In this article, discover effective strategies on how to create a budget that works for you and practical tips to stay committed and achieve your financial goals. Learn the art of budgeting and take control of your finances today!

Understanding the Importance of Budgeting

Budgeting often gets a bad rap, conjuring up images of restriction and deprivation. However, understanding the true importance of budgeting reveals a far more empowering picture. A budget isn’t about limiting your freedom; it’s about taking control of your finances to achieve your goals.

Here’s why budgeting is crucial:

1. Financial Awareness

Creating a budget forces you to confront your income and expenses head-on. It provides a crystal-clear picture of where your money is going, often revealing spending habits you weren’t even aware of. This awareness is the foundation of making informed financial decisions.

2. Goal Setting and Achievement

Whether it’s buying a house, paying off debt, or investing in your future, a budget helps you allocate funds towards your aspirations. By setting financial goals and tracking your progress through a budget, you turn your dreams into actionable plans.

3. Stress Reduction

Financial instability is a major source of stress. Budgeting provides a sense of control over your money, replacing uncertainty with peace of mind. Knowing where your money is going and that you’re prepared for expenses, both expected and unexpected, can significantly reduce financial anxiety.

4. Debt Management and Prevention

A budget is an essential tool for managing existing debt and, more importantly, preventing future debt. By tracking your spending and living within your means, you can avoid overreliance on credit cards and loans, paving the way for a healthier financial future.

5. Preparedness for the Unexpected

Life is full of surprises, and not all of them are pleasant. A budget ensures you’re financially prepared for emergencies such as job loss, medical bills, or unexpected repairs. Having an emergency fund, a key component of any good budget, can provide a crucial safety net during difficult times.

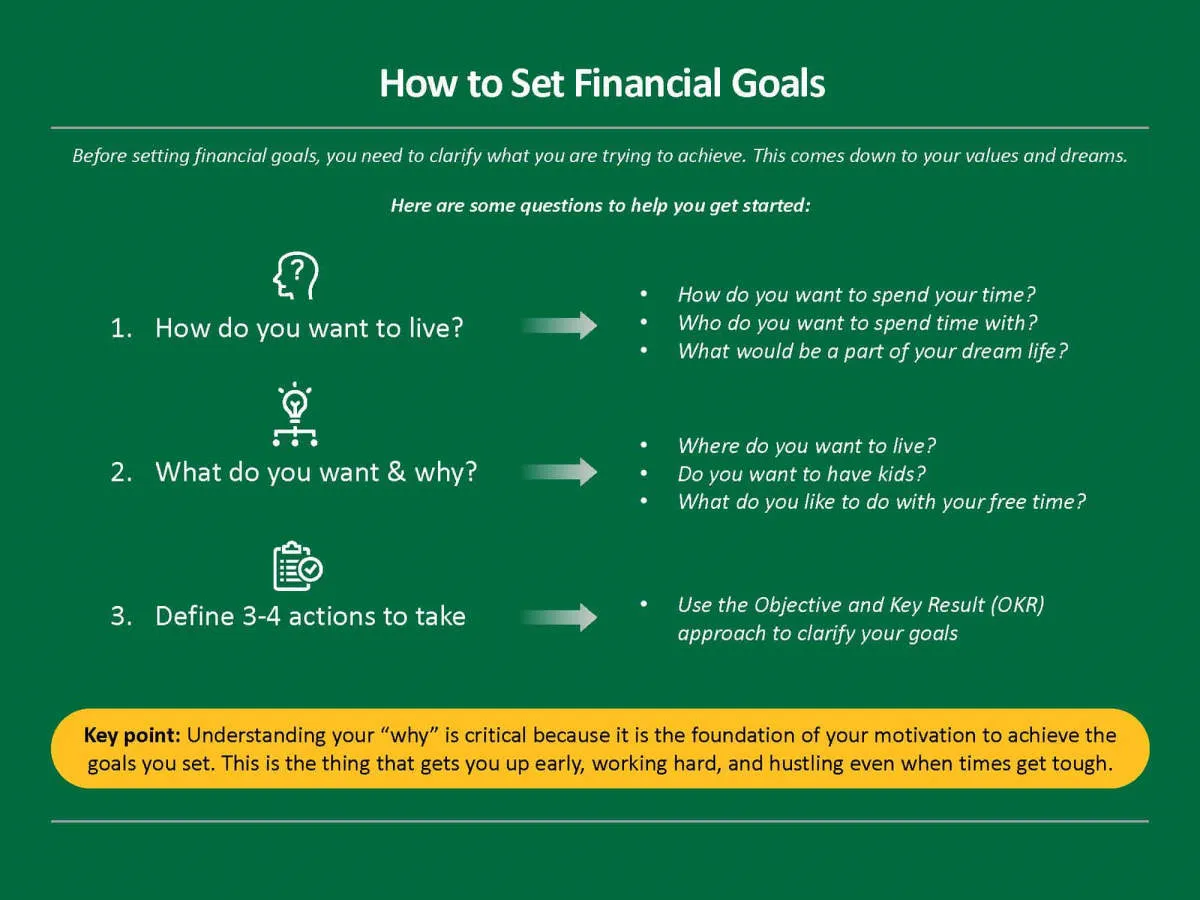

Setting Financial Goals

Before you can create a budget, you need to know what you’re budgeting for. Setting clear financial goals gives you something to work towards and helps you stay motivated. These goals will vary from person to person, but here are some examples:

- Short-Term Goals (within the next year):

- Building an emergency fund

- Paying off credit card debt

- Saving for a down payment on a car

- Mid-Term Goals (1-5 years):

- Saving for a down payment on a house

- Paying off student loans

- Taking a dream vacation

- Long-Term Goals (5+ years):

- Saving for retirement

- Investing in real estate

- Financial independence

When setting your goals, make sure they are:

- Specific: Instead of “save more money,” set a goal like “save $5,000 for a down payment.”

- Measurable: Track your progress and know how much closer you are to your goal.

- Achievable: Set realistic goals that you can actually reach with your current income and expenses.

- Relevant: Choose goals that are important to you and align with your values.

- Time-Bound: Give yourself a deadline to stay motivated and on track.

Tracking Your Income and Expenses

The cornerstone of any successful budget is understanding where your money is coming from and where it’s going. This means diligently tracking both your income and expenses.

Tracking Income

This part is often simpler. List out all your sources of income:

- Salary (after taxes)

- Wages (if paid hourly)

- Side hustle income

- Investments (dividends, interest, etc.)

- Other regular income (government benefits, etc.)

Be realistic about the total amount you bring in each month. If your income fluctuates, use your lowest earning month in recent times as a baseline.

Tracking Expenses

This is where many people struggle. Be as thorough as possible in listing out all your expenses:

- Fixed Expenses: Rent/mortgage, utilities, car payments, insurance, subscriptions

- Variable Expenses: Groceries, gas, dining out, entertainment, clothing

- Periodic Expenses: Car maintenance, medical bills, annual fees

- Debt Payments: Credit cards, student loans, personal loans

Use a budgeting app, spreadsheet, or even a notebook to meticulously record every dollar you spend for at least one full month. Categorize your expenses for a clearer picture.

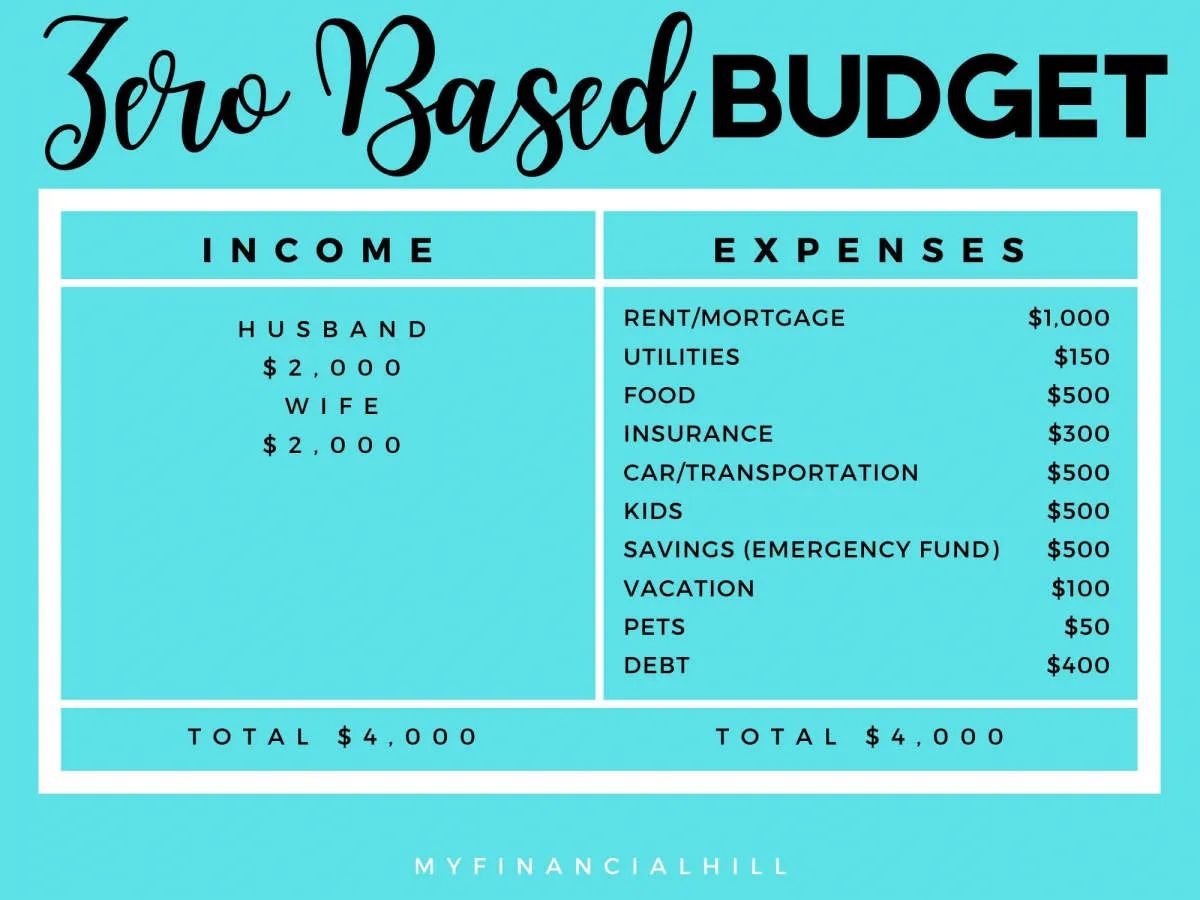

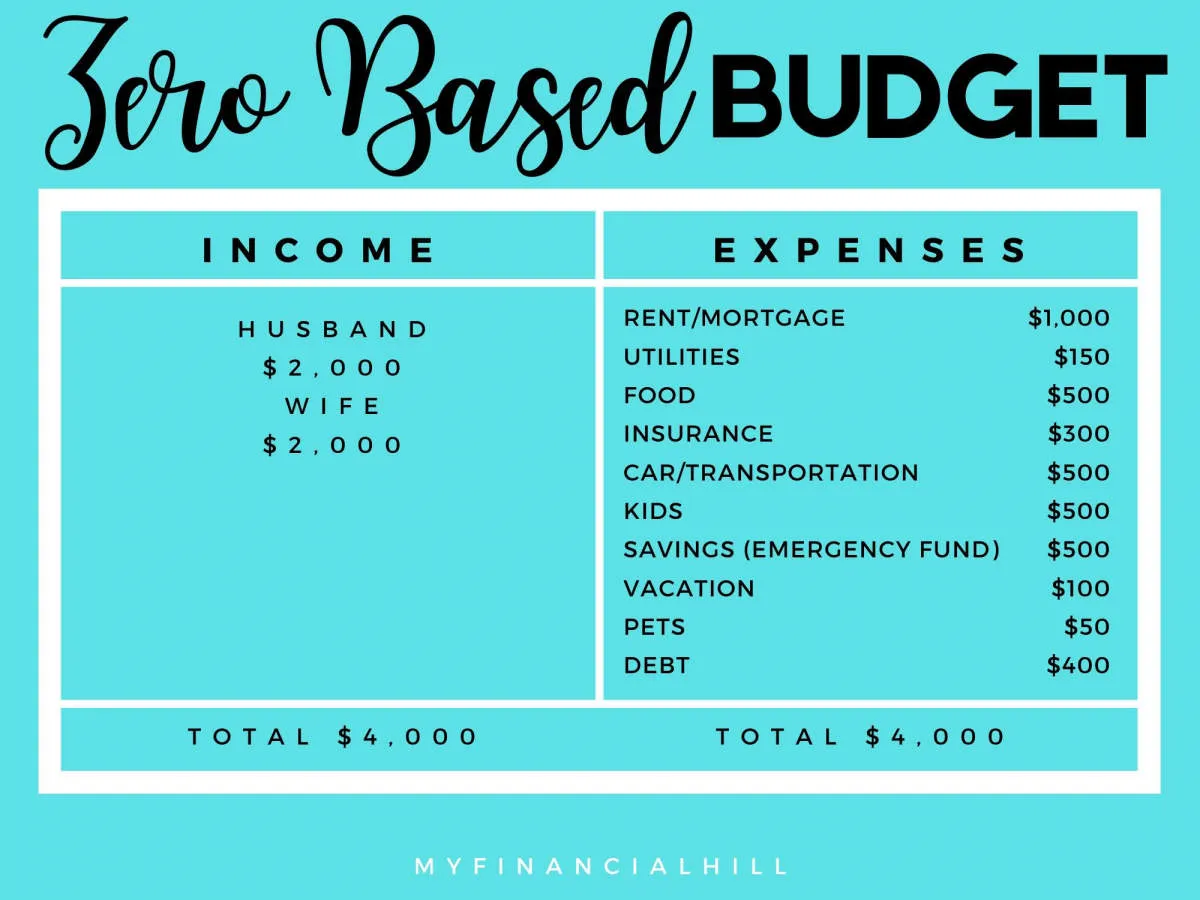

Creating a Monthly Budget

A monthly budget is the cornerstone of healthy financial management. It’s a roadmap that guides your income towards expenses, savings, and financial goals. Here’s a step-by-step process to craft your own:

1. Calculate Your Income

Begin by determining your total monthly income. This includes your salary, wages, bonuses, investment income, and any other sources of regular cash flow.

2. Track Your Expenses

For at least a month, meticulously track every dollar you spend. Categorize your expenses (e.g., housing, transportation, food, entertainment) to gain a clear understanding of where your money goes.

3. Set Realistic Financial Goals

What are your short-term and long-term financial aspirations? Do you want to save for a down payment, pay off debt, or invest? Defining your goals will help you allocate your funds strategically.

4. Differentiate Needs vs. Wants

Carefully analyze your spending habits. Separate your “needs” (essentials like housing and groceries) from your “wants” (discretionary spending like dining out or entertainment). Prioritize your needs while allocating a reasonable amount for your wants.

5. The 50/30/20 Rule (Optional)

Consider using the 50/30/20 budgeting rule as a guideline. This method suggests allocating:

- 50% of your income to needs

- 30% to wants

- 20% to savings and debt repayment

6. Choose a Budgeting Method

Explore various budgeting methods to find one that suits your preferences and lifestyle. Some popular options include:

- The Envelope System: Allocate cash to different spending categories in envelopes.

- Budgeting Apps: Utilize technology to track your income, expenses, and progress.

- Spreadsheets: Create a personalized budget using spreadsheet software.

7. Monitor and Adjust Regularly

Your budget isn’t set in stone. Review it regularly (monthly or bi-weekly) and make adjustments as needed. Life changes, income fluctuates, and goals evolve, requiring flexibility in your budget.

Finding Ways to Save Money

Once you have a clear picture of your income and expenses, it’s time to identify areas where you can save. This is where the rubber meets the road in budgeting, and it requires a shift in mindset from simply tracking money to actively finding ways to reduce spending.

Start by looking at your discretionary spending. These are the non-essential items that you have some control over, such as:

- Dining out

- Entertainment

- Subscriptions

- Clothing

- Personal care

See if you can identify areas where you can cut back without drastically altering your lifestyle. Could you commit to eating out one less time per week? Can you find more affordable entertainment options? Are there subscriptions you can cancel?

Negotiate Better Rates

Don’t be afraid to negotiate with service providers for better rates. Call your internet, phone, and insurance companies to see if you can lower your monthly bills. You might be surprised at how much you can save by simply asking.

Explore Cost-Effective Alternatives

Look for ways to replace expensive habits with more affordable alternatives. For example:

- Brew coffee at home instead of buying it daily.

- Pack your lunch a few times a week.

- Take advantage of free or low-cost entertainment options in your community.

- Utilize library resources instead of buying books and movies.

Automate Your Savings

One of the most effective ways to save is to make it automatic. Set up a system where a portion of each paycheck is automatically transferred to a savings account. You’ll be less likely to spend money that you don’t see in your checking account.

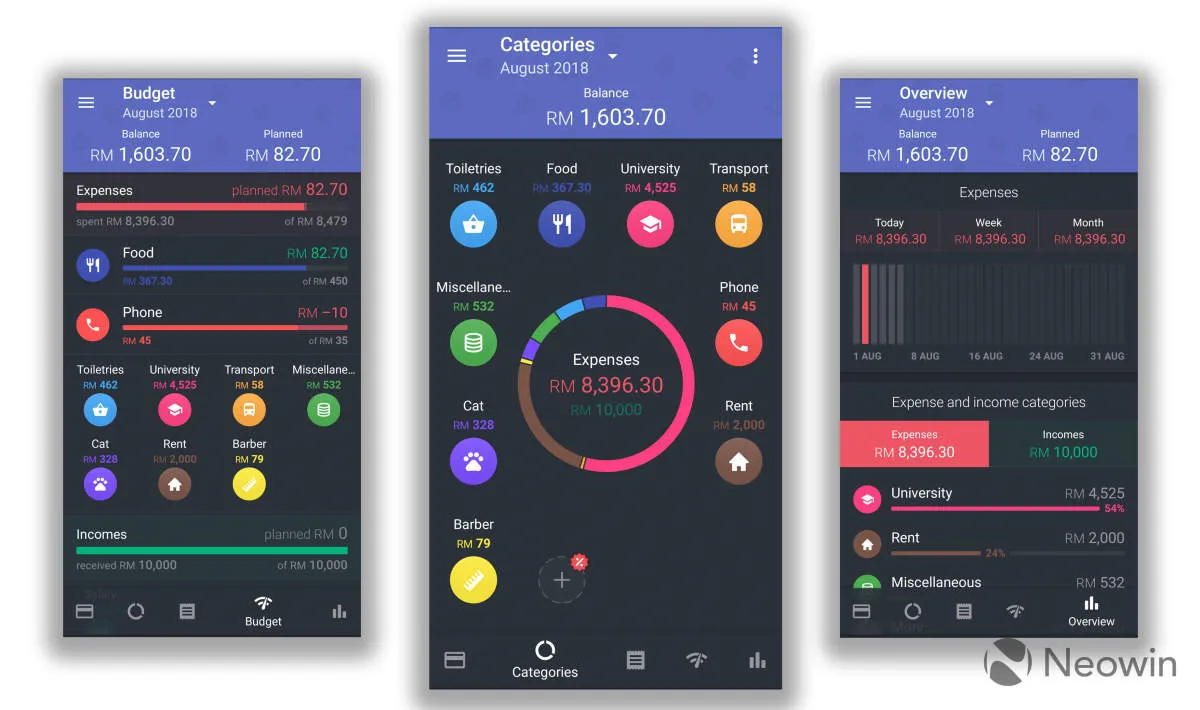

Using Budgeting Apps

Budgeting apps have exploded in popularity in recent years, and for good reason. They offer a convenient and often automated way to track your income and expenses, helping you gain a clearer picture of your financial habits.

Here are some key benefits of using budgeting apps:

- Automatic Tracking: Many apps can connect directly to your bank accounts and credit cards, automatically categorizing transactions to simplify tracking.

- Real-Time Updates: Stay informed about your financial standing at any time. Apps update your budget as you make transactions, so you’re always aware of how much you have left to spend.

- Customizable Budgets: Tailor your budget to your specific needs. Set spending limits for different categories and receive alerts if you’re approaching your limit.

- Goal Setting: Most apps allow you to set financial goals, like saving for a down payment or paying off debt, and track your progress towards them.

- Reporting and Insights: Gain valuable insights into your spending patterns. Apps often provide visual representations of your income, expenses, and progress towards your goals.

There are numerous budgeting apps available, each with its own features and pricing. Some popular options include Mint, YNAB (You Need A Budget), EveryDollar, Personal Capital, and PocketGuard. It’s important to research and compare different apps to find one that best suits your needs and preferences.

Reviewing and Adjusting Your Budget

Creating a budget is not a “set it and forget it” kind of task. Life is constantly changing, and your budget needs to be flexible enough to change with it. Regularly reviewing and adjusting your budget is essential for its success and for reaching your financial goals.

When and How Often to Review

Aim to review your budget at least monthly. This allows you to track your spending habits, identify any areas where you’ve overspent or underspent, and make necessary adjustments for the following month.

Analyzing Your Spending

During your budget review, carefully analyze your spending habits. Compare your actual expenses to your budgeted amounts. Look for patterns and areas where you can potentially cut back or need to allocate more funds.

Adjusting Your Budget

Based on your spending analysis, don’t be afraid to adjust your budget. Life throws curveballs – unexpected expenses, job changes, or shifts in priorities can all impact your finances.

- Increase or Decrease Budget Categories: If you consistently overspend in a specific category, consider increasing its allocated amount. Conversely, if you consistently underspend in another category, you might be able to reduce its allocation and allocate those funds elsewhere.

- Add or Remove Categories: As your life changes, you may need to add or remove budget categories entirely.

- Re-evaluate Your Goals: Your financial goals might change over time. Make sure your budget aligns with your current priorities, whether it’s saving for a down payment on a house, paying off debt, or investing for retirement.

Tips for Effective Budget Adjustments

- Be Realistic: When making adjustments, be realistic about what you can afford and what changes you’re willing to make to your spending habits.

- Start Small: If you need to make significant cuts, start with small, manageable changes rather than trying to overhaul your entire lifestyle overnight.

- Track Your Progress: Continue tracking your spending after making adjustments to ensure they’re effective and you’re staying on track with your financial goals.

Building an Emergency Fund

An emergency fund is a crucial part of responsible financial management. It acts as a safety net, providing financial security in unexpected situations. Without an emergency fund, you might find yourself relying on credit cards or loans, potentially leading to a cycle of debt.

Why is an Emergency Fund Important?

Life is full of surprises, and not all of them are pleasant. An emergency fund can help you navigate:

- Job loss

- Medical emergencies

- Car repairs

- Home repairs

- Unexpected travel expenses

How Much Should You Save?

A good rule of thumb is to have three to six months’ worth of living expenses saved in your emergency fund. This amount should be sufficient to cover your essential expenses for a period if your income is interrupted.

Where to Keep Your Emergency Fund

Your emergency fund should be easily accessible when you need it. A high-yield savings account is generally a good option, as it offers easy access to your funds while earning a bit of interest.

How to Build Your Emergency Fund

Building an emergency fund takes time and dedication. Here are a few tips:

- Start Small: Even setting aside a small amount each month can add up over time.

- Automate Your Savings: Set up automatic transfers from your checking account to your savings account each month.

- Cut Expenses: Look for areas where you can cut back on spending and redirect that money towards your savings goal.

- Windfalls: Deposit any unexpected income, such as tax refunds or work bonuses, into your emergency fund.

Managing Debt

Debt is a common financial burden that can make it difficult to stick to a budget. However, by taking steps to manage your debt, you can free up more money each month and reach your financial goals faster. Here’s how:

1. Create a List of All Your Debts

Start by making a list of all your debts, including the lender, outstanding balance, interest rate, and minimum payment. This will give you a clear picture of your overall debt load and help you prioritize which debts to tackle first.

2. Explore Debt Consolidation Options

If you have multiple debts with high interest rates, consider consolidating them into a single loan with a lower rate. This can simplify your finances and potentially save you money on interest payments.

3. Negotiate with Creditors

Don’t be afraid to contact your creditors and try to negotiate lower interest rates or monthly payments. They may be willing to work with you, especially if you’re experiencing financial difficulties.

4. Prioritize High-Interest Debts

Focus on paying down high-interest debts first, such as credit cards, as they can quickly accumulate and make it harder to get ahead. Consider using the debt snowball or debt avalanche method to accelerate your progress.

5. Consider a Debt Management Plan

If you’re struggling to manage your debt on your own, a debt management plan (DMP) through a reputable credit counseling agency may be a good option. A DMP can help you negotiate lower interest rates and consolidate your payments into a single, manageable amount.

Seeking Professional Advice

Sometimes, managing your finances and creating a budget can feel overwhelming. You might have complex financial situations, or maybe you’re just not sure where to start. In these cases, seeking advice from a financial advisor can be immensely beneficial.

Financial advisors can provide personalized guidance tailored to your specific financial goals and situation. They can help you with:

- Assessing your current financial health

- Developing a realistic budget and savings plan

- Managing debt effectively

- Planning for retirement

- Making informed investment decisions

Remember, financial advisors are professionals with the knowledge and experience to guide you towards financial well-being. Don’t hesitate to reach out if you need assistance.

Conclusion

In conclusion, creating a budget and sticking to it is essential for financial success. By tracking expenses, setting goals, and making adjustments when necessary, individuals can achieve their financial objectives.

{kind=link}