Learn how to leverage credit cards to maximize rewards and benefits in our guide on using credit cards strategically.

Understanding Credit Card Terms

Before you can maximize the benefits of credit cards, it’s crucial to understand the key terms and conditions that come with them. This knowledge will empower you to use your cards responsibly and avoid common pitfalls.

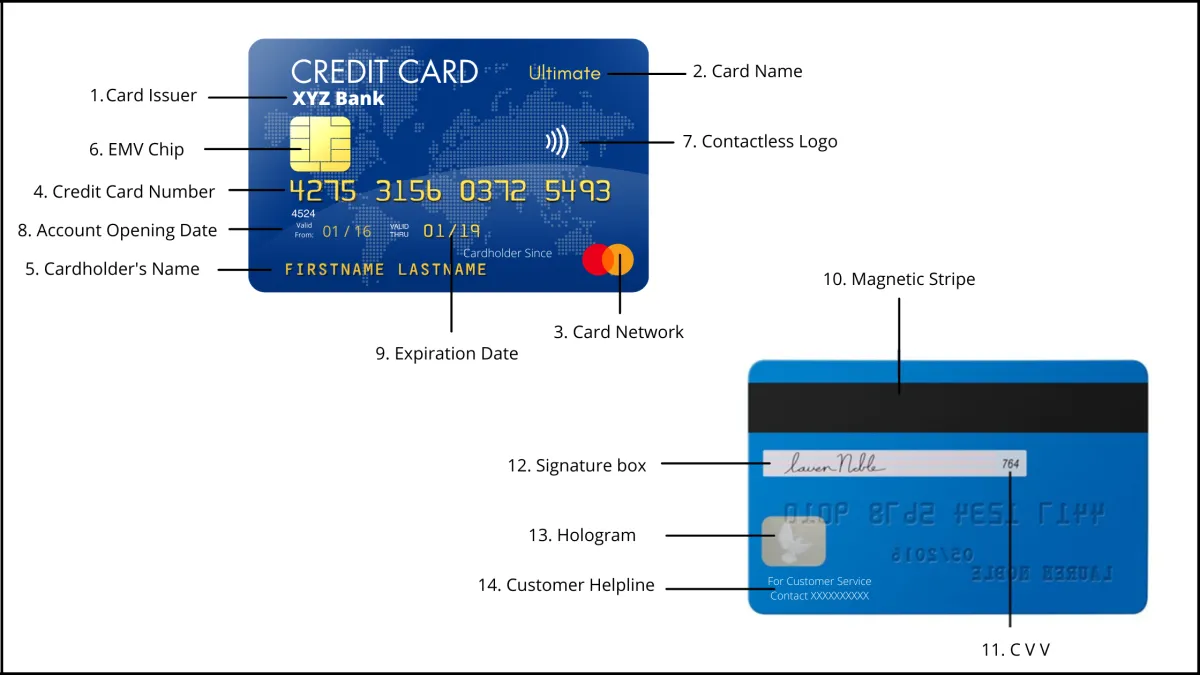

Important Credit Card Terms:

- APR (Annual Percentage Rate): This is the yearly interest rate charged on your outstanding balance. A lower APR means you’ll pay less in interest charges.

- Credit Limit: The maximum amount of money you can spend on your credit card. It’s important to keep your balance well below this limit to maintain a healthy credit utilization ratio.

- Minimum Payment: The minimum amount you need to pay each month to avoid late fees. However, paying only the minimum can keep you in debt for a long time due to accumulating interest.

- Grace Period: The interest-free period you have to pay your balance in full before interest starts accruing. Typically, this period is around 21 days from the statement closing date.

- Balance Transfer: Transferring your balance from one credit card to another, often to take advantage of a lower introductory APR.

- Cash Advance: Withdrawing cash from an ATM using your credit card. Be cautious, as these usually come with high fees and interest rates.

- Foreign Transaction Fees: Fees charged for using your credit card in a foreign country. These can vary, so check your card’s terms before traveling.

- Rewards Programs: Many credit cards offer rewards like cashback, travel points, or miles for your spending. Make sure the rewards program aligns with your spending habits.

- Credit Score: A numerical representation of your creditworthiness, influenced by factors like your payment history and credit utilization. A good credit score can help you qualify for lower interest rates and better terms.

Choosing the Right Credit Card

With a dizzying array of credit cards available, each touting attractive perks and rewards, finding the perfect one for your spending habits can seem overwhelming. But don’t fret! Selecting the right credit card can actually be quite straightforward when you know what to look for.

1. Identify Your Spending Habits

Before diving into the world of credit cards, take a hard look at your spending. Are you a frequent flyer who prioritizes travel rewards? A foodie who loves dining out? Or perhaps a homebody who values cashback on everyday purchases? Understanding where your money goes is crucial in identifying a card that aligns with your lifestyle.

2. Consider Your Credit Score

Your credit score plays a significant role in the types of cards you qualify for. Generally, individuals with excellent credit have access to cards with the best rewards and lowest interest rates. If you’re building your credit, secured or student cards offer a great starting point.

3. Compare Rewards Programs

Rewards are the name of the game! Whether it’s cashback, travel miles, or points redeemable for merchandise, there’s a reward program out there to suit you. Carefully compare the earning rates and redemption options across different cards to ensure you’re getting the most bang for your buck (or swipe!).

4. Factor in Fees and Interest Rates

Don’t let flashy rewards blind you to the fine print. Pay close attention to annual fees, balance transfer fees, and foreign transaction fees, especially if you travel frequently. Equally important is the APR (Annual Percentage Rate), which determines the interest you’ll accrue on unpaid balances. Aim for a card with a low APR to minimize interest charges.

5. Read the Fine Print

We know, reading the fine print isn’t the most thrilling activity, but it’s essential! Familiarize yourself with the card’s terms and conditions, including grace periods, late payment fees, and any restrictions on rewards earning or redemption.

Using Credit Cards for Necessities

While credit cards can be valuable tools for building credit and earning rewards, it’s important to use them responsibly. One strategy is to leverage them for essential expenses you’d typically pay for anyway. This approach can help you earn cash back, points, or miles on everyday purchases.

Identify your necessary expenses: These could include:

- Groceries

- Gas

- Utilities (electricity, water, internet)

- Monthly subscriptions (streaming services, gym memberships)

- Public transportation

Select the right credit card: Look for a card that offers the best rewards for your spending habits. Some cards provide higher cashback rates on specific categories like groceries or gas, while others offer bonus points for general spending. Compare options and choose the one that aligns with your necessities.

Set a budget and track your spending: Using credit cards for necessities only works if you maintain control over your spending. Create a budget to track your expenses and ensure you’re not overspending just to earn rewards. Remember, the goal is to maximize benefits without falling into debt.

Pay your balance in full and on time: The key to avoiding interest charges and maximizing the benefits of using credit cards for necessities is to pay your balance in full every month. Set up reminders or automatic payments to avoid late fees and maintain a positive credit history.

Paying Your Balance in Full

One of the most crucial aspects of utilizing credit cards effectively is paying your balance in full by the due date each month. This practice offers several significant advantages:

- Avoid Interest Charges: Credit card interest rates can be quite high. By paying your balance in full, you effectively avoid paying any interest, saving you money in the long run.

- Maintain a Good Credit Score: Payment history is a major factor in determining your credit score. Consistently paying on time demonstrates responsible credit management to lenders.

- Maximize Rewards: Many credit cards offer rewards such as cashback, points, or miles. Paying your balance in full ensures you reap the full benefits of these rewards without losing them to interest payments.

Failing to pay your balance in full can lead to a downward spiral of debt and damage your credit score. Make it a habit to track your spending, budget effectively, and prioritize paying your credit card balance in full each month to maximize the benefits of using credit cards responsibly.

Avoiding Cash Advances

While credit cards offer a convenient way to access credit, it’s crucial to understand the different features and use them wisely. One such feature that often comes with hefty costs is the cash advance option. Let’s delve into why avoiding cash advances is generally a good practice:

High Fees:

Cash advances typically come with high fees, often a percentage of the amount withdrawn or a minimum flat fee, whichever is greater. These fees can quickly add up, making your cash advance significantly more expensive than the amount you actually withdraw.

High APR:

Unlike regular purchases, cash advances often have a higher Annual Percentage Rate (APR). This means you’ll accrue interest at a faster rate, leading to a larger debt burden over time.

No Grace Period:

Unlike regular credit card purchases, which usually come with a grace period for interest charges, cash advances generally start accruing interest from the day you withdraw the cash. This lack of a grace period can further increase the overall cost of the advance.

Potential Impact on Credit Score:

Frequent cash advances can potentially negatively impact your credit score. They can signal to lenders a higher risk of default, potentially affecting future loan approvals and interest rates.

Monitoring Your Spending

One of the most crucial aspects of using credit cards effectively is diligent spending monitoring. It’s easy to overspend when you’re not closely tracking where your money is going. Here’s how to stay on top of your credit card spending:

1. Utilize Budgeting Apps or Spreadsheets

Numerous budgeting apps and online tools can seamlessly sync with your credit card accounts, providing a real-time view of your spending habits. Alternatively, a simple spreadsheet can be just as effective for tracking your purchases and categorizing them.

2. Review Your Statements Regularly

Don’t wait for your monthly statement to arrive in the mail. Most credit card issuers offer online account access, allowing you to review your transactions daily or weekly. This frequent check-in helps identify any discrepancies or potentially fraudulent activity early on.

3. Set Spending Alerts

Take advantage of the alert features offered by your credit card provider. You can typically set up alerts for different scenarios, such as when your balance reaches a certain limit, a transaction exceeds a specific amount, or your due date is approaching. These timely reminders can help prevent overspending and late payments.

4. Categorize Your Spending

By categorizing your credit card expenses (e.g., groceries, dining out, entertainment, travel), you gain valuable insights into your spending patterns. This allows you to identify areas where you might be overspending and make necessary adjustments to your budget.

5. Reconcile Your Transactions

Regularly cross-check your credit card transactions against your budget and bank statements. This process helps ensure accuracy and allows you to quickly spot any errors or unauthorized charges.

Setting a Credit Limit

A credit limit is the maximum amount of money a lender will allow you to borrow on your credit card. It’s a crucial factor that influences your credit utilization rate and overall financial well-being. When used responsibly, credit cards can provide numerous benefits, and setting the right credit limit is fundamental to maximizing those advantages.

Consider these factors when determining your ideal credit limit:

- Spending Habits: Analyze your monthly expenses and spending patterns. Choose a credit limit that aligns with your typical spending, avoiding unnecessary temptation to overspend.

- Financial Goals: A lower credit limit can be beneficial if you aim to manage debt or save money. Conversely, a higher limit might be suitable for building credit or making significant purchases, provided you maintain responsible usage.

- Credit Utilization Rate: Your credit utilization rate, the percentage of available credit you’re using, significantly impacts your credit score. A lower credit utilization ratio is generally better. A lower credit limit can make it easier to keep your credit utilization low, assuming you maintain control of your spending.

- Temptation and Control: Be honest with yourself about your spending habits. If you tend to overspend, a lower credit limit can act as a safeguard, preventing you from accumulating excessive debt.

Requesting a Credit Limit Increase or Decrease:

You can request a credit limit increase or decrease from your credit card issuer. When making your decision, carefully weigh the potential benefits and drawbacks and how they align with your overall financial strategy.

Building an Emergency Fund

While credit cards can be incredibly useful tools for managing your finances and even earning rewards, they should never be your first line of defense in a financial emergency. That’s where a robust emergency fund comes in.

An emergency fund is a stash of cash specifically set aside to cover unexpected expenses, such as:

- Job loss

- Medical bills

- Car repairs

- Home repairs

Having this fund acts as a buffer, preventing you from relying on high-interest credit card debt when unforeseen events arise. Aim to have 3-6 months’ worth of living expenses saved in a liquid, easily accessible account.

Here’s how you can start building your emergency fund:

- Assess your monthly expenses: Determine how much you need each month to cover essential costs.

- Set a savings goal: Aim for 3-6 months’ worth of living expenses, but start with a smaller, achievable target.

- Automate your savings: Schedule regular transfers from your checking account to your emergency fund.

- Cut back on unnecessary spending: Identify areas where you can reduce spending and redirect funds to your savings.

- Find extra income opportunities: Explore side hustles or freelance work to boost your savings rate.

By diligently building your emergency fund, you’ll be better prepared to navigate financial challenges without relying heavily on credit. This will ultimately lead to a healthier financial future and allow you to use your credit cards strategically for rewards and benefits rather than out of necessity.

Using Credit Card Rewards Responsibly

Earning credit card rewards can feel like getting free money, but it’s important to approach them with a responsible mindset. Here’s how to make the most of your rewards without falling into debt traps:

1. Don’t Spend More to Earn Rewards:

The golden rule of credit card rewards is to only spend what you can afford to pay back in full each month. Chasing rewards by overspending will negate any benefits and lead to unnecessary debt.

2. Understand Your Redemption Options:

Credit card rewards come in various forms like cashback, travel points, and merchandise. Familiarize yourself with your card’s redemption options and their associated values. Sometimes, a seemingly higher rewards rate might not translate to the best value for your spending habits.

3. Track Your Points and Expiration Dates:

Keep an eye on your rewards balance and expiration dates. Some programs have inactivity clauses that could forfeit your hard-earned points. Set reminders or utilize reward tracking apps to stay organized.

4. Prioritize Needs Over Wants:

While it’s tempting to splurge your rewards on luxury items, consider prioritizing your needs first. Using your rewards to offset essential expenses like groceries or utility bills can provide significant financial relief.

5. Avoid Fees That Outweigh Rewards:

Be mindful of annual fees, foreign transaction fees, or interest charges. Calculate if these fees outweigh the potential rewards you’d earn. Sometimes, a no-fee card with a lower rewards rate might be more beneficial in the long run.

Seeking Professional Advice

While this article provides general advice on maximizing credit card benefits, remember that individual financial situations vary. Consulting a qualified financial advisor can provide personalized guidance tailored to your circumstances.

A financial advisor can help you:

- Assess your credit card needs and goals.

- Identify the best cards and rewards programs for you.

- Develop a credit card strategy to maximize benefits while avoiding debt.

- Create a budget that incorporates credit card usage and repayment.

- Improve your credit score for better card offers.

Seeking professional advice ensures you’re making informed decisions to leverage credit cards effectively and reach your financial goals.

Conclusion

In conclusion, utilizing credit cards wisely by maximizing rewards, monitoring spending, and paying balances in full each month can lead to significant benefits and financial gains.

{kind=link}