Choosing the right bank account is essential for managing your finances effectively. This article will guide you through the steps to find a bank account that suits your specific needs and goals.

Types of Bank Accounts

When it comes to managing your money, choosing the right bank account is crucial. Different accounts cater to different financial needs and goals. Here’s a breakdown of the most common types of bank accounts:

Checking Accounts

Checking accounts are designed for your everyday financial transactions. They offer easy access to your funds through:

- Debit cards

- Checks

- Online and mobile banking

- ATM withdrawals

Key features of checking accounts:

- Liquidity: Deposit and withdraw funds easily.

- Convenience: Manage bills, make purchases, and access cash conveniently.

- Some accounts may offer interest, though rates are typically low.

Savings Accounts

Savings accounts are designed to help you save money and earn interest. They typically offer higher interest rates than checking accounts, making them ideal for:

- Emergency funds

- Short-term savings goals

- Money you don’t need for immediate expenses

Key features of savings accounts:

- Interest-bearing: Earn interest on your balance.

- Safety and security: FDIC-insured up to $250,000 per depositor, per insured bank.

- Limited access: Some accounts may have restrictions on withdrawals.

Money Market Accounts (MMAs)

MMAs combine features of both checking and savings accounts. They offer higher interest rates than checking accounts and provide some check-writing privileges, though typically with limitations.

Key features of MMAs:

- Competitive interest rates

- Check-writing privileges (usually limited)

- Debit card access

- Higher minimum balance requirements than checking or savings accounts

Certificates of Deposit (CDs)

CDs offer a fixed interest rate over a set period, ranging from a few months to several years. They’re ideal for those seeking a safe investment with a guaranteed return.

Key features of CDs:

- Fixed interest rates

- Guaranteed returns

- Limited access: Funds are locked in for the CD term, and early withdrawals incur penalties.

Understanding Fees

Not all bank accounts are created equal, especially when it comes to fees. It’s crucial to understand the various fees associated with different accounts to avoid unexpected surprises and keep your hard-earned money in your pocket.

Here are some common bank fees to watch out for:

- Monthly maintenance fees: Some accounts charge a recurring fee simply for keeping your money there. This fee can often be waived by maintaining a minimum balance or meeting specific transaction requirements.

- ATM fees: Withdrawing money from an ATM outside your bank’s network can result in hefty fees. Look for accounts offering a wide ATM network or reimbursements for out-of-network ATM fees.

- Overdraft fees: Spending more money than you have in your account will trigger an overdraft fee. Consider opting for overdraft protection or linking a savings account to minimize these charges.

- Foreign transaction fees: Using your debit card internationally can incur additional fees. If you travel frequently, consider an account with low or no foreign transaction fees.

- Inactivity fees: Some accounts penalize you for not using your account regularly. Be mindful of these fees if you plan to open an account with infrequent use.

Carefully review the fee schedule for any bank account you’re considering. Compare fees across different banks and choose an account that aligns with your spending habits and financial goals.

Interest Rates and Benefits

Interest rates are a crucial factor to consider when choosing a bank account. Different accounts offer varying interest rates, which can significantly impact your savings growth.

High-yield savings accounts typically offer more competitive interest rates compared to traditional savings accounts. These accounts are designed to help your money grow faster, making them ideal for long-term savings goals.

Checking accounts, on the other hand, generally offer lower interest rates or none at all. However, some checking accounts may provide minimal interest on balances, especially those with higher minimum balance requirements.

In addition to interest rates, it’s essential to consider the benefits associated with different bank accounts. Some common benefits include:

- ATM fee reimbursements: Some banks offer to reimburse ATM fees charged by other institutions, providing convenience and cost savings.

- Mobile banking features: Look for accounts that offer user-friendly mobile apps with features like mobile check deposit, bill pay, and account alerts.

- Rewards programs: Certain banks offer rewards programs that allow you to earn points or cash back on your debit card purchases.

Carefully evaluate the interest rates and benefits offered by different banks and accounts to determine the best fit for your financial needs and goals.

Online vs. Traditional Banks

When considering how to choose the right bank account, one of the first decisions you’ll face is whether to go with an online or traditional bank. Both options offer a variety of checking and savings accounts, but they differ in key aspects:

Online Banks

Pros:

- Higher interest rates on savings accounts and CDs. Since online banks don’t have the overhead of physical branches, they can offer more competitive interest rates.

- Lower fees. Online banks are known for having lower or no monthly maintenance fees, overdraft fees, and ATM fees.

- 24/7 access and convenience. Manage your account, deposit checks, and pay bills from anywhere with internet access.

Cons:

- Lack of in-person banking. You won’t have the option to visit a branch to speak with someone face-to-face or make cash deposits.

- Potential for security concerns. While online banks employ robust security measures, some individuals may feel more comfortable with the perceived security of traditional banks.

Traditional Banks

Pros:

- In-person banking experience. Visit a branch to open an account, speak with a teller or banker, make deposits, and access other financial services.

- Established reputation and trust. Traditional banks have a long history and are often seen as more secure and reliable.

- Wide range of services. Access a broader range of financial products and services, such as loans, mortgages, and investment accounts.

Cons:

- Lower interest rates and higher fees. Traditional banks generally offer lower interest rates on savings accounts and higher fees compared to online banks.

- Less convenient. You may need to visit a branch during business hours for certain transactions, which may not be convenient for everyone.

How to Open a Bank Account

Once you’ve compared different banks and accounts and found the right one for your needs, it’s time to open your account. Here’s a step-by-step guide:

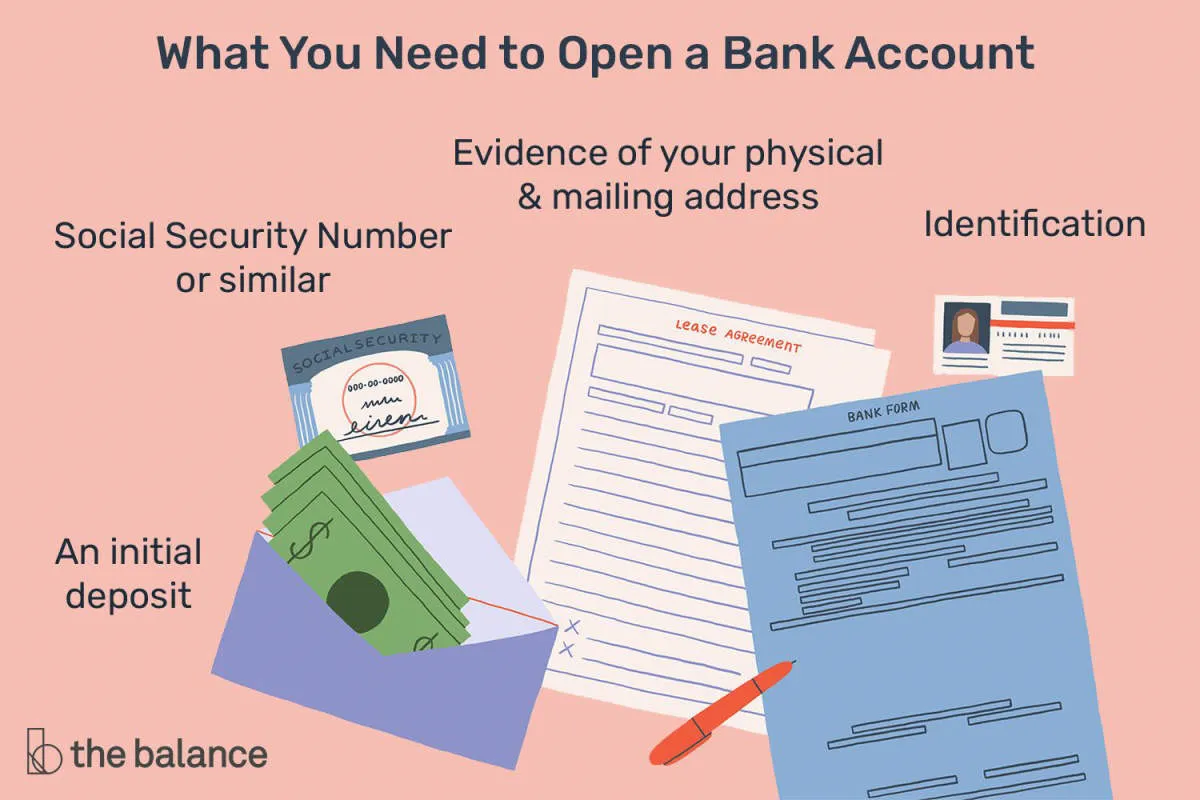

1. Gather Your Information

Before you begin the application process, gather the necessary information, which typically includes:

- Valid government-issued photo ID: This could be your driver’s license, passport, or state ID.

- Social Security number: You’ll need to provide your SSN for identification and tax purposes.

- Proof of address: This could be a utility bill, lease agreement, or bank statement.

- Initial deposit: Most banks require an initial deposit to open an account, which can vary depending on the account type.

2. Choose Your Application Method

You can usually open a bank account in one of three ways:

- Online: Many banks allow you to open an account entirely online through their website.

- In person: You can visit a local branch of the bank to open an account with the assistance of a bank representative.

- Over the phone: Some banks may allow you to open an account by calling their customer service line.

3. Complete the Application

Regardless of your chosen method, you’ll need to complete an application form. This will involve providing your personal information, choosing an account type, and setting up your account access (online banking, debit card, etc.).

4. Fund Your Account

Once your application is approved, you’ll need to make your initial deposit. This can often be done online, in person, or by mail.

5. Receive Your Account Information

After your account is funded, the bank will provide you with your account number, routing number, and any other relevant information. You’ll typically receive your debit card and PIN by mail within a few business days.

Managing Your Bank Account

Once you’ve chosen the right bank account, managing it effectively is crucial for financial health. Here are some key tips:

Track Your Spending and Income

Regularly review your account statements or use budgeting apps to track your income and expenses. This helps you understand your spending habits, identify areas for saving, and ensure you have enough funds to cover your bills.

Set Up Account Alerts

Most banks offer account alerts via text or email to notify you of important events, such as low balances, deposits, or suspicious activity. These alerts can help you avoid overdraft fees and stay informed about your account status.

Utilize Online and Mobile Banking

Take advantage of online and mobile banking platforms for convenient account management. You can check balances, transfer funds, pay bills, and even deposit checks remotely, saving you time and effort.

Reconcile Your Account Regularly

Compare your bank statements with your own records of transactions to ensure accuracy and identify any discrepancies. This helps detect errors or unauthorized transactions promptly.

Protecting Your Funds

When choosing a bank account, security should be a top priority. Here’s what to consider to ensure your money is protected:

FDIC or NCUA Insurance

In the United States, look for banks that are insured by the Federal Deposit Insurance Corporation (FDIC) or credit unions insured by the National Credit Union Administration (NCUA). These institutions provide deposit insurance, typically up to $250,000 per depositor, per insured bank, in case the bank fails. This insurance gives you peace of mind knowing your funds are protected.

Strong Security Measures

Opt for banks with robust security measures in place. This includes:

- Two-factor authentication: This adds an extra layer of security when accessing your account online or through mobile apps.

- Encryption: Ensure the bank uses encryption technology to protect your information during online transactions.

- Fraud monitoring: Choose a bank that actively monitors accounts for suspicious activity and alerts you promptly.

Fraud Prevention Tips

While banks implement security measures, it’s crucial to take proactive steps to protect yourself:

- Use strong passwords: Create unique, complex passwords for your online banking and avoid using the same password for multiple accounts.

- Be cautious of phishing scams: Beware of suspicious emails or websites that ask for your personal or financial information. Banks typically don’t solicit this information through unsolicited emails.

- Regularly monitor your account: Review your bank statements frequently and report any discrepancies or unauthorized transactions immediately.

Using Mobile Banking

In today’s digital age, mobile banking has become an indispensable part of managing finances. Most banks offer user-friendly mobile apps that allow you to access your accounts and conduct transactions conveniently and securely from your smartphone or tablet.

Here are key features and benefits of mobile banking to consider when choosing a bank account:

- Account Management: Easily check balances, view transaction history, and monitor account activity in real-time.

- Fund Transfers: Quickly transfer funds between your accounts or send money to other individuals domestically.

- Bill Pay: Schedule and pay bills electronically, ensuring timely payments and avoiding late fees.

- Mobile Check Deposit: Deposit checks conveniently by snapping a photo using your smartphone’s camera.

- ATM & Branch Locator: Quickly find nearby ATMs and bank branches when you need cash or in-person assistance.

- Customer Service: Connect with customer support representatives directly through the app for assistance with account-related queries.

- Security Features: Mobile banking apps prioritize security with features such as multi-factor authentication, encryption, and fraud monitoring to protect your financial information.

When evaluating mobile banking options, consider the app’s functionality, ease of use, and the availability of features that align with your banking habits. Reading user reviews and comparing ratings can provide insights into the performance and reliability of different mobile banking apps.

Finding the Best Bank for You

Once you have a clear understanding of your banking needs and the types of accounts available, it’s time to research and compare different financial institutions. Here are key factors to consider when choosing a bank:

1. Fees and Charges

Carefully review the fee schedule for each bank you’re considering. Pay close attention to monthly maintenance fees, ATM fees, overdraft fees, and any other charges associated with the account you’re interested in. Look for banks that offer ways to waive or minimize these fees, such as maintaining a minimum balance or setting up direct deposit.

2. Interest Rates

While interest rates on checking accounts are generally low, it’s still worthwhile to compare rates offered by different banks, especially if you plan to maintain a high balance. For savings accounts and other interest-bearing accounts, prioritize banks with competitive interest rates to maximize your earnings.

3. Account Features and Convenience

Consider the features and conveniences offered by each bank. This may include online and mobile banking capabilities, bill pay services, mobile check deposit, ATM access, and branch availability. Choose a bank that aligns with your lifestyle and preferred banking methods.

4. Customer Service and Reputation

Research each bank’s reputation for customer service. Look for reviews and ratings from other customers to get an idea of their experiences. Consider contacting the bank directly to ask questions and assess their responsiveness and helpfulness.

5. Security and FDIC Insurance

Ensure the bank you choose is FDIC-insured, which protects your deposits up to $250,000 per depositor, per insured bank. Additionally, inquire about their security measures to safeguard your account from fraud and unauthorized access. Look for features like two-factor authentication and fraud monitoring.

Frequently Asked Questions

What are the different types of bank accounts available?

Common types include checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs). Each serves a different purpose and comes with unique features and fees.

How do I know which bank account is right for me?

Consider your financial goals and spending habits. Do you need an account for daily transactions or long-term savings? How important are interest rates and fees to you?

What fees should I be aware of with bank accounts?

Be sure to understand potential charges like monthly maintenance fees, ATM fees, overdraft fees, and minimum balance requirements. These can vary greatly between banks and account types.

How important is it to choose a bank with a strong online and mobile banking platform?

For many, convenient online and mobile access is crucial. Look for features like mobile check deposit, bill pay, and account alerts that fit your lifestyle.

Should I consider a credit union instead of a traditional bank?

Credit unions are member-owned and often offer competitive rates and lower fees. Consider if you qualify for membership based on their criteria.

Can I have multiple bank accounts with different institutions?

Yes, you can open accounts at various banks to take advantage of different products and services that best meet your needs.

Conclusion

Choosing the right bank account is crucial for managing your finances effectively. Consider your needs, compare account options, and look for features that align with your goals to make an informed decision.

{kind=link}