In the digital age, credit cards have become an essential tool for managing finances. Learn how to leverage credit cards wisely to maximize benefits and avoid falling into debt traps.

Understanding Credit Card Terms

Before you can use a credit card wisely, you need to understand the terms and conditions that come with it. These terms can significantly impact how much you end up paying and how your credit score is affected.

Here are some key credit card terms to familiarize yourself with:

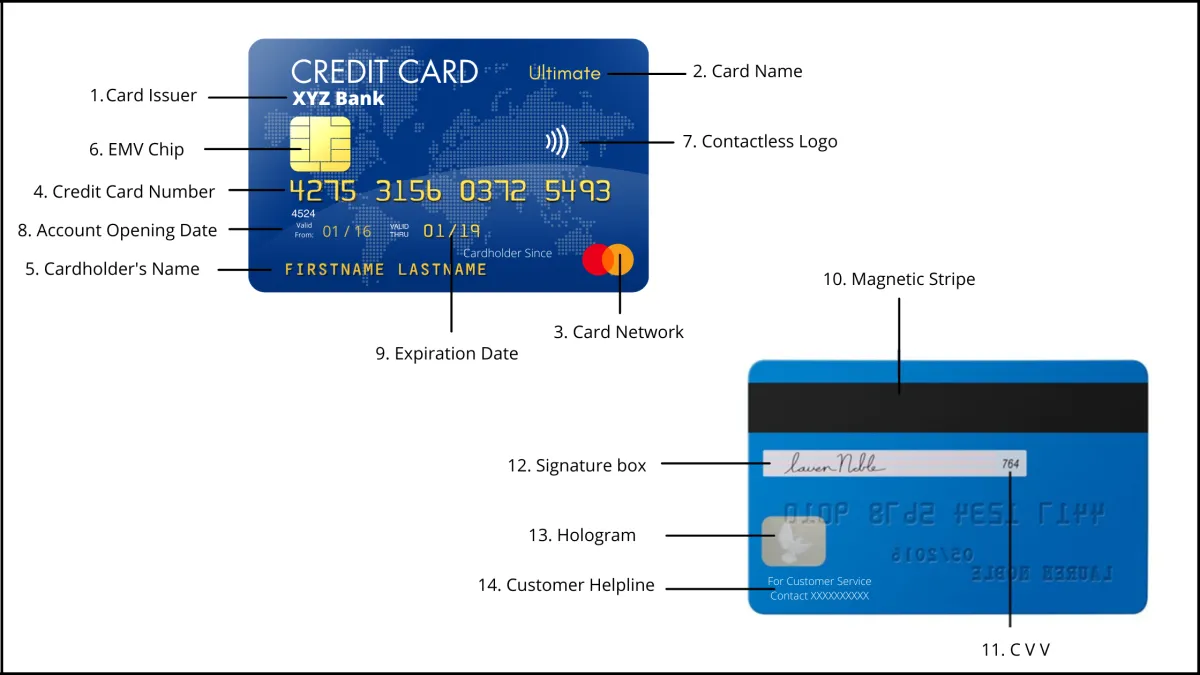

- APR (Annual Percentage Rate): This is the yearly interest rate you are charged on any outstanding balance. It’s crucial to compare APRs as a lower rate means less interest accrued.

- Credit Limit: This is the maximum amount of money you can borrow on your credit card. It’s important to stay well below your credit limit to maintain a good credit utilization ratio (the percentage of available credit you’re using), which impacts your credit score.

- Minimum Payment: This is the minimum amount you need to pay each month to avoid late fees. However, only paying the minimum can keep you in debt for years due to accruing interest.

- Grace Period: This is the time you have to pay your balance in full before interest is charged. If you pay within this period, you essentially avoid interest charges, making this a powerful tool for saving money.

- Balance Transfer: This allows you to transfer a balance from one credit card to another, often with the incentive of a lower introductory APR. This can be a good strategy for paying off high-interest debt, but watch out for balance transfer fees.

- Fees: Credit cards can come with various fees, such as annual fees, late payment fees, balance transfer fees, and foreign transaction fees. Be aware of these fees and factor them into the overall cost of using your credit card.

By taking the time to thoroughly understand these key terms, you can empower yourself to use your credit card responsibly and avoid common pitfalls.

Choosing the Right Credit Card

With countless credit card options available, finding the right one can feel overwhelming. However, selecting a card that aligns with your spending habits and financial goals is crucial for responsible credit card use. Here’s a breakdown to help you navigate the selection process:

1. Understand Your Spending Habits

Before you start comparing cards, analyze your monthly expenses. Identify categories where you spend the most, such as groceries, dining, travel, or gas. This analysis will help you determine which card benefits would be most valuable to you.

2. Explore Different Card Types

- Rewards Cards: These cards offer points, miles, or cashback on your purchases. Some cards provide bonus rewards in specific spending categories, making them ideal if your spending aligns.

- Cash Back Cards: These cards offer a percentage back on your purchases, typically ranging from 1% to 5%. Some cards offer higher cashback rates on rotating categories or specific merchants.

- Travel Rewards Cards: These cards allow you to earn points or miles redeemable for flights, hotels, and other travel expenses. They often come with travel perks like airport lounge access or travel insurance.

- Balance Transfer Cards: These cards offer a low or 0% introductory APR on balance transfers for a set period, typically 12 to 21 months. They can be beneficial for consolidating high-interest debt.

- Low APR Cards: These cards have a consistently low APR, making them suitable for carrying a balance or making large purchases you plan to pay off over time.

3. Consider Fees and Interest Rates

Pay close attention to the card’s APR, annual fees, balance transfer fees, and foreign transaction fees. Choose a card with fees and interest rates that fit your budget and financial situation.

4. Read the Fine Print

Before applying for a credit card, thoroughly read the terms and conditions. Understanding the card’s features, fees, and rewards program will help you avoid surprises and maximize its benefits.

Using Credit Cards for Necessities

While it’s generally advised to avoid using credit cards for unnecessary expenses, there are situations where using them for necessities can be acceptable, even beneficial. However, it’s crucial to approach this strategy with caution and a clear plan to avoid falling into debt.

What qualifies as a “necessity”? Necessities are essential goods or services you need to live and function daily. This typically includes:

- Groceries

- Utilities (electricity, gas, water)

- Transportation costs (gas, public transport)

- Rent or mortgage payments

- Essential medical expenses

When to consider using a credit card for necessities:

- Earning rewards or cash back: Some credit cards offer generous rewards programs, allowing you to earn points, miles, or cash back on your spending. If you can pay off your balance in full each month, using your card for necessities can maximize these rewards.

- Emergency situations: In a financial emergency, like an unexpected car repair or medical bill, using a credit card can provide a temporary safety net.

- Building credit: Using a credit card responsibly and paying it off on time can help you build a positive credit history, which is essential for obtaining loans, mortgages, or even renting an apartment.

Important considerations:

- Budget carefully: Before using your credit card, ensure you have enough money in your budget to cover the purchase and pay off the balance in full when your statement arrives.

- Track your spending: Monitor your credit card transactions closely to stay on top of your spending and avoid overspending.

- Avoid interest charges: Pay your credit card balance in full and on time every month to avoid accruing high-interest charges, which can quickly negate any rewards or benefits earned.

Paying Your Balance in Full

One of the most crucial aspects of using credit cards responsibly is paying your balance in full by the due date each month. This practice helps you avoid accruing interest charges, which can quickly add up and lead to debt. When you carry a balance, you’re essentially taking out a high-interest loan from your credit card issuer.

Here’s why paying in full is essential:

- Avoid Interest Charges: Credit card interest rates can be incredibly high. By paying your balance in full, you effectively use the card’s credit line interest-free.

- Maintain Good Credit Score: Your payment history makes up a significant portion of your credit score. Consistently paying on time and in full demonstrates responsible credit management.

- Stay Out of Debt: Carrying a balance month-to-month can easily spiral into a cycle of debt that’s difficult to break free from.

Avoiding Cash Advances

While credit cards offer a convenient way to pay, it’s crucial to understand how different card features work to use them responsibly. One such feature that often comes with high costs is the cash advance.

A cash advance allows you to use your credit card to withdraw cash, either from an ATM or through bank tellers. However, unlike regular purchases, cash advances come with several drawbacks:

- High Fees: Cash advances typically incur a hefty fee, often a percentage of the amount withdrawn or a minimum flat fee, whichever is greater.

- High APR: Unlike purchases, which may have a grace period, interest charges on cash advances usually accrue immediately at a much higher APR than regular purchases.

- Impact on Credit Utilization: A high credit utilization ratio can negatively impact your credit score, making it appear riskier to lenders.

Alternatives to Cash Advances

Instead of resorting to cash advances, consider these alternatives:

- Emergency Fund: A dedicated emergency fund can help cover unexpected expenses without relying on credit.

- Budgeting and Saving: By tracking your income and expenses, you can identify areas to reduce spending and allocate funds for potential cash needs.

- Short-Term Loan: While not ideal, a short-term loan from a credit union or family member may offer lower fees and interest rates compared to cash advances.

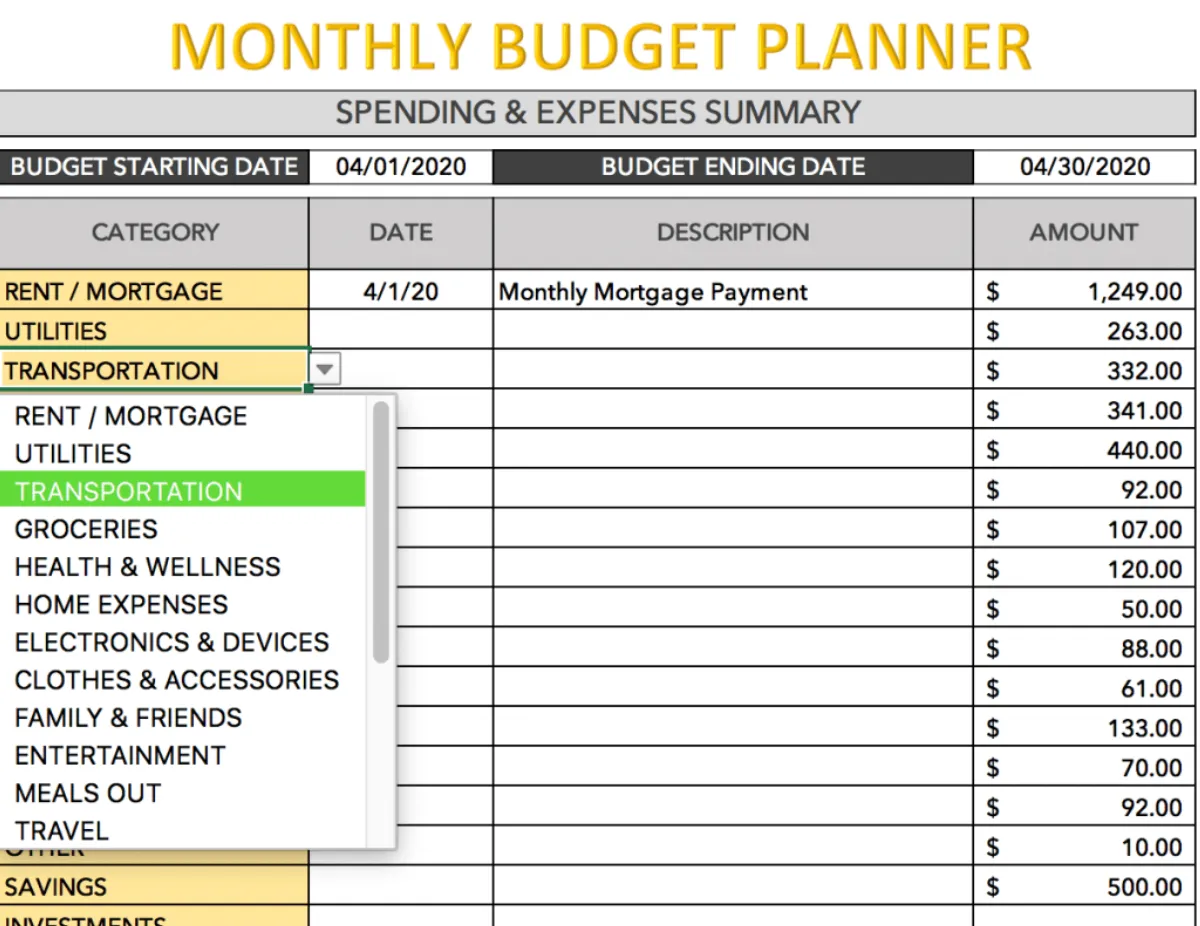

Monitoring Your Spending

Keeping track of your credit card spending is crucial in using credit cards responsibly and avoiding debt. Here are some tips for effectively monitoring your spending:

1. Utilize Budgeting Tools and Apps

Numerous budgeting apps and tools can help you track your credit card expenses. These tools can link to your credit card accounts and categorize your spending, giving you a clear picture of where your money is going.

2. Regularly Review Your Statements

Don’t wait for the paper bill to arrive. Make it a habit to review your credit card statements online at least once a week, if not more frequently. This allows you to spot any errors or fraudulent transactions quickly.

3. Set Spending Limits for Different Categories

Create a budget and allocate specific spending limits for different categories, such as dining, entertainment, or groceries. Monitor your spending against these limits to ensure you’re staying on track.

4. Track Your Spending in Real-Time

Take advantage of mobile banking apps that allow you to track your credit card transactions in real time. This can help you stay mindful of your spending habits and make necessary adjustments.

5. Use Account Alerts

Set up account alerts to notify you of specific transactions, such as when you approach your credit limit or make a large purchase. These alerts provide timely reminders and help you stay on top of your spending.

6. Reconcile Your Transactions

Regularly reconcile your credit card transactions with your bank statements. This helps identify any discrepancies or errors and ensures that all charges are legitimate.

Setting a Credit Limit

A credit limit is the maximum amount of money a lender will allow you to borrow on your credit card. It’s a crucial aspect of responsible credit card use and plays a significant role in managing your debt.

When choosing a credit limit, consider your income and spending habits. A lower credit limit can be a useful tool to manage spending and avoid overextending your finances. It acts as a safeguard, limiting the potential debt you can accumulate.

On the other hand, a higher credit limit might seem tempting, but it’s important to proceed with caution. While it offers greater spending power, it also increases the risk of accumulating significant debt, especially if you encounter unexpected financial difficulties.

Contact your credit card issuer to discuss your credit limit options. They can help you determine a suitable credit limit based on your financial situation and creditworthiness. Remember, having a credit card doesn’t mean you should max it out every month. Responsible credit card use involves staying well within your limit and managing your spending wisely.

Building an Emergency Fund

Having a safety net of readily available cash is crucial to using credit cards wisely and avoiding debt. Unexpected expenses like car repairs, medical bills, or job loss can quickly derail your finances if you’re unprepared. That’s where an emergency fund comes in.

An emergency fund is a separate savings account specifically designed to cover unexpected costs, preventing you from relying on credit cards and accumulating high-interest debt.

How much should you save?

Aim to save at least three to six months’ worth of living expenses in your emergency fund. This may seem daunting, but start small and gradually increase your savings over time.

Where to keep your emergency fund:

Keep your emergency fund in an easily accessible account, such as a high-yield savings account or money market account. Avoid investing this money, as you want it to be readily available when needed.

Using Credit Card Rewards Responsibly

Credit card rewards programs can seem like a fantastic way to earn free travel, cashback, or other perks. However, it’s crucial to use them responsibly to avoid falling into debt. Here’s how to make the most of your rewards without jeopardizing your financial health:

1. Understand Your Earning and Redemption Options

Not all rewards programs are created equal. Some cards offer higher rewards rates in specific spending categories, while others have a flat rate for all purchases. Familiarize yourself with your card’s terms and conditions, including:

- Earning Rates: How many points or miles do you earn per dollar spent in different categories?

- Redemption Value: What is the value of your rewards points or miles when redeemed for different options like travel, merchandise, or statement credits?

- Expiration Policies: Do your rewards points expire, and if so, under what circumstances?

2. Don’t Spend More to Earn Rewards

The most important rule of responsible credit card use is to avoid spending money you don’t have just to earn rewards. Treat your credit card like cash and only make purchases you can afford to pay off in full each month.

3. Pay Your Balance in Full and On Time

Rewards are only beneficial if you’re not racking up high-interest charges. Always pay your credit card balance in full and on time to avoid interest fees that can quickly negate any rewards you earn.

4. Track Your Spending and Rewards

Keep a close eye on your credit card statements and use budgeting tools or apps to monitor your spending. Regularly check your rewards balance and understand your redemption options. This awareness will help you make informed decisions about your spending and reward redemption strategy.

Seeking Professional Advice

While this article provides a general guide on using credit cards wisely, seeking advice from a certified financial advisor is crucial for personalized strategies. A financial advisor can help you:

- Analyze your current financial situation: They will assess your income, expenses, debts, and credit score to understand your financial standing.

- Develop a personalized budget: Based on your financial goals, they can create a budget that optimizes your credit card usage and debt management.

- Explore debt consolidation options: If you have existing debt, they can explore options like balance transfers or debt consolidation loans to potentially lower interest rates.

- Recommend suitable credit cards: They can help you find cards with rewards programs and benefits that align with your spending habits and financial goals.

- Provide ongoing support: Financial advisors offer continued guidance and adjust strategies as needed, ensuring you stay on track with responsible credit card use.

Remember, seeking professional financial advice empowers you to make informed decisions tailored to your unique circumstances, maximizing the benefits of credit cards while minimizing the risk of debt.

Conclusion

In conclusion, by practicing responsible spending habits and making timely payments, individuals can effectively use credit cards to their advantage while avoiding debt traps.

{kind=link}