Learn effective strategies to rebuild your credit after bankruptcy, including budgeting tips, securing a secured credit card, and timely payment practices. Regain your financial footing and improve your credit score with these actionable steps.

Understanding Bankruptcy

Bankruptcy is a legal process that provides individuals and businesses facing overwhelming debt with a fresh start. It’s a court-supervised proceeding where you either work out a plan to repay creditors or liquidate assets to pay off debts. While bankruptcy can provide much-needed relief, it leaves a significant mark on your credit report, making it harder to access credit in the future.

There are different types of bankruptcy, with Chapter 7 and Chapter 13 being the most common for individuals.

- Chapter 7 bankruptcy, also known as liquidation bankruptcy, involves selling off non-exempt assets to pay off creditors. This option is typically for those with limited income and assets.

- Chapter 13 bankruptcy, or reorganization bankruptcy, allows individuals with regular income to propose a repayment plan to creditors over three to five years. This option helps retain assets while addressing debt.

Understanding the type of bankruptcy you filed and its impact on your credit score is crucial. Both Chapter 7 and Chapter 13 bankruptcies stay on your credit report for years – Chapter 7 for 10 years and Chapter 13 for seven. During this period, obtaining new credit can be challenging and often comes with higher interest rates.

Creating a Budget

After bankruptcy, creating and sticking to a budget is crucial for rebuilding your credit. A budget allows you to track your income and expenses, identify areas where you can cut back, and free up money to put towards debt repayment and savings.

Here’s how to create a realistic budget:

- Track your income and expenses. Write down all sources of income and track every dollar you spend for a month. Use a budgeting app, spreadsheet, or notebook.

- Categorize your expenses. Divide your expenses into categories like housing, transportation, food, utilities, and entertainment.

- Identify areas to reduce spending. Look for non-essential expenses you can cut back on or eliminate, such as dining out, entertainment subscriptions, or expensive hobbies.

- Set realistic financial goals. Determine how much you can realistically afford to save and allocate towards debt repayment each month. Start small and gradually increase the amount as your finances improve.

- Monitor and adjust your budget regularly. Review your budget monthly, track your progress, and make adjustments as needed. Life changes, and your budget should reflect those changes.

Building an Emergency Fund

While it may seem counterintuitive to save while you’re still digging out of debt, having an emergency fund is crucial after bankruptcy. This safety net prevents you from falling back into bad financial habits, like relying on credit cards, when unexpected expenses arise.

Here’s why it’s important:

- Prevents further debt: An emergency fund covers unexpected costs like medical bills or car repairs, preventing you from using credit cards and accumulating new debt.

- Reduces financial stress: Knowing you have funds set aside for emergencies provides peace of mind and reduces the stress associated with unexpected financial burdens.

- Supports credit rebuilding: While building an emergency fund doesn’t directly impact your credit score, it establishes responsible financial behavior that can lead to better credit management in the long run.

How to build your emergency fund:

- Set a realistic savings goal: Aim for at least $1,000 initially, then gradually build towards 3-6 months’ worth of living expenses.

- Create a budget: Track your income and expenses to identify areas where you can cut back and redirect funds towards savings.

- Automate your savings: Set up automatic transfers from your checking to your savings account to make saving consistent and effortless.

- Find extra income sources: Consider a side hustle, selling unused items, or taking on freelance work to boost your savings efforts.

Opening a Secured Credit Card

One of the most effective ways to rebuild credit after bankruptcy is through a secured credit card. Unlike traditional credit cards, secured cards require a security deposit that typically equals your credit limit. This deposit minimizes the risk for the lender, making them more accessible to individuals with poor credit history.

Here’s how a secured credit card can help you rebuild your credit:

- Establishes a Positive Payment History: By making on-time payments on your secured card, you demonstrate responsible credit behavior, which is reported to the credit bureaus.

- Builds Credit Utilization: Keep your credit utilization ratio low (below 30%) by charging small amounts and paying your balance in full each month.

- Offers a Fresh Start: A secured card provides a clean slate to establish positive credit, gradually improving your credit score over time.

When choosing a secured credit card:

- Compare fees, such as annual fees, late payment fees, and foreign transaction fees.

- Look for cards that report to all three major credit bureaus (Experian, Equifax, and TransUnion).

- Consider cards with potential for graduation, where you may be upgraded to an unsecured card after a period of responsible use.

Using Credit Responsibly

Rebuilding credit after bankruptcy requires a cautious approach to using credit. The way you manage your credit now directly impacts your future creditworthiness. Here’s how to use credit responsibly during your rebuilding phase:

1. Secured Credit Cards: Your Stepping Stone

Secured credit cards are excellent tools for rebuilding credit. These cards require a security deposit that typically equals your credit limit, minimizing risk for lenders. Use your secured card for small, essential purchases and pay the balance in full and on time each month.

2. Limited Credit Applications: Slow and Steady Wins the Race

Avoid applying for multiple credit accounts in a short period. Each application can result in a hard inquiry on your credit report, potentially lowering your score. Focus on building a positive payment history with one or two accounts before considering others.

3. Budgeting and Timely Payments: The Cornerstones of Creditworthiness

Create a realistic budget that prioritizes debt payments. Set reminders for due dates to ensure timely payments. Late payments can severely damage your credit score, even if they’re just a few days late.

4. Monitor Your Credit Report: Stay Informed

Regularly review your credit report from all three credit bureaus (Experian, Equifax, and TransUnion). Look for inaccuracies and dispute any errors immediately. Staying informed empowers you to address issues promptly and track your progress.

5. Patience is Key: Rebuilding Takes Time

Rebuilding credit is a gradual process. It takes time to demonstrate responsible credit behavior and for positive information to outweigh negative marks on your credit history. Be patient, remain consistent with your financial habits, and celebrate your progress along the way.

Paying Bills on Time

After a bankruptcy, demonstrating responsible financial behavior is key to rebuilding your credit. One of the most impactful ways to do this is by consistently paying your bills on time. Payment history carries significant weight on your credit score, and a string of on-time payments shows lenders you are committed to managing your finances responsibly.

Here’s how to prioritize on-time payments:

- Set Reminders: Utilize calendar alerts, mobile apps, or even written notes to remind yourself of upcoming due dates.

- Automate Payments: Whenever possible, set up automatic payments for recurring bills like utilities, loans, or credit card minimums.

- Create a Budget: A realistic budget allows you to track income and expenses, ensuring you have funds available when bills are due.

- Communicate with Creditors: If you anticipate difficulty meeting a payment deadline, reach out to your creditor proactively. They may offer temporary hardship programs or adjusted payment plans.

By making on-time payments a non-negotiable habit, you’ll steadily improve your credit score and demonstrate to lenders that you’re a trustworthy borrower.

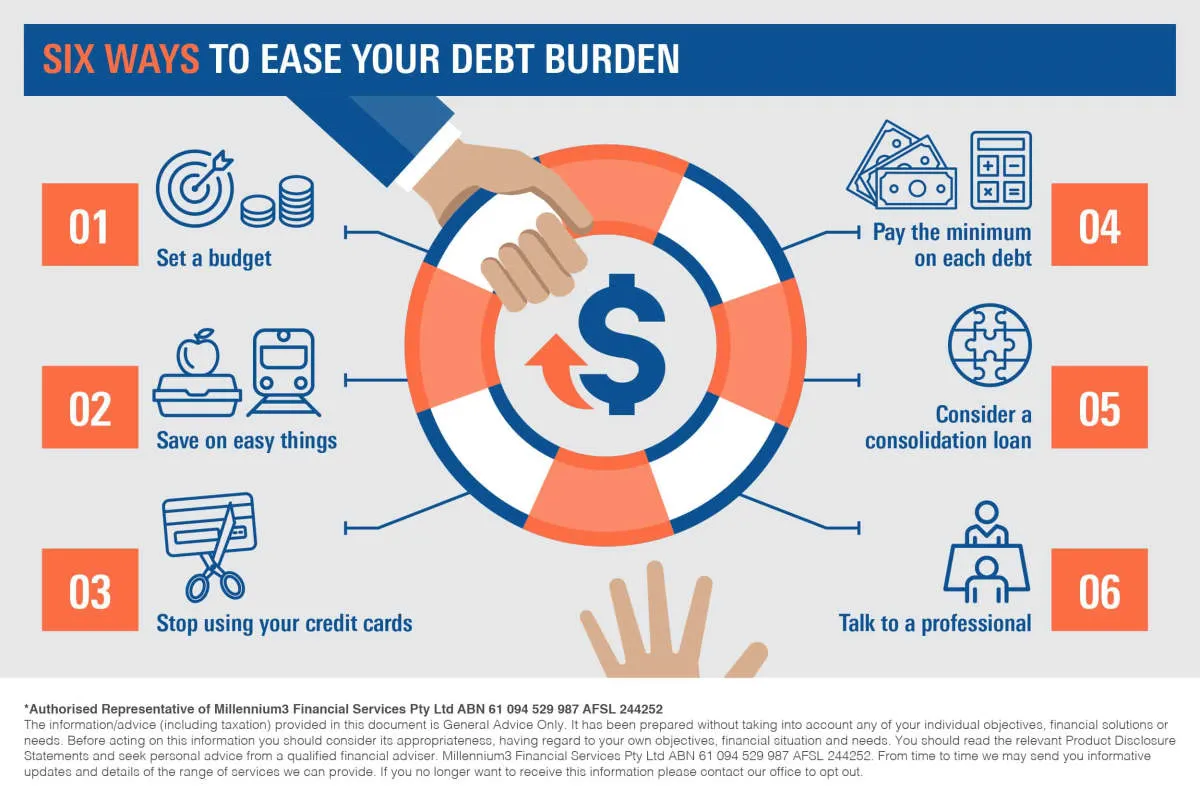

Keeping Balances Low

One of the most impactful factors in your credit score after bankruptcy is your credit utilization ratio. This ratio represents the amount of credit you’re using compared to your total available credit. Keeping this ratio low is crucial for rebuilding your credit. Here’s why and how:

Why Low Balances Matter:

A high credit utilization ratio signals to lenders that you might be relying too heavily on credit. This can be interpreted as a sign of financial strain and make you appear riskier. Keeping balances low, on the other hand, demonstrates responsible credit management and can lead to a better score.

Strategies for Low Balances:

- Keep track of spending: Use a budgeting app, spreadsheet, or notebook to monitor your expenses and avoid overspending.

- Pay down existing debt: Prioritize paying down existing credit card balances to reduce your overall utilization.

- Use cards strategically: If you have multiple cards, focus on using one or two and keep the balances low. Avoid maxing out cards.

- Request credit limit increases: While this doesn’t directly lower your balance, it can improve your credit utilization ratio by increasing your available credit.

- Consider a secured card: A secured credit card requires a security deposit that typically becomes your credit limit. Responsible use can help build a positive payment history and lower your utilization.

Avoiding New Debt

After bankruptcy, rebuilding your credit requires a cautious approach to new debt. While it might seem counterintuitive, taking on some forms of credit responsibly can be beneficial for your credit score. However, it’s crucial to avoid falling back into old habits that led to financial trouble. Here’s how to navigate new debt:

Exercise Extreme Caution

Avoid applying for new credit immediately after bankruptcy. Your credit report will reflect the bankruptcy for several years, making it difficult to get approved for loans or credit cards with favorable terms. Instead, focus on building a positive credit history through other means.

Start Small and Manage Responsibly

- Secured Credit Cards: Consider a secured credit card, which requires a cash deposit as collateral. Use it for small purchases and pay the balance in full and on time every month.

- Credit Builder Loans: These loans involve borrowing a small amount that’s held in a savings account. You make regular payments, and upon completion, you receive the borrowed amount plus any accrued interest.

- Authorized User Status: Ask a trusted friend or family member to add you as an authorized user on their credit card. Ensure they have good credit and responsible spending habits, as their account activity will reflect on your credit report.

Create a Realistic Budget

Before taking on any new debt, create a detailed budget that tracks your income and expenses. Ensure you can comfortably afford the monthly payments without accumulating more debt.

Resist Temptation

Credit card offers and loan solicitations may be tempting, but it’s crucial to resist the urge to overextend yourself financially. Remember your goals for rebuilding your credit and prioritize responsible financial habits.

Checking Your Credit Report

After a bankruptcy, taking stock of where your credit stands is the first step towards rebuilding. You might be surprised at how much your credit score has been impacted. It’s essential to get a clear picture of your credit report and understand the information it holds.

You are entitled to a free credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – every 12 months through AnnualCreditReport.com. These reports will detail your credit history, including accounts in good standing, late payments, collections, and public records such as bankruptcy.

Carefully review each report for errors or inaccuracies, as these can negatively affect your score. If you find any discrepancies, dispute them immediately with the respective credit bureau. It’s crucial to ensure that your credit report reflects your financial situation accurately as you embark on the journey to rebuild your credit.

Seeking Professional Advice

While it’s possible to rebuild your credit on your own after bankruptcy, seeking professional guidance can be incredibly beneficial. Consider these options:

1. Credit Counseling Agencies

Non-profit credit counseling agencies can provide valuable advice on budgeting, debt management, and credit rebuilding. They can help you understand your credit report, create a personalized action plan, and may even offer educational workshops.

2. Financial Advisors

For more comprehensive financial planning, consider consulting with a financial advisor. They can help you establish healthy financial habits, explore investment opportunities, and create a long-term strategy for rebuilding your credit as part of an overall financial plan.

3. Bankruptcy Attorneys

If you’re considering bankruptcy or have recently filed, consulting with a bankruptcy attorney is crucial. They can guide you through the legal processes, protect your rights, and ensure you understand the long-term financial implications.

4. Choosing the Right Professional

When seeking professional advice, it’s important to choose reputable and qualified individuals or organizations. Research their credentials, experience, and client reviews before making a decision.

Conclusion

Rebuilding credit after bankruptcy requires patience and discipline. By focusing on timely payments, responsible credit utilization, and monitoring your credit report, you can gradually improve your credit score and financial standing.

{kind=link}