In the world of personal finance, knowledge is key. This article will break down the basics of managing your money, covering topics like budgeting, saving, investing, and more to help you make informed financial decisions.

Creating a Budget

A budget is a financial plan that outlines your expected income and expenses over a specific period, typically a month. It acts as a roadmap, guiding your spending and saving habits to help you achieve your financial goals. Creating a budget may seem daunting, but it’s a crucial step towards financial well-being. Here’s a step-by-step guide to get you started:

1. Track Your Income and Expenses

The first step is understanding where your money comes from and where it goes. Begin by listing all sources of income, such as your salary, wages, or any other regular payments. Next, track your expenses diligently. Utilize banking apps, spreadsheets, or budgeting tools to record every expense, categorizing them for better analysis.

2. Differentiate Between Needs and Wants

Once you have a clear picture of your cash flow, differentiate between your needs and wants. Needs are essential expenses like housing, groceries, utilities, and transportation. Wants, on the other hand, are non-essential expenses like entertainment, dining out, or luxury items. Prioritize your spending by allocating funds for needs before considering wants.

3. Set Realistic Financial Goals

Define your short-term and long-term financial goals. Whether it’s saving for a down payment, paying off debt, or investing, having clear goals provides direction for your budget. Determine how much you need to save or allocate each month to reach these goals within your desired timeframe.

4. Choose a Budgeting Method

Various budgeting methods cater to different preferences and lifestyles. Some popular methods include the 50/30/20 budget, where 50% of your income goes towards needs, 30% towards wants, and 20% towards savings and debt repayment. Others prefer the envelope system, where cash is allocated to specific spending categories in envelopes. Explore different methods and choose one that aligns with your style.

5. Monitor and Adjust Regularly

Creating a budget is not a one-time task. Life is dynamic, and your financial situation may fluctuate. Regularly review your budget, preferably monthly, to track your progress, identify areas for improvement, and make necessary adjustments. Celebrate small victories and stay committed to your financial plan.

Managing Debt

Debt is a fact of life for many people, but it’s important to manage it responsibly. High levels of debt can lead to stress, financial instability, and difficulty achieving your financial goals. Here are some key strategies for managing debt effectively:

1. Create a Budget and Track Your Spending:

Start by understanding where your money is going. Create a detailed budget that tracks your income and expenses. This will help you identify areas where you can cut back on spending and free up more cash flow to put towards debt repayment.

2. Prioritize Debt Repayment:

Not all debt is created equal. Prioritize high-interest debt, such as credit card debt, as it accrues interest quickly and can trap you in a cycle of debt. Consider using strategies like the debt snowball or debt avalanche method to accelerate your repayment.

3. Explore Debt Consolidation or Refinancing:

If you have multiple debts with varying interest rates, explore options for debt consolidation or refinancing. Consolidating your debts into a single loan with a lower interest rate can simplify your repayment and potentially save you money on interest charges.

4. Negotiate with Creditors:

Don’t be afraid to contact your creditors and try to negotiate lower interest rates, waived fees, or modified payment plans. They may be willing to work with you, especially if you’re experiencing financial hardship.

5. Seek Professional Advice:

If you’re struggling to manage your debt or feel overwhelmed, don’t hesitate to seek professional financial advice. A financial advisor can provide personalized guidance, help you create a debt management plan, and explore potential solutions tailored to your situation.

Building an Emergency Fund

An emergency fund is a crucial component of healthy personal finances. It acts as a safety net, providing a financial cushion to cover unexpected expenses or financial disruptions without derailing your overall financial stability.

Why is an Emergency Fund Important?

Life is full of surprises, and not all of them are pleasant. Unexpected events such as job loss, medical emergencies, car repairs, or home repairs can put a significant strain on your finances. Without an emergency fund, you might be forced to rely on credit cards, take out high-interest loans, or dip into long-term savings to cover these costs. This can lead to a cycle of debt and financial stress.

How Much Should You Save?

A common rule of thumb is to save three to six months’ worth of living expenses in your emergency fund. This means having enough money saved to cover essential expenses like rent/mortgage payments, utilities, groceries, transportation, and debt payments for that period. The exact amount you need will depend on your individual circumstances, such as your job security, dependents, and living costs.

Where to Keep Your Emergency Fund

Your emergency fund should be easily accessible when you need it. The best place to keep it is in a separate, high-yield savings account. This allows you to earn interest on your savings while still being able to access your funds quickly when an emergency arises.

Tips for Building Your Emergency Fund

- Start small: Even if you can only save a small amount each month, it’s better than nothing. Gradually increase your savings rate over time.

- Make it automatic: Set up automatic transfers from your checking account to your emergency fund each month. This makes saving easier and ensures consistency.

- Cut expenses and find extra income: Look for ways to reduce your spending or find additional sources of income to boost your savings rate.

- Replenish your fund after use: If you need to use your emergency fund, make it a priority to replenish it as soon as possible.

Investing for the Future

Investing is a crucial aspect of personal finance that focuses on growing your wealth over time. It involves putting your money to work in assets that have the potential to increase in value, generating returns and helping you achieve your long-term financial goals, such as retirement or buying a home.

Why is Investing Important?

Investing is essential for several reasons:

- Outpacing Inflation: Investments help your money grow at a rate that outpaces inflation, ensuring that your purchasing power is maintained over time.

- Building Wealth: By investing wisely, you can accumulate wealth steadily, even with modest contributions.

- Reaching Financial Goals: Investing allows you to work towards significant financial milestones, such as retirement planning, purchasing a home, or funding your children’s education.

Types of Investments:

There are numerous investment options available, each with its own risk and return characteristics. Some common investment types include:

- Stocks: Represent ownership in publicly traded companies. Stocks offer the potential for high returns but also come with higher volatility.

- Bonds: Debt securities issued by governments or corporations. Bonds typically offer lower returns than stocks but are generally less risky.

- Mutual Funds and ETFs: Investment vehicles that pool money from multiple investors to invest in a diversified portfolio of assets.

- Real Estate: Investing in physical property, such as residential or commercial real estate.

Understanding Credit Scores

A credit score is a three-digit number that represents your creditworthiness, or how likely you are to repay borrowed money. Lenders, such as banks and credit card companies, use credit scores to assess the risk of lending you money. A higher credit score indicates lower risk to the lender, often resulting in better interest rates and loan terms.

Factors Influencing Credit Scores:

Several factors contribute to your credit score calculation. The most significant ones include:

- Payment History (35%): Your track record of paying bills on time, including credit card payments, loans, and utilities.

- Amounts Owed (30%): The amount of debt you have relative to your available credit (credit utilization ratio). Lower utilization generally indicates better credit health.

- Length of Credit History (15%): A longer credit history demonstrates stability and reliability to lenders.

- Credit Mix (10%): Having a mix of different credit types, such as credit cards and installment loans, can positively impact your score.

- New Credit (10%): Opening several new credit accounts in a short period can lower your score as it may indicate increased risk.

Importance of a Good Credit Score

A good credit score unlocks numerous financial benefits:

- Lower interest rates on loans, saving you money over the life of the loan.

- Higher credit card limits and better rewards programs.

- Easier approval for rental applications and utilities.

- Potential discounts on insurance premiums.

Using Financial Tools

Managing your personal finances effectively often requires utilizing various financial tools available to you. These tools can range from simple budgeting apps to more sophisticated investment platforms, each serving a specific purpose in helping you achieve your financial goals.

Budgeting and Expense Tracking:

Keeping track of your income and expenses is the foundation of personal finance. Several tools can assist you in this crucial task:

- Budgeting Apps: Mint, YNAB (You Need a Budget), and Personal Capital are popular choices that allow you to connect your bank accounts, categorize transactions, and set spending limits.

- Spreadsheets: You can create a simple yet effective budgeting spreadsheet using programs like Microsoft Excel or Google Sheets. This method offers greater customization but requires manual input.

- Envelope System: This traditional approach involves allocating cash to different spending categories in envelopes. While effective for some, it may not be practical for all expenses in today’s digital world.

Saving and Investing:

Once you have a clear picture of your cash flow, you can explore tools to help you save and invest your money:

- High-Yield Savings Accounts: These accounts offer better interest rates than traditional savings accounts, helping your money grow faster.

- Investment Apps: Platforms like Robinhood, Acorns, and Stash make investing accessible to beginners, offering fractional shares and automated investing options.

- Retirement Accounts: Employer-sponsored plans like 401(k)s and individual retirement accounts (IRAs) provide tax advantages for retirement savings. Consult with a financial advisor to determine the best option for your situation.

Credit Monitoring and Debt Management:

Maintaining a healthy credit score is essential for obtaining loans and favorable interest rates. These tools can help you monitor and manage your credit:

- Credit Monitoring Services: Experian, Equifax, and TransUnion offer credit monitoring services that alert you to changes in your credit report, potentially protecting you from fraud.

- Debt Consolidation Loans: If you have multiple debts with high interest rates, consolidating them into a single loan with a lower rate can simplify payments and save money.

- Debt Snowball or Avalanche Method: These debt repayment strategies offer structured approaches to paying off debt, empowering you to take control of your finances.

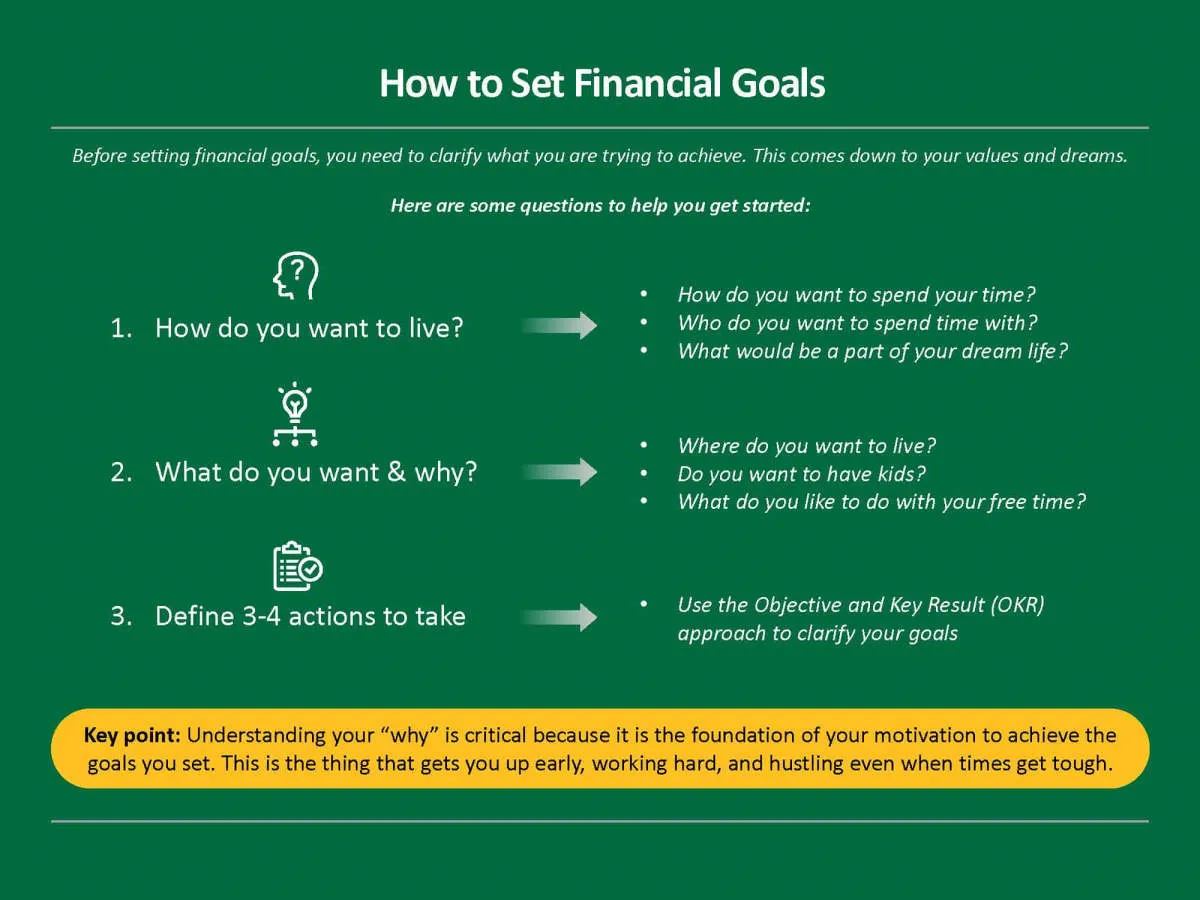

Setting Financial Goals

Setting financial goals is the cornerstone of effective personal finance management. It provides a roadmap for your financial journey, helping you prioritize spending, save effectively, and work towards achieving your aspirations. Whether it’s buying a home, retiring comfortably, or simply gaining control of your finances, well-defined goals are essential.

Types of Financial Goals:

Financial goals can be categorized based on their time horizon:

- Short-Term Goals: Achievable within a year, such as building an emergency fund or paying off a credit card.

- Mid-Term Goals: Typically achieved within 1-5 years, such as saving for a down payment or a major vacation.

- Long-Term Goals: Require 5+ years, such as retirement planning or saving for a child’s college education.

SMART Goals:

The SMART goal-setting framework is highly effective for financial planning:

- Specific: Clearly define your goal, including the amount and purpose (e.g., save $10,000 for a down payment).

- Measurable: Track your progress with concrete numbers (e.g., save $500 per month).

- Achievable: Set realistic goals within your financial means.

- Relevant: Align your goals with your values and priorities.

- Time-Bound: Establish a clear deadline to create urgency (e.g., save the down payment within 2 years).

Prioritizing Your Goals:

It’s important to prioritize your financial goals. Consider which goals are most important to you and focus on those first. You can then allocate your resources accordingly.

Reviewing and Adjusting Your Plan

Creating a personal finance plan is a crucial first step, but it’s not a “set it and forget it” kind of deal. Life is dynamic, and your financial plan needs to be flexible enough to adapt to these changes. This is where regular review and adjustment come in.

Why Review?

Life throws curveballs. You might encounter:

- Income changes: A raise, a job loss, or starting a side hustle all impact your financial situation.

- Unexpected expenses: Medical bills, car repairs, or a leaking roof can pop up unexpectedly.

- Shifts in goals: Maybe you’re getting married, buying a house, or planning for early retirement – all requiring adjustments to your financial strategy.

- Market fluctuations: Investments don’t always go up. Market downturns can impact your savings and investments, necessitating a reevaluation.

When and How Often to Review

A good rule of thumb is to review your plan at least annually. However, more frequent check-ins, such as quarterly, are recommended, especially during times of significant change or economic uncertainty.

What to Look For During Review

- Progress on Goals: Are you on track to meet your savings goals, debt reduction targets, or investment milestones?

- Budget vs. Actual Spending: How closely are you sticking to your budget? Are there areas of overspending or opportunities to cut back?

- Debt Management: Is your debt level manageable? Are you paying off high-interest debts efficiently?

- Emergency Fund: Do you have enough saved to cover 3-6 months of living expenses in case of emergencies?

- Investment Performance: How are your investments performing? Do you need to rebalance your portfolio based on your risk tolerance and goals?

Making Adjustments

Based on your review, don’t hesitate to make necessary adjustments. This might involve:

- Tweaking your budget: Reduce unnecessary spending in certain areas or allocate more funds to essential categories.

- Renegotiating debt: Explore options like balance transfers or debt consolidation to manage high-interest debt.

- Adjusting savings or investment strategies: Increase contributions to reach your goals faster or rebalance your investment portfolio to align with market conditions and your risk appetite.

- Seeking professional advice: Consider consulting with a financial advisor for personalized guidance, especially if you’re facing major financial decisions or navigating complex situations.

Building Good Financial Habits

Building good financial habits is fundamental to achieving financial well-being. By adopting responsible practices and integrating them into your daily life, you can gain control over your finances and work towards your financial goals. Here are some key habits to cultivate:

1. Budgeting and Tracking Expenses:

Creating a budget is crucial for understanding your income, expenses, and where your money is going. Track your spending meticulously using budgeting apps, spreadsheets, or a notebook. Analyze your spending patterns to identify areas where you can cut back and save more.

2. Saving Regularly:

Make saving a priority by automating regular transfers to your savings account. Aim to save at least 20% of your income. Even small amounts saved consistently over time can accumulate significantly.

3. Managing Debt Wisely:

Minimize and manage debt effectively. Prioritize paying down high-interest debts first, such as credit cards, while making timely payments on all debts. Explore options for debt consolidation or balance transfers to potentially reduce interest charges.

4. Setting Financial Goals:

Establish clear financial goals, both short-term and long-term. This will provide you with direction and motivation. Your goals might include buying a home, saving for retirement, or funding your children’s education.

5. Living Below Your Means:

Avoid overspending and strive to live below your means. Differentiate between needs and wants, and prioritize spending on essentials. Resist impulsive purchases and consider the long-term financial implications of your spending decisions.

Seeking Professional Advice

While this article provides basic information about personal finance, it’s crucial to understand that everyone’s financial situation is unique. What works for one person might not work for another. Therefore, seeking advice from qualified financial professionals can be immensely beneficial.

Here are some situations where professional financial advice is highly recommended:

- You’re struggling with debt and need help creating a repayment plan.

- You’re planning for major life events like buying a home, starting a family, or retirement.

- You’ve received a significant sum of money (inheritance, work bonus) and are unsure how to manage it.

- You want to start investing but feel overwhelmed by the options.

- You need help with complex financial matters like estate planning or tax optimization.

Types of financial advisors:

- Financial Planners: Offer comprehensive financial planning services, including budgeting, saving, investing, insurance, and estate planning.

- Investment Advisors: Specialize in investment management and can help you create a portfolio aligned with your risk tolerance and financial goals.

- Certified Public Accountants (CPAs): Experts in tax planning and preparation.

Choosing the right advisor:

When selecting a financial advisor, it’s essential to choose someone trustworthy, qualified, and experienced in the areas you need assistance. Look for certifications like CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst). Consider their fee structure and ensure it aligns with your budget and needs.

Conclusion

Mastering personal finance basics is crucial for financial stability. Budgeting, saving, and investing wisely are key to achieving long-term financial goals.

{kind=link}