Choosing the right credit card can make a big difference in managing your finances effectively. In this comprehensive guide, we will explore essential factors to consider when selecting the best credit card to meet your specific needs and lifestyle.

Understanding Credit Card Types

Before diving into the specifics of choosing a credit card, it’s crucial to grasp the different types available, as each caters to varying financial needs and spending habits.

1. Rewards Credit Cards

These cards are designed to give back to the spender. They offer rewards in the form of:

- Cashback: Earn a percentage of your spending back as cash rebates.

- Points: Accumulate points on purchases, redeemable for travel, merchandise, or statement credits.

- Miles: Ideal for frequent flyers, these cards reward spending with airline miles.

Within rewards cards, there are variations like flat-rate cards offering consistent rewards on all purchases and tiered rewards cards offering higher rewards in specific spending categories like dining or travel.

2. Travel Credit Cards

Designed for travel enthusiasts, these cards offer benefits like:

- Travel rewards: Earn miles or points redeemable for flights, hotels, and rental cars.

- Travel insurance: Complimentary insurance coverage for trip cancellations, lost luggage, or travel accidents.

- Airport lounge access: Enjoy complimentary access to airport lounges for a more comfortable travel experience.

3. Balance Transfer Credit Cards

These cards help you manage existing debt with features like:

- Introductory 0% APR: Enjoy a period of 0% interest on balance transfers, allowing you to pay down debt faster.

Before opting for balance transfers, understand the balance transfer fees and the duration of the 0% APR period.

4. Secured Credit Cards

Ideal for building or rebuilding credit, these cards require a security deposit that typically serves as your credit limit. Responsible use helps establish a positive credit history.

5. Student Credit Cards

Designed for students with limited credit history, these cards offer lower credit limits and potential rewards or cashback programs to encourage responsible spending habits.

6. Business Credit Cards

Tailored for business expenses, these cards offer features like employee cards, higher credit limits, and rewards tailored for business spending, such as office supplies or travel.

Comparing Interest Rates and Fees

Interest rates and fees are crucial factors to consider when choosing a credit card. They directly impact the overall cost of using the card and can significantly affect your financial well-being.

Interest Rates

Annual Percentage Rate (APR) is the annual cost of borrowing money on your credit card. It’s expressed as a percentage and includes both the interest rate and certain fees.

- Purchase APR: Applied to purchases made with the card.

- Balance Transfer APR: Applied to balances transferred from other credit cards.

- Cash Advance APR: Applied to cash withdrawals made with the card.

Lower APRs are generally better as they result in lower interest charges. Look for cards with competitive APRs that align with your spending and payment habits.

Fees

Credit cards often come with various fees, which can add up quickly if you’re not careful. Some common fees include:

- Annual Fee: Charged annually for using the card.

- Balance Transfer Fee: Charged for transferring a balance from another credit card.

- Cash Advance Fee: Charged for withdrawing cash with the card.

- Late Payment Fee: Charged if you make a payment after the due date.

- Foreign Transaction Fee: Charged for transactions made outside of your home country.

Carefully review the fee schedule of each credit card you’re considering. Choose a card with low or no fees that align with your spending patterns.

Considering Rewards Programs

One of the most enticing aspects of credit cards is the potential to earn rewards on your spending. However, not all rewards programs are created equal, and the best one for you depends on your spending habits and preferences.

Types of Rewards Programs:

- Cash Back: These programs offer a straightforward reward – a percentage of your spending back as cash. Some cards offer a flat rate on all purchases, while others offer higher rates in specific categories.

- Points: Points programs allow you to accumulate points for every dollar spent. These points can be redeemed for a variety of rewards, such as travel, merchandise, gift cards, or even statement credits.

- Miles: Ideal for frequent travelers, miles programs reward you with miles for every dollar spent. These miles can be redeemed for flights, hotel stays, and other travel-related expenses.

Evaluating Rewards:

- Earning Rates: Compare the earning rates offered by different cards. Look for cards that offer higher rewards in categories where you spend the most.

- Redemption Options: Consider the flexibility and value of the redemption options. Are you limited to specific airlines or hotels for travel rewards? What is the cash equivalent of points or miles?

- Bonus Categories and Rotating Categories: Some cards offer bonus rewards in rotating categories throughout the year. Ensure these categories align with your spending habits to maximize your rewards.

- Sign-Up Bonuses: Many cards offer attractive sign-up bonuses for spending a certain amount within the first few months. Factor in these bonuses when comparing cards, but don’t let them be the sole deciding factor.

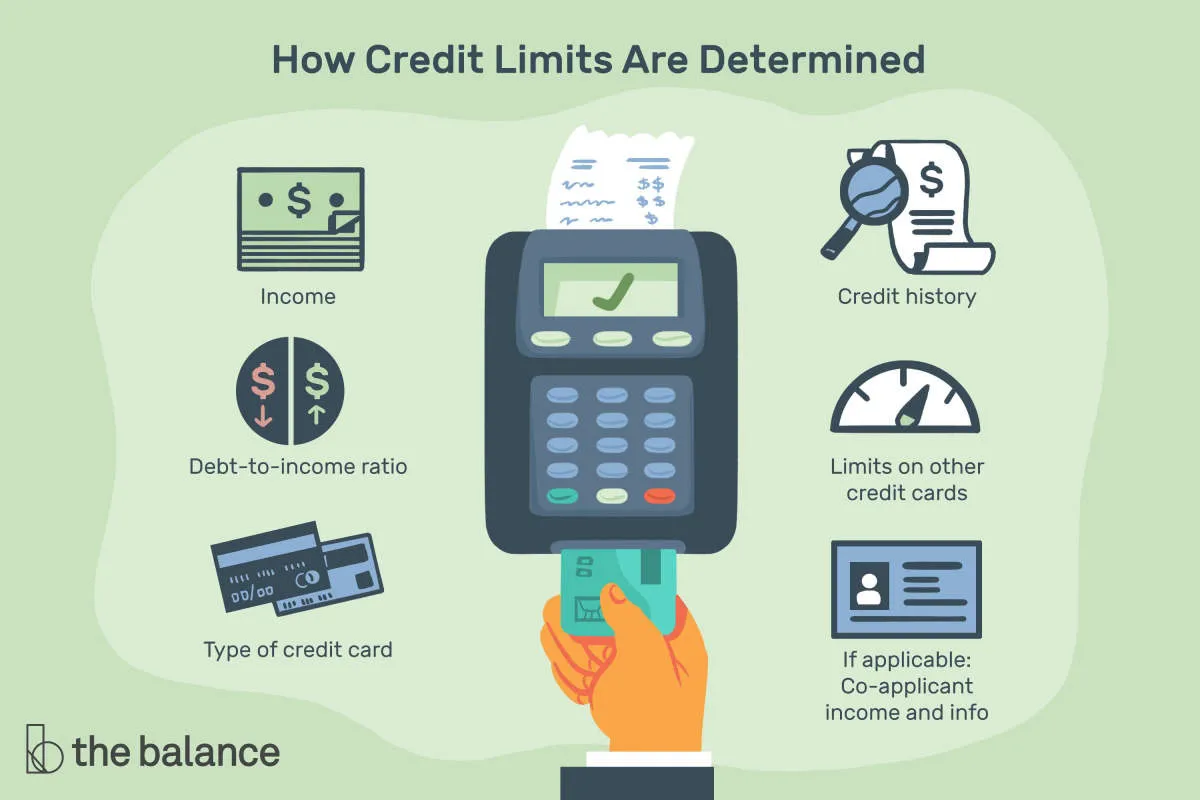

Evaluating Credit Limits

Your credit limit is the maximum amount of money you can borrow on your credit card at any given time. It’s a crucial factor to consider when choosing a credit card because it directly impacts your purchasing power and, potentially, your credit score.

Understanding Credit Utilization

Credit utilization is the ratio of your credit card balance to your credit limit. It’s a significant factor in your credit score, and keeping it low is essential for maintaining a good credit rating. A lower credit utilization rate indicates to lenders that you’re managing your credit responsibly.

Factors Influencing Your Credit Limit

Credit card issuers determine your credit limit based on several factors, including:

- Credit Score: A higher credit score generally leads to a higher credit limit, as it suggests a lower risk of default.

- Income: Lenders consider your income to assess your ability to repay your debts. A higher income may result in a higher credit limit.

- Existing Debt: If you have significant existing debt, lenders may be hesitant to offer you a high credit limit.

- Credit History: A long and positive credit history demonstrates responsible credit management, which can lead to higher credit limits.

The Importance of Choosing a Suitable Credit Limit

Choosing a credit card with a credit limit that aligns with your spending habits and financial situation is crucial. Requesting a credit limit increase or decrease might be necessary as your financial circumstances evolve.

Reading the Fine Print

While enticing rewards and low introductory rates might catch your eye, it’s crucial to delve into the fine print of any credit card offer. This section often holds critical details that could significantly impact your financial well-being. Here’s what to scrutinize:

APR (Annual Percentage Rate)

Don’t just focus on the introductory APR. Pay close attention to the regular APR that kicks in after the introductory period ends. This rate determines the interest charged on your outstanding balance, so a lower APR translates to lower interest payments.

Fees

Credit cards can come with various fees, including:

- Annual fees: A yearly charge for simply holding the card.

- Balance transfer fees: Charged when transferring balances from other credit cards.

- Cash advance fees: Applied to cash withdrawals using your credit card.

- Late payment fees: Imposed for missing the payment due date.

- Foreign transaction fees: Charged on purchases made outside your home country.

Carefully review the fee schedule to understand the potential costs associated with the card.

Penalty APR

This higher interest rate can be triggered by actions like late payments or exceeding your credit limit. Understand the conditions that could lead to a penalty APR and its impact on your balance.

Rewards and Benefits Terms

If you’re drawn to a card for its rewards program, examine the terms carefully. Understand:

- Earning rates: How many points or miles per dollar spent?

- Redemption options: How can you use your rewards? Are there limitations or restrictions?

- Expiration policies: Do your rewards expire?

Make sure the rewards structure aligns with your spending habits and redemption preferences.

Choosing Based on Your Spending Habits

Your spending habits are a major factor in determining the best credit card for you. Different cards reward different types of spending, so aligning your card choice with your spending patterns can maximize your rewards and benefits. Consider the following:

1. High Spenders

If you tend to have high monthly expenses, focus on cards with high cashback or rewards rates. Look for cards that offer:

- Unlimited cashback on all purchases.

- High rewards rates in categories where you spend the most, such as dining, travel, or groceries.

- Annual fee waivers or perks that outweigh the cost of the fee.

2. Category-Focused Spenders

If you consistently spend heavily in specific categories, such as groceries or gas, opt for a card that offers:

- Bonus rewards on specific spending categories, like 5% back on groceries or 3% back on gas.

- Rotating bonus categories that align with your spending patterns.

3. Travelers

For frequent travelers, prioritize cards with:

- Travel rewards programs that allow you to earn points or miles redeemable for flights, hotels, and other travel expenses.

- Travel perks such as airport lounge access, free checked bags, or travel insurance.

- No foreign transaction fees for international purchases.

4. Budget-Conscious Consumers

If you’re working on building credit or prefer simplicity, consider cards with:

- Low or no annual fees to minimize costs.

- Straightforward rewards programs like flat-rate cashback.

- Tools and resources to help you track spending and manage your credit responsibly.

Understanding Credit Card Terms

Before you start comparing credit cards, it’s crucial to understand the common terms and conditions associated with them. This knowledge will help you make informed decisions and choose a card that aligns with your spending habits and financial goals.

Key Credit Card Terms

Here are some important credit card terms you should be familiar with:

- Annual Percentage Rate (APR): This is the yearly interest rate charged on your credit card balance. It’s essential to look for a card with a low APR, especially if you plan to carry a balance.

- Credit Limit: This is the maximum amount you can borrow on your credit card. A higher credit limit can be beneficial, but it’s crucial to use it responsibly.

- Minimum Payment: This is the minimum amount you need to pay each month to avoid late fees. However, making only the minimum payment will result in paying more interest and taking longer to pay off your balance.

- Grace Period: This is the time you have to pay your balance in full before interest is charged. Typically, it’s around 21 days from the statement closing date.

- Balance Transfer: This allows you to transfer your existing credit card debt to another card, often with a lower introductory APR. This can save you money on interest charges.

- Cash Advance: This allows you to withdraw cash from an ATM using your credit card. However, cash advances typically have higher APRs and fees compared to purchases.

- Rewards Programs: Many credit cards offer rewards programs, such as cashback, travel points, or miles. Consider your spending habits and choose a card that offers rewards aligned with your preferences.

- Fees: Credit cards may come with various fees, including annual fees, balance transfer fees, cash advance fees, and late payment fees. It’s essential to be aware of these fees before applying for a card.

Applying for a Credit Card

Once you’ve compared different credit cards and found one that aligns with your needs and financial situation, it’s time to apply. Here’s a step-by-step guide to navigate the application process:

1. Gather Your Information

Before starting the application, gather the necessary information, including:

- Social Security number

- Date of birth

- Current address

- Employment information (employer name, income)

- Housing information (rent/own, monthly payment)

2. Check Your Credit Score

Your credit score plays a significant role in credit card approval. Obtain a free credit report from annualcreditreport.com to assess your creditworthiness and identify any potential issues that might impact your application.

3. Complete the Application

Visit the credit card issuer’s website or contact them directly to access the application form. Fill out the application accurately and completely, providing all requested information.

4. Review and Submit

Before submitting your application, carefully review all the information you’ve provided to ensure accuracy. Double-check for any errors or omissions. Once you’re confident, submit your application.

5. Wait for a Decision

After submitting your application, the credit card issuer will review your information and make a decision. The time it takes to receive a decision varies, ranging from instant approval to several weeks. You’ll be notified of the decision by mail or email.

Using Credit Cards Responsibly

Choosing the right credit card is an important step, but using it responsibly is crucial for building healthy financial habits. Here’s how to make the most of your credit card while avoiding common pitfalls:

1. Treat it Like a Debit Card:

The golden rule of responsible credit card use is to only spend what you can afford to repay when the bill arrives. Imagine your credit card as a debit card directly linked to your checking account. This mindset will help you avoid overspending and accumulating debt.

2. Pay Your Balance in Full and on Time:

Credit card interest rates can be high. To avoid paying unnecessary interest charges, aim to pay your balance in full by the due date each month. This practice saves you money and contributes to a good credit score.

3. Track Your Spending:

Credit cards can make it easy to overspend if you’re not careful. Monitor your transactions regularly, either through your bank’s mobile app or by reviewing your monthly statements. This awareness helps you stay within budget and identify any potential issues early on.

4. Understand Your Credit Limit:

Your credit limit is the maximum amount you’re allowed to borrow on your card. It’s essential to keep your spending well below this limit. Maxing out your credit card can negatively impact your credit score and make it seem like you’re financially overextended.

5. Resist Impulse Purchases:

Credit cards can make impulse buys tempting, but it’s important to pause and consider the necessity of a purchase before swiping your card. Ask yourself if you truly need the item and if it aligns with your budget.

Monitoring Your Credit Card Activity

Regularly monitoring your credit card activity is crucial for maintaining good financial health and protecting yourself from fraud. Here’s why it’s important and how to do it effectively:

Why It’s Essential

- Early Fraud Detection: Catching unauthorized transactions quickly minimizes your liability and prevents further damage.

- Spot Errors: Identify billing mistakes, incorrect charges, or duplicate transactions that need correction.

- Track Spending Habits: Monitoring helps you understand your spending patterns, enabling better budget control.

- Maintain Good Credit: Addressing issues promptly, like late payments, protects your credit score.

How to Monitor Effectively

- Review Statements Carefully: Go through your monthly statement line by line, checking for any discrepancies.

- Utilize Online and Mobile Banking: Most banks offer online platforms and apps to track transactions in real-time.

- Set Up Account Alerts: Configure notifications for transactions above a certain amount, international purchases, or cash withdrawals.

- Check Your Credit Report: Review your credit report periodically for any suspicious activity or accounts you don’t recognize. You can access your credit report for free from the major credit bureaus.

Conclusion

Choosing the best credit card involves considering your spending habits, rewards preferences, and financial goals. Conduct thorough research to select a card that aligns with your needs and offers the most benefits.

{kind=link}