Choosing the right credit card can have a significant impact on your financial well-being. In this article, we will explore key factors to consider in order to select a credit card that aligns with your specific needs and lifestyle.

Understanding Credit Card Types

Navigating the world of credit cards can feel like learning a new language. Before you even start comparing interest rates and rewards, it’s crucial to understand the different types of credit cards available. Each caters to specific needs and spending habits. Here’s a breakdown of the most common types:

1. Standard Credit Cards:

These are your everyday, no-frills cards. They usually come with a set credit limit and may or may not offer rewards programs. Standard cards are a good starting point for building credit or for those seeking simplicity.

2. Rewards Credit Cards:

If you’re a savvy spender, rewards cards can be lucrative. They offer points, miles, or cashback on your purchases. Within this category, you’ll find:

- Travel Rewards Cards: Earn miles or points redeemable for flights, hotels, and travel perks.

- Cash Back Cards: Receive a percentage of your spending back as cash rebates.

- Points Cards: Accumulate points redeemable for various rewards, including merchandise, gift cards, and travel.

3. Balance Transfer Credit Cards:

Carrying high-interest debt? Balance transfer cards offer a temporary 0% APR period, allowing you to transfer your existing balances and potentially save on interest charges. Be mindful of balance transfer fees and the regular APR that kicks in after the promotional period.

4. Secured Credit Cards:

Designed for those new to credit or rebuilding their credit history, secured cards require a cash deposit that typically serves as your credit limit. Responsible use of a secured card can help establish a positive credit track record.

5. Student Credit Cards:

Tailored for college students and recent graduates, these cards often have lower credit limits and may offer rewards programs geared towards student life. They can be a helpful tool for building credit early on.

6. Business Credit Cards:

Designed for business owners and their employees, business credit cards help separate business expenses from personal ones, offer higher credit limits, and often include perks like expense tracking features and travel insurance.

Understanding the nuances of each credit card type empowers you to choose a card that aligns with your financial goals and spending patterns.

Comparing Interest Rates and Fees

Interest rates and fees are crucial factors to consider when choosing a credit card. They can significantly impact the overall cost of using your card, so understanding how they work is essential.

Interest Rates:

APR (Annual Percentage Rate) is the yearly interest rate charged on your outstanding balance. It’s crucial to look for a card with a low APR, especially if you plan to carry a balance from month to month.

- Purchase APR: This applies to purchases made with your card.

- Balance Transfer APR: This applies if you transfer a balance from another credit card.

- Cash Advance APR: This usually comes with a higher interest rate and is applied to cash withdrawals from ATMs using your credit card.

Fees:

Credit cards can come with various fees, and it’s essential to understand them before making a decision:

- Annual Fee: Some cards charge an annual fee for the benefits they offer. Consider if the benefits outweigh the cost.

- Balance Transfer Fee: A fee might be charged when you transfer a balance from another card.

- Foreign Transaction Fee: If you travel internationally, be aware of these fees, typically a percentage of each transaction made abroad.

- Late Payment Fee: Charged if you fail to make your minimum payment by the due date.

Pro Tip: Many websites and financial tools allow you to compare credit cards side-by-side. Utilize these resources to compare interest rates, fees, and rewards programs to find the best fit for your spending habits and financial goals.

Considering Rewards Programs

One of the most enticing aspects of credit cards is the opportunity to earn rewards on your spending. Different cards offer different types of rewards programs, each with its own perks and drawbacks. Here’s a closer look at common rewards structures:

1. Cash Back Rewards

As the name suggests, these programs give you a percentage of your spending back as cash. Some cards offer a flat rate on all purchases, while others have rotating bonus categories where you can earn a higher percentage back.

2. Points Rewards

Points programs allow you to accumulate points for every dollar you spend. These points can be redeemed for a variety of rewards, including travel (flights, hotels, rental cars), merchandise, gift cards, or even statement credits. The value of a point can vary depending on the card and how you choose to redeem your rewards.

3. Miles Rewards

Geared towards frequent travelers, miles rewards cards let you earn miles for each dollar spent. These miles can typically be redeemed for flights, hotel stays, and other travel-related expenses. Some cards partner with specific airlines or hotel chains, while others offer more flexibility in how you can use your miles.

4. Evaluating Your Spending Habits

To maximize your rewards, consider where you spend the most money. If you’re a homebody who rarely travels, a travel-focused rewards card might not be the best fit. Analyze your spending patterns to determine which type of program aligns best with your lifestyle.

5. Reading the Fine Print

Rewards programs often come with terms and conditions, so it’s essential to read the fine print. Pay attention to:

- Earning Rates: Understand how much you’ll earn for different purchase categories.

- Redemption Options: Explore how you can use your rewards and any potential limitations.

- Expiration Policies: Check if your rewards expire and if there’s a limit on how many you can accumulate.

- Annual Fees: Some rewards cards come with annual fees. Weigh the cost against the potential rewards to see if it’s worthwhile for you.

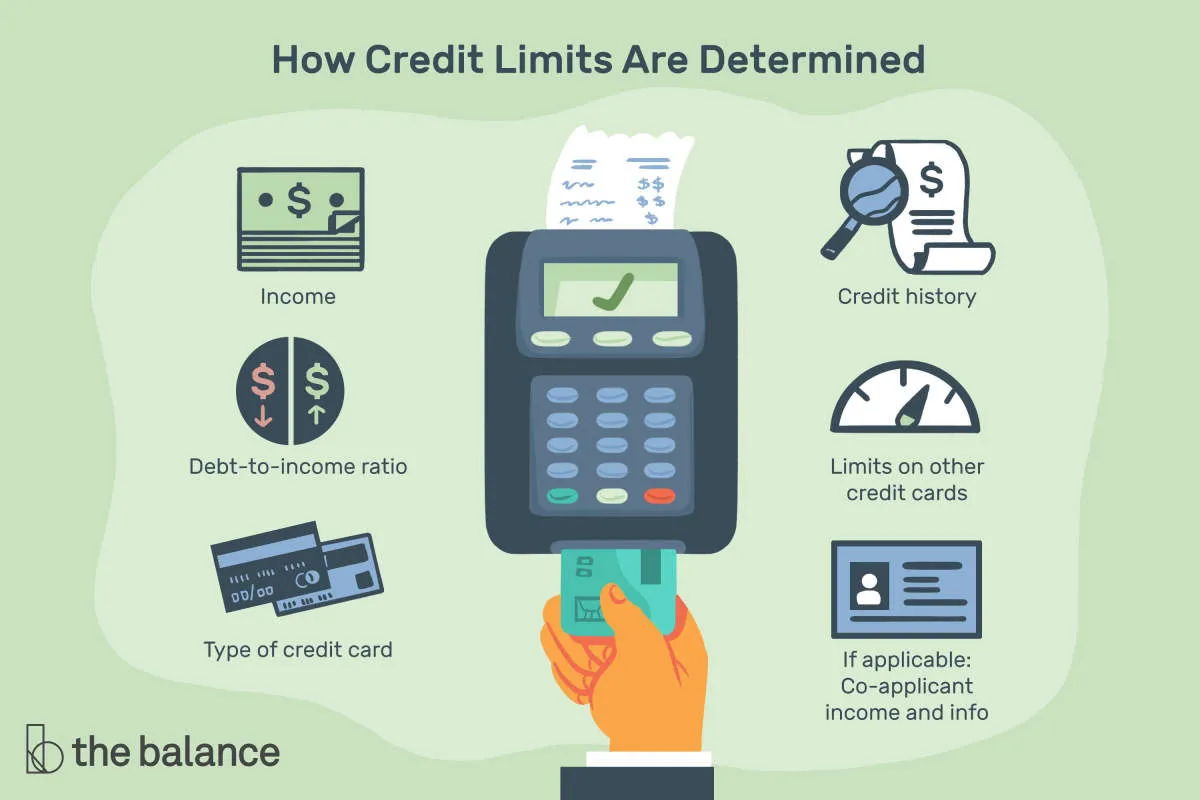

Evaluating Credit Limits

Your credit limit is the maximum amount of money you can borrow on your credit card at any given time. A higher credit limit can be beneficial, but it’s important to choose a limit that aligns with your spending habits and financial goals. Here are key factors to consider when evaluating credit limits:

1. Spending Habits and Needs

Carefully assess your typical monthly expenses and determine how much you realistically need to charge to your credit card. A good rule of thumb is to choose a credit limit that comfortably accommodates your regular spending without exceeding 30% of your total available credit (credit utilization ratio).

2. Credit Score and History

Your credit score and history play a significant role in determining your credit limit. Individuals with excellent credit scores are typically offered higher limits, while those with limited or poor credit may have lower limits. Building a positive credit history through responsible credit card use can increase your chances of securing a higher credit limit in the future.

3. Financial Goals

Consider your financial goals when evaluating credit limits. If you’re aiming to improve your credit score, a lower credit limit can be a good starting point. As you demonstrate responsible credit management, you can request a credit limit increase from your issuer over time.

4. Temptation and Overspending

A high credit limit can be tempting, potentially leading to overspending and debt accumulation. If you tend to overspend or have difficulty managing credit, it’s generally advisable to opt for a lower credit limit that aligns with your spending boundaries.

Reading the Fine Print

Before you hit “apply” on that shiny new credit card offer, take a deep breath and prepare to dive into the fine print. It might seem tedious, but this is where the true cost of the card reveals itself. Here’s what to look for:

Interest Rates (APR)

This is the biggest one. The Annual Percentage Rate (APR) determines how much you’ll be charged in interest on your balance. Look for a card with a low APR, especially if you tend to carry a balance.

Fees

- Annual Fees: Some cards charge an annual fee just for having the card. Consider if the rewards or benefits outweigh this cost.

- Balance Transfer Fees: Planning to transfer a balance from another card? Check the fee, which is usually a percentage of the amount transferred.

- Foreign Transaction Fees: Traveling internationally? Some cards charge a fee for purchases made outside your home country.

- Late Payment Fees: Avoid these at all costs by setting up autopay or reminders to pay on time.

Other Terms and Conditions

Don’t gloss over the rest of the fine print! Look for details like:

- Grace Period: This is the amount of time you have to pay your balance in full before interest is charged.

- Penalty APR: Your interest rate can skyrocket if you make a late payment or miss a minimum payment. Know what triggers this and what the new APR will be.

- Rewards Program Rules: If you’re choosing a rewards card, be clear on how you earn and redeem points, miles, or cash back. Are there limitations or blackout dates?

Choosing Based on Your Spending Habits

Your spending habits are key to finding a credit card that truly fits your lifestyle. Different cards reward different types of spending. Think about your regular expenses and prioritize accordingly:

1. The Everyday Spender:

If you use your credit card for most purchases like groceries, gas, and recurring bills, a cash back or rewards points card on general spending is ideal. Look for cards offering:

- High cashback percentage (e.g., 1.5%-2% on all purchases)

- Bonus rewards at common retailers (e.g., grocery stores, gas stations)

2. The Frequent Flyer:

For those who travel often, travel rewards cards are your best bet. These cards offer:

- Miles or points earned per dollar spent, redeemable for flights, hotels, and travel perks

- Perks like airport lounge access, free checked bags, and travel insurance

3. The Dining Enthusiast:

Love trying new restaurants or ordering in frequently? A dining rewards card could be perfect. Benefits often include:

- Elevated rewards points at restaurants (e.g., 3x-5x points)

- Dining credits or discounts at partner restaurants

4. The Big Spender:

If you have high monthly expenses, a premium rewards card can offer significant value. However, these cards typically come with:

- Higher annual fees

- Large sign-up bonuses requiring significant spending to unlock

- Access to luxury perks and benefits (e.g., concierge services, travel credits)

Understanding Credit Card Terms

Before you even think about APRs or rewards programs, you need a firm grasp of basic credit card terminology. This will help you decipher the fine print and make informed decisions about which card aligns best with your spending habits and financial goals.

Key Terms to Know:

- Annual Percentage Rate (APR): This is the cost of borrowing money on your credit card, expressed as a yearly percentage. A lower APR means you’ll pay less in interest charges.

- Balance Transfer: This involves moving your existing credit card debt from one card to another, often to take advantage of a lower introductory APR.

- Credit Limit: This is the maximum amount you’re allowed to borrow on your credit card. It’s important to stay well below this limit to maintain a healthy credit utilization ratio.

- Grace Period: This is the timeframe between the end of your billing cycle and when your payment is due, during which you can pay your balance in full and avoid interest charges.

- Minimum Payment: This is the lowest amount you can pay each month to keep your account in good standing. However, consistently making only the minimum payment will keep you in debt longer and cost you more in interest.

- Annual Fee: Some credit cards charge an annual fee for the privilege of using their card and its perks. Consider whether the benefits outweigh the cost before signing up for a card with an annual fee.

- Rewards Programs: Many credit cards offer rewards such as cash back, points, or miles for your spending. Evaluate your spending habits to see which type of rewards program best suits your needs.

- Foreign Transaction Fees: If you travel internationally, be aware of these fees, which are charged for purchases made outside of your home country.

Take the time to thoroughly read and understand the terms and conditions associated with each credit card you’re considering. If anything is unclear, don’t hesitate to contact the credit card issuer for clarification.

Applying for a Credit Card

Once you’ve researched and compared different credit cards and found one that aligns with your needs and financial situation, it’s time to apply. Here’s a step-by-step guide to navigating the application process:

1. Gather Your Information

Before you start the application, collect the necessary documents and information, including:

- Social Security number

- Government-issued photo ID

- Proof of income (pay stubs, tax returns)

- Housing information (rent or mortgage payments)

2. Complete the Application

Most credit card applications can be completed online through the issuer’s website. You’ll need to provide the information you gathered, as well as details about your employment history and credit history. Be sure to review all information carefully for accuracy before submitting.

3. Review and Submit

Before hitting the submit button, double-check all the information you’ve provided. Any errors or inaccuracies could delay the application process or even lead to a denial. Once you’re certain everything is correct, submit your application.

4. Wait for a Decision

Credit card issuers typically make decisions on applications fairly quickly. You might receive an instant decision online, or you might have to wait a few days to a couple of weeks for a response by mail.

5. If Approved

Congratulations! If you’re approved, you’ll receive your credit card in the mail within 7-10 business days. Once it arrives, you’ll need to activate it before you can start using it. Be sure to review the card’s terms and conditions, including interest rates, fees, and rewards programs.

6. If Denied

Don’t worry – a credit card denial isn’t the end of the world. You’re entitled to a free copy of your credit report if you were denied based on information in it. Review your report carefully for any errors and dispute any inaccuracies with the credit bureau. You can also contact the issuer to ask why your application was denied and what steps you can take to improve your chances in the future.

Using Credit Cards Responsibly

Choosing the right credit card is an important step, but equally crucial is using it responsibly. Misusing credit cards can lead to debt and damage your credit score. Here’s how to manage your credit cards effectively:

1. Treat it Like a Debit Card:

Imagine your credit card as a debit card linked directly to your bank account. Only spend what you can afford to pay back in full when the bill arrives. This practice helps prevent overspending and accumulating debt.

2. Pay Your Balance in Full and On Time:

Avoid paying only the minimum payment due, as this can lead to a cycle of debt due to high interest charges. Strive to pay your balance in full by the due date to save on interest and maintain a good credit score.

3. Track Your Spending:

Regularly review your credit card statements to track your spending habits. Identify areas where you can cut back and ensure all transactions are accurate. Consider using budgeting apps or tools to help you monitor your expenses.

4. Maintain a Low Credit Utilization Ratio:

Your credit utilization ratio is the amount of credit you use compared to your total available credit. It’s recommended to keep this ratio below 30% to demonstrate responsible credit management to lenders. For example, if your credit limit is $10,000, aim to keep your balance below $3,000.

5. Avoid Cash Advances:

Cash advances from credit cards typically come with higher interest rates and additional fees. It’s best to avoid them unless absolutely necessary. Explore alternative options like personal loans if you require immediate cash.

6. Limit the Number of Credit Cards:

Having too many credit cards can complicate your finances and potentially lead to overspending. Focus on managing a few cards responsibly rather than juggling multiple accounts.

Monitoring Your Credit Card Activity

Regularly monitoring your credit card activity is crucial for maintaining healthy finances and protecting yourself from fraud. Here’s how you can stay on top of your credit card usage:

1. Review Statements Carefully

Don’t just look at the minimum payment due. Examine each transaction on your statement to ensure you recognize and authorize it. Pay attention to the date, merchant name, and amount.

2. Online and Mobile Banking

Most credit card issuers offer online platforms and mobile apps for real-time tracking. Utilize these tools to check your balance, available credit, and recent transactions whenever convenient.

3. Set Up Account Alerts

Opt for alerts from your credit card provider to receive notifications about suspicious activity, approaching credit limits, or payment due dates. This proactive approach can help you catch issues early on.

4. Check Your Credit Report

Get into the habit of checking your credit report regularly for any inaccuracies or signs of fraudulent activity. You can obtain a free credit report from each of the three major credit bureaus annually.

5. Report Discrepancies Immediately

If you notice any unauthorized transactions or errors on your statement, report them to your credit card issuer immediately. Acting quickly can minimize potential losses and aid in resolving the issue promptly.

Conclusion

Choosing the right credit card is essential for managing your finances effectively. Consider your spending habits, rewards, fees, and interest rates carefully to find a card that aligns with your needs and goals.

{kind=link}