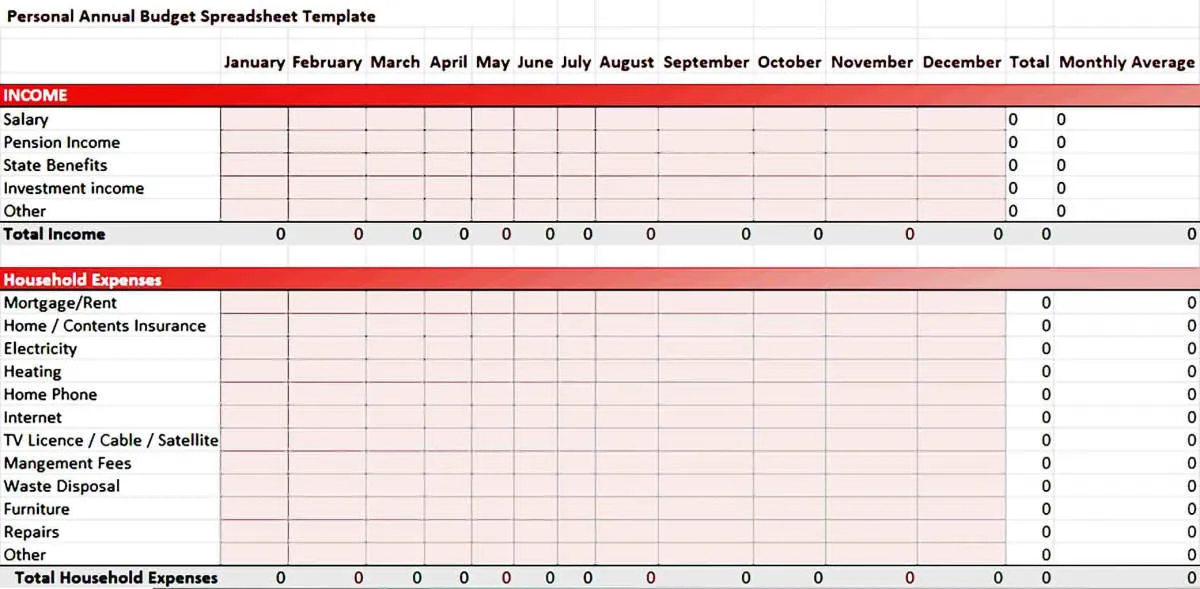

Creating a Joint Budget

One of the cornerstones of a successful financial partnership is a well-planned joint budget. This collaborative tool helps you and your partner align your financial goals, track your income and expenses, and make informed decisions about your money.

Here are some key steps in creating a joint budget:

1. Have an Open and Honest Conversation

Start by discussing your individual financial situations, including income, debts, spending habits, and financial goals. Transparency and honesty are crucial for building trust and creating a realistic budget.

2. Determine Your Combined Income

Calculate your total household income, including salaries, wages, bonuses, investment income, and any other sources of regular income.

3. Track Your Expenses

Keep a detailed record of all your expenses for at least a month. This will give you a clear picture of where your money is going and help you identify areas for potential savings.

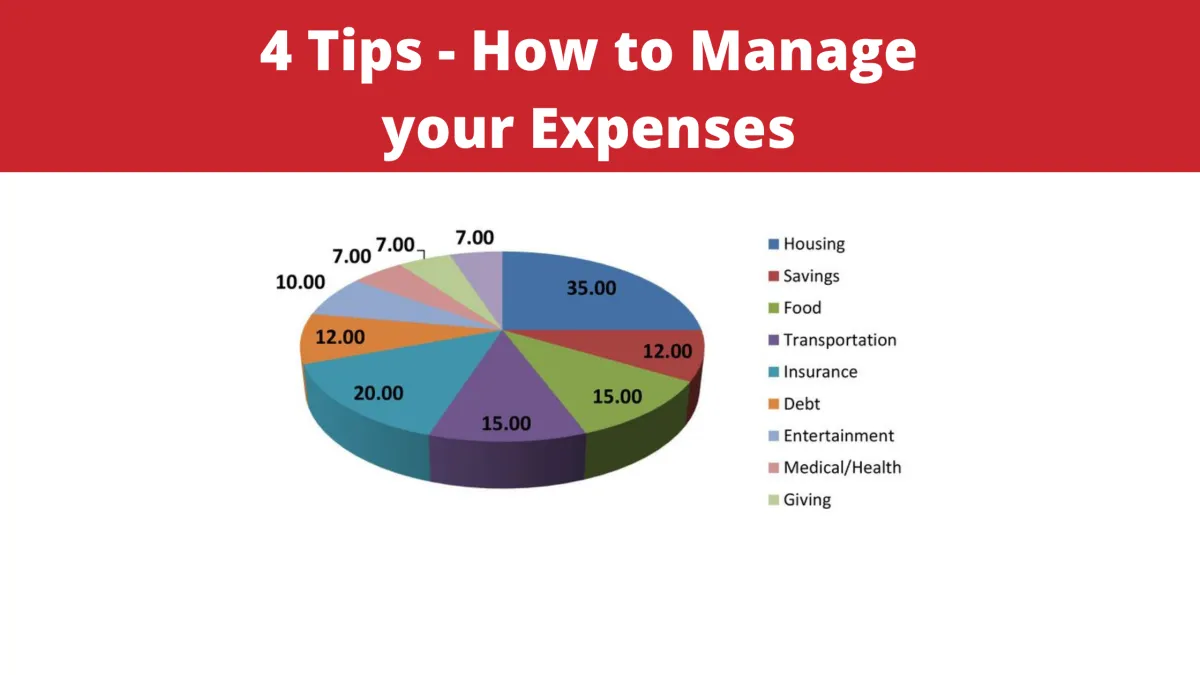

4. Categorize Your Expenses

Group your expenses into categories such as housing, transportation, food, entertainment, and savings. This will help you analyze your spending patterns and allocate your funds effectively.

5. Set Financial Goals

Identify your short-term and long-term financial goals as a couple. This could include saving for a down payment on a house, investing for retirement, or paying off debt. Having shared goals will keep you motivated and aligned.

6. Create a Budgeting Method

Choose a budgeting method that works best for you as a couple, such as the 50/30/20 budget, the envelope system, or zero-based budgeting. The key is to find a system that you both understand and can stick to.

7. Review and Adjust Regularly

Life is constantly changing, and so are your financial circumstances. Review your budget regularly, at least monthly, and make adjustments as needed to ensure you’re staying on track with your goals.

Managing Shared Expenses

One of the cornerstones of a strong financial partnership is open and honest communication about money. This is especially important when it comes to managing shared expenses. Here are some tips for navigating shared finances effectively:

1. Decide on a Method:

Determine how you’ll handle shared expenses. Will you:

- Pool all your income into a joint account? This approach works well for couples who are comfortable with full financial transparency.

- Maintain separate accounts but contribute proportionally to a shared account? This option allows for individual financial autonomy while still covering joint expenses.

- Split bills evenly or based on income? This method requires clear communication about who is responsible for what.

The best method varies depending on your individual circumstances and preferences.

2. Create a Budget:

A joint budget is essential for tracking income, expenses, and financial goals. Outline all sources of income and categorize expenses. Be realistic about spending habits and prioritize needs over wants. A budget provides clarity and helps avoid financial conflicts.

3. Track Spending:

Whether you use budgeting apps, spreadsheets, or a simple notebook, consistent tracking is key. Regularly review your spending as a couple to ensure you’re staying on track and identify any potential areas for adjustment.

4. Communicate Openly:

Regular money conversations are crucial. Discuss financial goals, concerns, and any changes in income or expenses. Honesty and transparency foster trust and prevent misunderstandings.

5. Review and Adjust:

Life is dynamic, and your financial plan should be too. Regularly review your budget and expense-sharing methods, making adjustments as needed to accommodate changes in income, lifestyle, or financial goals.

Building an Emergency Fund

One of the most crucial aspects of financial planning for couples is establishing a robust emergency fund. This fund acts as a financial safety net, providing peace of mind and security during unforeseen circumstances.

Why is an emergency fund so important for couples?

- Job Loss: If one partner experiences a job loss, the emergency fund can cover essential expenses while they search for new employment.

- Medical Emergencies: Unexpected medical bills can put a significant strain on finances. An emergency fund helps cover deductibles, co-payments, and other out-of-pocket expenses.

- Home or Car Repairs: Appliances break down, cars require maintenance—having funds readily available prevents these events from derailing your budget.

- Relationship Stability: Financial stress is a leading cause of conflict in relationships. An emergency fund provides a buffer, reducing anxiety and potential disagreements related to money matters.

How much should couples save in their emergency fund?

A common guideline is to aim for 3-6 months’ worth of living expenses. This amount should be sufficient to cover essential costs like rent or mortgage payments, utilities, groceries, transportation, and debt obligations.

Where to keep your emergency fund:

Liquidity is key for emergency funds. Consider a high-yield savings account or a money market account that offers easy access to your funds when you need them.

Investing for the Future

Building a solid financial future as a couple requires a forward-thinking approach to investing. Here’s what to consider:

Shared Goals, Shared Vision

Before investing a single dollar, align on your long-term goals. Are you saving for a down payment? Retirement? Your children’s education? Defining these objectives will guide your investment strategy.

Risk Tolerance: Finding Common Ground

Discuss your individual risk tolerance levels. Are you both comfortable with market volatility, or does one of you prefer more conservative investments? Striking a balance is key to creating a portfolio that reflects both your comfort levels.

Diversification is Key

Don’t put all your eggs in one basket. Diversifying your investment portfolio across different asset classes (stocks, bonds, real estate, etc.) can help mitigate risk and potentially enhance returns.

Retirement Planning: Starting Early is Key

The power of compounding means that the earlier you start investing for retirement, the better. Explore options like 401(k)s, IRAs, and other retirement savings plans that work best for both of you.

Regular Review and Adjustment

Financial situations change. Regularly review your investment portfolio together, at least annually, and make adjustments as needed based on your goals, risk tolerance, and market conditions.

Understanding Each Other’s Financial Habits

One of the cornerstones of successful financial planning as a couple is open and honest communication about your individual financial habits. Before you can effectively plan for the future, you need to understand where you’re both coming from financially and how you each approach money management.

Start by discussing your individual:

- Spending Habits: Are you a spender or a saver? Do you prioritize experiences or material possessions? Understanding each other’s spending triggers and tendencies can help you anticipate potential conflicts and develop strategies for managing money together.

- Financial Goals: What are your individual short-term and long-term financial goals? Do you dream of owning a home, starting a business, or retiring early? Sharing your aspirations will help you align your financial plans and work towards shared objectives.

- Financial History: Have you made any significant financial decisions in the past, such as taking out loans or making investments? Being transparent about past experiences, both positive and negative, can help build trust and understanding.

- Attitudes Towards Money: How were you raised to think about money? Were your parents savers or spenders? Did you have open conversations about finances growing up? Unpacking your individual money scripts can reveal underlying beliefs and values that influence your financial behavior.

Communicating About Money

Open and honest communication is crucial for couples when it comes to finances. Money is a common source of stress in relationships, so establishing healthy communication patterns early on can prevent misunderstandings and conflicts down the road.

Schedule Regular Money Dates

Set aside dedicated time to discuss finances, ideally in a relaxed and comfortable setting. This could be a weekly or monthly “money date” where you review bills, track spending, and discuss financial goals.

Share Your Financial History

Be transparent about your financial past, including any debts, assets, and spending habits. This helps build trust and understanding between partners.

Discuss Financial Goals

Talk about your individual and shared financial aspirations. Do you want to buy a house, retire early, or travel the world? Aligning your goals will make it easier to create a joint financial plan.

Create a Budget Together

Develop a budget that works for both of you. This involves tracking income and expenses, and allocating funds towards essential needs, savings, and discretionary spending. Collaborating on a budget fosters a sense of shared responsibility.

Establish Clear Responsibilities

Decide who will be responsible for paying bills, managing investments, and tracking expenses. Having designated roles can streamline financial management and reduce the risk of errors or oversights.

Listen Actively and Empathize

When discussing finances, practice active listening and try to understand your partner’s perspective. Avoid interrupting, blaming, or being judgmental. Empathy is key to resolving conflicts and finding solutions that work for both partners.

Planning for Major Expenses

As a couple, you’ll likely face many major expenses together—buying a home, funding a wedding, having children, taking vacations, or planning for retirement. Planning for these expenses together, even if they seem far off, can reduce financial stress and help you achieve your goals faster.

Here are some tips for planning major expenses:

- Define your goals together. Discuss what major expenses you anticipate as a couple and when you might want to achieve them. Make sure you’re on the same page regarding priorities and timelines.

- Create a budget—and stick to it. Track your income and expenses to understand your cash flow. Identify areas where you can cut back to save for your major expenses.

- Set up a dedicated savings account. Automate regular transfers into this account to make saving consistent and less overwhelming. Consider high-yield savings accounts or other investment options to make your money work harder.

- Research and compare costs. Whether it’s a house, a wedding, or a vacation, research and compare prices from different vendors or providers. Don’t be afraid to negotiate for better deals.

- Factor in unexpected expenses. Life throws curveballs. Build an emergency fund to cover unexpected costs and prevent derailing your savings for major expenses.

- Regularly review and adjust. Your financial situation and goals might change over time. Make it a habit to review your plan and adjust your savings strategy as needed.

Protecting Your Assets

When you’re in a relationship, it’s natural to share your life with your partner – and that often includes finances. But it’s crucial to protect what’s yours, both individually and as a couple. Here’s how:

Prenuptial and Postnuptial Agreements

Consider these as your financial safety net, especially important if:

- One partner has significant assets or debts.

- You have children from a previous relationship.

- You’re entering a second or subsequent marriage.

A prenuptial agreement outlines asset division and potential alimony in case of divorce *before* you marry. A postnuptial agreement does the same *after* you’re married. These agreements offer legal clarity and can prevent future disputes.

Joint vs. Separate Accounts

Many couples find a balance with both joint and separate accounts. A joint account can cover shared expenses like rent or mortgage, while individual accounts maintain financial independence. Discuss what works best for your spending and saving habits.

Insurance Coverage

Life can be unpredictable. Having adequate insurance coverage protects both you and your partner. This includes:

- Life insurance: Provides financial security for your partner if you pass away.

- Health insurance: Covers medical expenses and protects against financial strain from unexpected illness.

- Disability insurance: Offers income replacement if you’re unable to work due to an injury or illness.

Estate Planning

Don’t wait until it’s too late. Estate planning ensures your wishes are honored and your assets are distributed according to your desires. It involves:

- Wills: Designates beneficiaries for your assets and appoints a guardian for minor children.

- Trusts: Offer greater control over asset distribution and can minimize estate taxes.

- Power of Attorney: Grants someone the legal authority to make financial and healthcare decisions on your behalf if you become incapacitated.

Seeking Professional Advice

While DIY financial planning can work for some couples, seeking advice from a qualified financial advisor can be incredibly beneficial. A financial advisor can provide:

- Objective Perspective: They can assess your financial situation without emotional bias, helping you make rational decisions.

- Expertise: Financial advisors have in-depth knowledge of investment strategies, tax laws, insurance options, and retirement planning.

- Personalized Plans: They can create a customized financial plan tailored to your specific goals, risk tolerance, and time horizon.

- Ongoing Support: A financial advisor can provide regular check-ins, adjustments to your plan as needed, and answer any questions you have.

When choosing a financial advisor, look for someone who is:

- Certified: Look for designations like Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA).

- Experienced: Choose an advisor with a proven track record of helping couples.

- Trustworthy: You should feel comfortable discussing your financial situation openly and honestly with them.

Remember, financial planning is an ongoing process. Regularly reviewing and adjusting your plan with your advisor will help you stay on track to reach your financial goals together.

Conclusion

Effective financial planning is crucial for couples to achieve their goals and build a secure future together. By communicating openly, setting shared objectives, and managing their finances wisely, couples can navigate financial challenges and strengthen their relationship.

{kind=link}