In the modern world, managing debt effectively is essential for financial stability. This article explores practical strategies and tips to help individuals gain control over their debts and work towards a debt-free future.

Understanding Your Debt

The first step towards effective debt management is understanding what you owe and to whom. This might seem simple, but it’s easy to lose track, especially if you have multiple debts.

Start by creating a list of all your debts. This list should include:

- Creditor: The name of the company or individual you owe money to.

- Debt type: Is it a credit card, student loan, mortgage, auto loan, or something else?

- Total balance: How much do you currently owe?

- Interest rate: This is crucial for prioritization. Higher interest rates mean you’re accruing more debt over time.

- Minimum payment: The minimum amount you need to pay each month to avoid penalties.

- Due date: Mark down when each payment is due to avoid late fees.

Once you have a clear picture of your debts, you can start analyzing them. Ask yourself:

- Which debts have the highest interest rates? These are usually your top priority for repayment.

- Are there any debts you can consolidate? Combining debts can sometimes result in a lower overall interest rate.

- Are there any unnecessary expenses you can cut to free up more money for debt repayment?

Understanding your debt is not about feeling overwhelmed, but about gaining clarity and control. It’s the essential foundation for developing and implementing an effective debt management strategy.

Creating a Repayment Plan

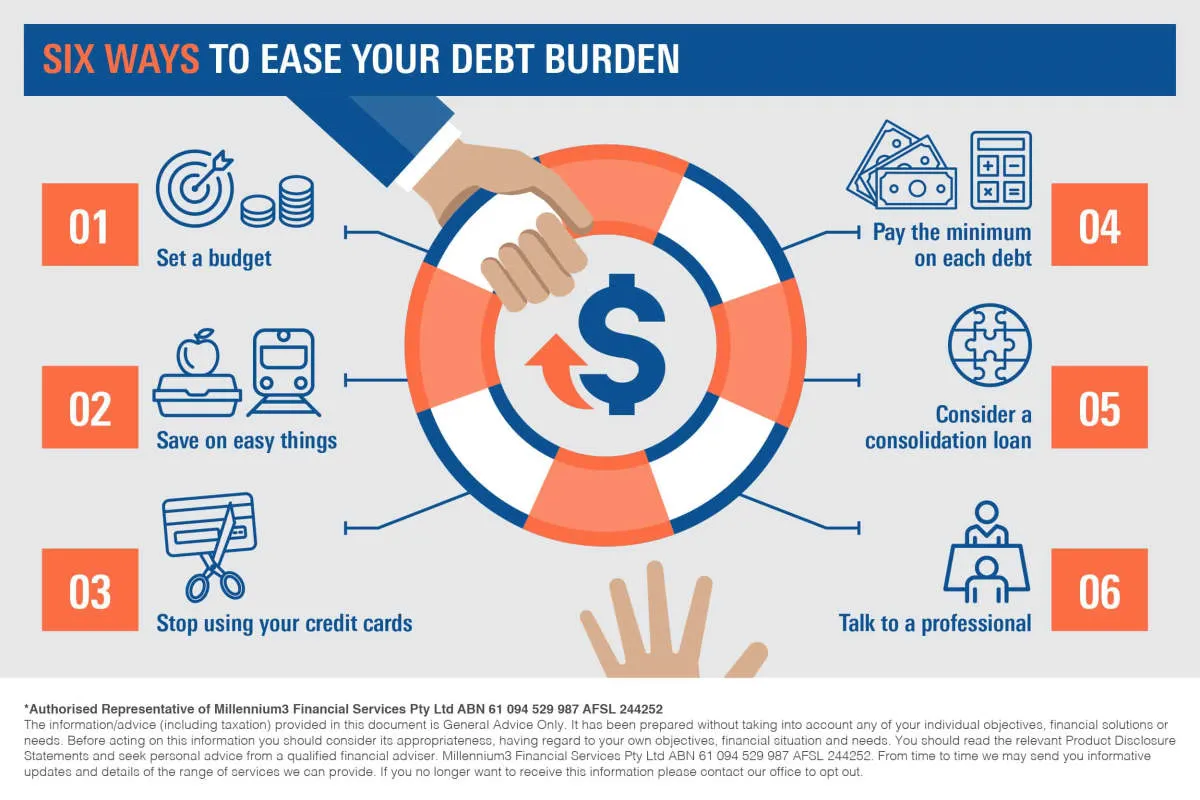

A crucial step in effective debt management is creating a structured repayment plan. This involves understanding your current financial situation, prioritizing debts, and developing a realistic budget that allows for consistent debt repayment.

1. Assess Your Financial Situation

Start by listing all your debts, including credit cards, loans, and any outstanding bills. Note down the interest rates, minimum payments, and total amount owed for each debt. This overview will provide a clear picture of your current debt load.

2. Prioritize Your Debts

It’s generally recommended to prioritize debts with the highest interest rates. This is because high-interest debts accrue more debt over time. Focus on paying more than the minimum payment on these high-priority debts while making minimum payments on other debts.

3. Develop a Realistic Budget

Analyze your income and expenses to create a budget that allocates funds for essential expenses, savings, and debt repayment. Identify areas where you can cut back on spending to free up more money for debt repayment.

4. Explore Debt Consolidation Options

If you have multiple debts with varying interest rates, consider debt consolidation. This involves taking out a new loan to pay off your existing debts, ideally at a lower interest rate. This can simplify your finances and potentially save you money on interest payments.

5. Negotiate with Creditors

Don’t hesitate to contact your creditors and explain your financial situation. They may be willing to negotiate lower interest rates, waive fees, or create a more manageable payment plan. Open communication with creditors can lead to mutually beneficial solutions.

6. Track Your Progress and Adjust as Needed

Regularly monitor your repayment progress. Track your payments, monitor your debt balances, and celebrate milestones. If your financial situation changes, adjust your repayment plan accordingly. Flexibility is key to staying on track with debt management.

Consolidating Your Debt

Debt consolidation is a strategy that involves taking out a new loan to pay off one or more existing debts. This can simplify your finances by giving you a single monthly payment, and it may also help you save money if you can secure a lower interest rate on the consolidation loan.

There are several ways to consolidate debt, including:

- Balance Transfer Credit Cards: These cards offer a low or 0% introductory interest rate for a set period, allowing you to transfer balances from high-interest cards and save on interest charges.

- Personal Loans: You can use a personal loan to pay off multiple debts, such as credit cards, medical bills, or payday loans. Personal loans typically have fixed interest rates and repayment terms.

- Home Equity Loans or Lines of Credit: If you’re a homeowner, you may be able to borrow against the equity in your home to consolidate debt. These options often come with lower interest rates than other types of loans, but they also put your home at risk if you default.

Benefits of Debt Consolidation:

- Simplified debt management with one monthly payment.

- Potential to lower your interest rate and save money.

- Improved credit score by reducing credit utilization.

Considerations Before Consolidating:

- Fees: Some consolidation methods may come with fees, such as balance transfer fees or origination fees for loans.

- Interest Rates: Ensure the new interest rate is lower than your current rates to save money.

- Repayment Terms: Understand the length of the repayment term and how it affects your monthly payments.

Negotiating with Creditors

Direct communication with your creditors is a crucial aspect of debt management. Instead of avoiding their calls, consider these steps for effective negotiation:

1. Be Prepared:

Before contacting your creditors, gather all relevant information, including account statements, payment history, and a clear understanding of your budget and how much you can realistically afford to pay.

2. Communicate Clearly and Respectfully:

Explain your financial situation honestly and politely. Creditors are more likely to work with you if you demonstrate a genuine willingness to repay your debt.

3. Explore Options:

Be prepared to discuss potential solutions, such as:

- Lowering interest rates: Negotiating a reduced interest rate can make your monthly payments more manageable.

- Waiving late fees: If you’ve incurred late fees due to a temporary hardship, ask if they can be waived.

- Setting up a payment plan: Propose a payment plan that aligns with your budget, whether it involves smaller monthly installments or a lump-sum settlement.

4. Get Agreements in Writing:

Once you reach an agreement with a creditor, ensure that all terms are clearly documented in writing to avoid misunderstandings later.

5. Seek Professional Help if Needed:

If you’re uncomfortable negotiating on your own or facing complex debt situations, consider seeking assistance from a reputable credit counseling agency. They can provide guidance and advocate on your behalf.

Using Debt Management Programs

Debt management programs (DMPs) are offered by credit counseling agencies to help individuals consolidate and pay off unsecured debts, such as credit card bills and medical expenses.

Here’s how a DMP typically works:

- Credit Counseling: You’ll start by speaking with a credit counselor who will review your financial situation, including your income, expenses, and debts.

- Debt Negotiation: If you qualify for a DMP, the credit counseling agency will negotiate with your creditors to potentially lower interest rates, waive fees, and create a manageable payment plan.

- Monthly Payments: You’ll make a single monthly payment to the credit counseling agency, and they will distribute the funds to your creditors according to the agreed-upon plan.

Benefits of DMPs:

- Lower interest rates and monthly payments

- Simplified debt repayment with a single monthly payment

- Protection from creditor calls and collection efforts

Considerations for DMPs:

- DMPs typically take 3-5 years to complete.

- Your credit score may be impacted, at least initially.

- You may need to close your existing credit card accounts.

Choosing a Reputable DMP:

It’s crucial to choose a reputable and accredited credit counseling agency. Look for agencies certified by organizations like the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

Avoiding New Debt

While you’re working hard to pay down your existing debt, it’s crucial to avoid taking on any new debt. This might seem daunting, but it’s essential for achieving financial freedom and avoiding a debt spiral.

Here are some tips to help you avoid new debt:

- Create a realistic budget and stick to it. Track your income and expenses, identify areas where you can cut back, and allocate funds for your needs before your wants.

- Live within your means. Avoid impulse purchases and prioritize needs over wants. Before buying something, ask yourself if you truly need it and if it aligns with your financial goals.

- Build an emergency fund. Having a financial safety net can prevent you from relying on credit cards for unexpected expenses like medical bills or car repairs. Aim for 3-6 months’ worth of living expenses.

- Use cash or debit cards instead of credit cards. This will help you stay conscious of your spending and avoid accumulating interest charges.

- Resist temptation. Avoid situations that trigger overspending, such as malls or online shopping. Unsubscribe from tempting promotional emails and limit your exposure to advertising.

- Seek out free or low-cost alternatives for entertainment and leisure. Explore free community events, try out hobbies that don’t require expensive equipment, or borrow books and movies from the library instead of buying them.

- Delay gratification. If you’re considering a significant purchase, wait a few days or weeks before committing. This will give you time to carefully consider the purchase and determine if it’s truly necessary.

- Set financial goals and remind yourself of them often. Having clear financial goals, such as buying a house or retiring early, can motivate you to stay on track and avoid unnecessary debt.

Building an Emergency Fund

A cornerstone of effective debt management is having a safety net to catch you when unexpected expenses arise. This is where an emergency fund comes in. Instead of turning to credit cards or loans when faced with car repairs, medical bills, or job loss, a well-stocked emergency fund provides a financial buffer. This prevents you from accumulating further debt and jeopardizing your financial stability.

How much should you save? A good rule of thumb is to have three to six months’ worth of living expenses saved in a readily accessible account. This ensures you can cover essential costs even during periods of financial strain.

Where should you keep it? Opt for a high-yield savings account or money market account that offers easy access to your funds without risking market volatility.

How to Build Your Emergency Fund:

- Start Small: Even small, consistent contributions add up over time.

- Automate Savings: Set up automatic transfers to your emergency fund on a regular basis.

- Cut Expenses: Identify areas where you can reduce spending and redirect those funds to your emergency fund.

- Windfalls: Deposit any unexpected income, such as tax refunds or bonuses, directly into your emergency fund.

Increasing Your Income

While managing expenses is crucial for debt management, increasing your income can significantly accelerate your debt payoff journey and provide you with more financial breathing room. Here are some strategies to consider:

Negotiate a Raise or Promotion

If you’ve consistently exceeded expectations at your current job, consider negotiating a raise or promotion. Research industry standards for your position and experience level to determine a reasonable salary increase. Prepare a strong case highlighting your accomplishments and the value you bring to the company.

Seek Additional Income Streams

Explore opportunities to generate additional income streams outside of your primary job. This could include:

- Freelancing: Utilize your skills in writing, graphic design, web development, or other areas to offer freelance services.

- Gig Economy: Participate in the gig economy by driving for a ride-sharing service, delivering food, or completing tasks on platforms like TaskRabbit.

- Online Business: Start an online business selling products or services that align with your interests and expertise.

- Passive Income: Explore passive income opportunities such as creating and selling online courses, writing an e-book, or investing in dividend-paying stocks.

Develop In-Demand Skills

Consider acquiring new skills or enhancing existing ones that are in high demand. This could involve taking online courses, attending workshops, or pursuing certifications. Increasing your skillset can make you a more competitive candidate for higher-paying jobs or freelance opportunities.

Turn Your Hobbies into Income

If you have hobbies that you’re passionate about, explore ways to monetize them. For instance, if you enjoy photography, you could sell your prints online or offer photography services for events. If you’re crafty, consider selling your creations at craft fairs or through online marketplaces.

Using Financial Tools

Managing debt effectively often requires utilizing various financial tools designed to provide organization, insight, and control over your finances. These tools can range from simple budgeting apps to more sophisticated debt management software. Here’s how you can leverage them:

1. Budgeting Apps and Software:

Numerous apps and software programs are available to help you track income, expenses, and spending habits. These tools often provide visual representations of your cash flow, making it easier to identify areas where you can cut back and allocate more towards debt repayment.

2. Debt Tracking Spreadsheets:

If you prefer a more hands-on approach, creating a debt tracking spreadsheet can be beneficial. List all your debts, including interest rates, minimum payments, and due dates. This allows you to prioritize high-interest debts and track your progress.

3. Credit Monitoring Services:

Maintaining a good credit score is crucial when managing debt. Credit monitoring services provide regular updates on your credit report, alerting you to any potential errors or signs of identity theft that could impact your creditworthiness.

4. Debt Consolidation Loans:

If you have multiple high-interest debts, consolidating them into a single loan with a lower interest rate can simplify payments and potentially save money. Debt consolidation loans can be obtained from various financial institutions.

5. Financial Calculators:

Online financial calculators can be invaluable for debt management. Use them to estimate monthly payments for different loan terms, compare interest rates, and determine how long it will take to become debt-free using different repayment strategies.

Remember, the key is to find the tools that best suit your needs and preferences. Experiment with different options and utilize those that empower you to manage your debt efficiently and work towards financial freedom.

Seeking Professional Advice

Sometimes, managing debt feels overwhelming, and you might find yourself struggling to stay afloat. In these situations, seeking professional advice is crucial. A financial advisor can provide personalized strategies tailored to your specific financial circumstances.

Benefits of Seeking Professional Advice:

- Debt Consolidation Options: An advisor can help you explore options like debt consolidation loans or balance transfers to simplify your payments and potentially reduce interest rates.

- Budgeting and Financial Planning: They can work with you to create a realistic budget, identify areas for savings, and develop a plan to eliminate debt gradually.

- Negotiating with Creditors: In some cases, a financial advisor can negotiate with your creditors on your behalf to lower interest rates, waive fees, or establish a more manageable payment plan.

- Credit Counseling and Education: Financial advisors can provide valuable insights into credit management, helping you understand your credit score and develop strategies for improvement.

Remember, seeking help is a sign of strength, not weakness. Reaching out to a financial advisor can provide you with the support and expertise needed to navigate the challenges of debt and achieve long-term financial stability.

Conclusion

In conclusion, implementing a combination of budgeting, debt consolidation, and financial planning are effective strategies for debt management, leading to improved financial health and long-term stability.

{kind=link}