Learn effective strategies to quickly boost your credit score with our comprehensive guide on improving your financial standing. Discover actionable tips and tricks to elevate your credit rating in no time.

Understand Your Credit Score

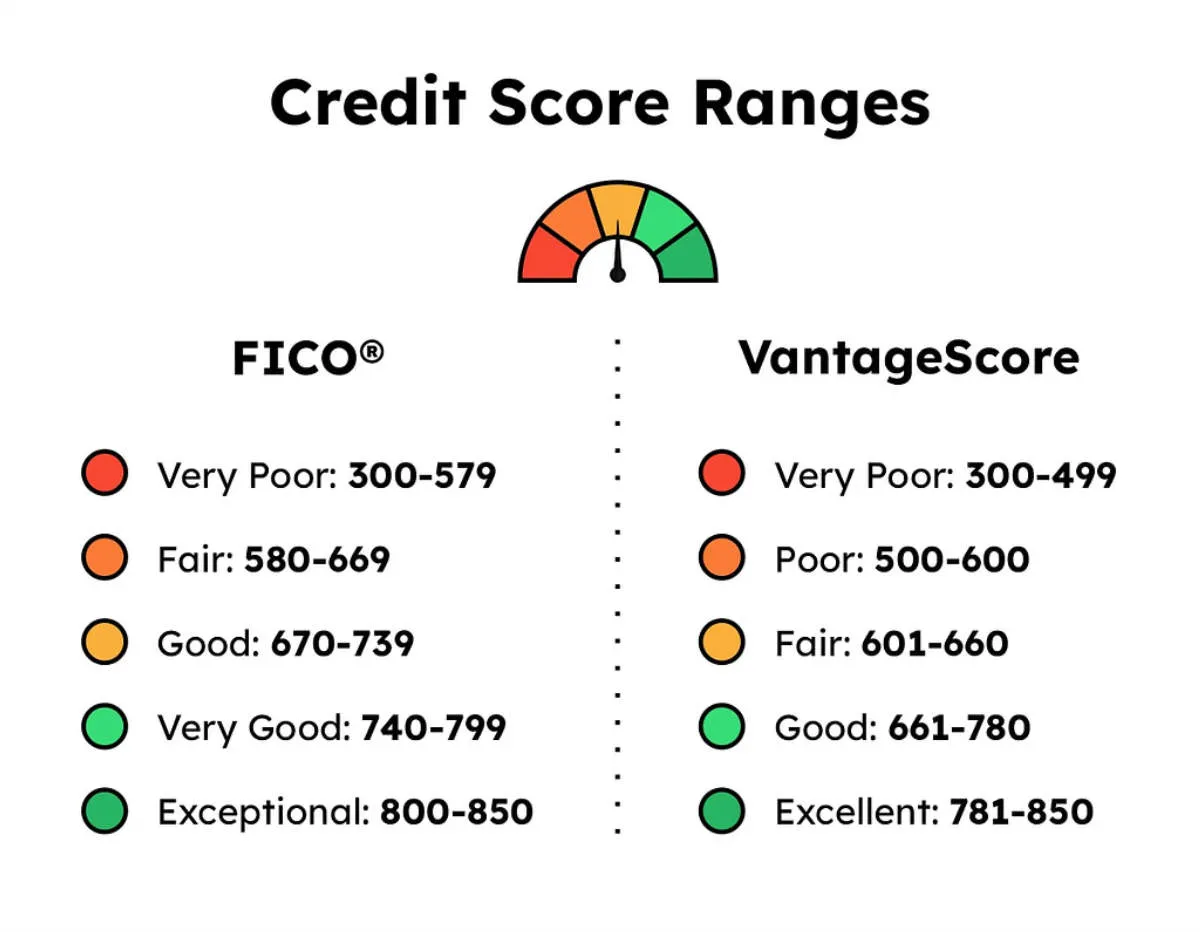

Before you can improve your credit score, you need to understand what it is and what factors influence it. Your credit score is a three-digit number, typically ranging from 300 to 850, that represents your creditworthiness. Lenders use this score to assess the risk of lending you money. A higher score indicates lower risk, making you more likely to be approved for loans and credit cards with favorable terms.

Here are the key factors that affect your credit score:

- Payment History (35%): The most crucial factor is whether you pay your bills on time. Late payments, collections, and bankruptcies can severely damage your score.

- Amounts Owed (30%): This refers to your credit utilization ratio, which is the amount of credit you use compared to your total credit limit. Keeping your balances low, ideally below 30%, demonstrates responsible credit management.

- Length of Credit History (15%): A longer credit history generally results in a better score, as it shows lenders your long-term financial behavior.

- Credit Mix (10%): Having a mix of credit types, such as credit cards, installment loans, and mortgages, can positively impact your score, indicating diverse borrowing experience.

- New Credit (10%): Applying for new credit frequently can lower your score, as it suggests increased risk. Each hard inquiry, which occurs when lenders check your credit report, can temporarily ding your score.

Check Your Credit Report

The first step to improving your credit score is understanding where you currently stand. This begins with obtaining your credit report from each of the three major credit bureaus: Equifax, Experian, and TransUnion.

You can access your credit reports for free once a year from each bureau through AnnualCreditReport.com. Regularly checking your reports allows you to:

- Identify inaccuracies: Look for errors such as accounts that don’t belong to you, incorrect balances, or duplicate entries. Dispute any inaccuracies with the respective credit bureau.

- Spot potential issues: Your credit report highlights factors affecting your score, like late payments or high credit utilization. This awareness helps you prioritize areas needing improvement.

- Track your progress: As you take steps to improve your credit, regularly checking your report lets you monitor the effectiveness of your efforts and make adjustments as needed.

Remember, improving your credit score is an ongoing process. Regularly reviewing your credit reports is crucial for maintaining good credit health and achieving your financial goals.

Pay Your Bills on Time

This is the most crucial factor in building good credit. Late payments can significantly hurt your credit score, and the damage can linger for years. Lenders want to see that you’re responsible and can manage your finances. Here’s how to make sure you always pay on time:

Set Reminders

Use calendar alerts, mobile apps, or even good old-fashioned sticky notes to remind yourself when bills are due. Don’t rely solely on receiving paper bills, as mail can be delayed.

Automate Payments

Most banks and service providers offer automatic payment options. This ensures your bills are paid on time, even if you forget. Just make sure you have enough funds in your account to cover the payments.

Negotiate Due Dates

If you’re struggling with a particular due date, contact the creditor and see if it’s possible to change it. Many companies are willing to work with you to find a more convenient payment schedule.

Don’t Miss Minimum Payments

If you can’t pay the full amount due, at least make the minimum payment by the due date. This shows creditors you’re making an effort and helps avoid late fees.

Reduce Outstanding Debt

One of the most impactful ways to improve your credit score is by reducing your outstanding debt. Credit utilization, the ratio of your credit card balances to your credit limits, is a major factor in determining your score. Lowering your utilization demonstrates responsible credit management and can lead to a significant score boost.

Here are some effective strategies to reduce your outstanding debt:

1. Create a Budget and Identify Areas to Cut Back

Start by analyzing your income and expenses. Identify areas where you can cut back on non-essential spending and redirect those funds towards debt repayment. Even small reductions can make a difference over time.

2. Prioritize High-Interest Debt

Focus on paying down your debts with the highest interest rates first, such as credit cards. This approach minimizes the amount of interest you accrue, allowing you to pay off your debt faster.

3. Explore Debt Consolidation Options

If you have multiple debts with high interest rates, consider consolidating them into a single loan with a lower rate. This can simplify your payments and potentially save you money on interest.

4. Negotiate with Creditors

Don’t be afraid to reach out to your creditors and try to negotiate lower interest rates or monthly payments. They may be willing to work with you, especially if you’re committed to repaying your debt.

5. Consider a Balance Transfer Credit Card

A balance transfer credit card allows you to transfer your existing balances to a new card with a promotional 0% APR period. This can provide temporary relief from high interest rates, giving you time to focus on paying down your debt.

Avoid Opening New Credit Accounts

While it might seem counterintuitive, opening several new credit accounts in a short period can actually harm your credit score. Here’s why:

- Hard inquiries: Each time you apply for new credit, lenders make a “hard inquiry” on your credit report. These inquiries can slightly lower your score, especially if you have multiple inquiries within a short time frame.

- Lower average credit age: A significant factor in your credit score is the length of your credit history. Opening new accounts lowers your average credit age, which can negatively impact your score, especially if you don’t have a long credit history to begin with.

- Increased credit utilization: Even if you don’t use the new credit accounts, they increase your total available credit. This can lead to a higher credit utilization ratio (the amount of credit you’re using compared to your total available credit), which can lower your score.

Instead of opening new accounts, focus on managing your existing credit responsibly. Make on-time payments, keep your balances low, and avoid closing old accounts in good standing.

Keep Old Accounts Open

The length of your credit history, which reflects how long you’ve been managing credit, accounts for 15% of your credit score. Closing old accounts, even if you don’t use them anymore, can actually hurt your score in several ways:

- Reduced average age of accounts: Closing your oldest account can significantly shorten your average credit history length, potentially lowering your score.

- Lower credit utilization ratio: Closing an account removes its credit limit from your overall available credit. This can increase your credit utilization ratio, especially if you have outstanding balances on other cards. A higher utilization rate can negatively impact your score.

Instead of closing old accounts, consider keeping them open and using them occasionally for small purchases that you can pay off quickly. This demonstrates responsible credit management and helps preserve the positive history associated with those accounts.

Limit Credit Inquiries

Every time you apply for a new credit card or loan, lenders often make a “hard inquiry” into your credit report. These inquiries can slightly lower your credit score, usually by a few points, as they signal to lenders that you might be taking on more debt. While a few inquiries over a long period are not a major concern, multiple inquiries in a short time can raise red flags.

Here’s why limiting credit inquiries is important:

- Impact on credit score: Hard inquiries can stay on your credit report for up to two years, potentially affecting your ability to get favorable interest rates or loan approvals.

- Perception of risk: Multiple inquiries in a short period can make you appear financially unstable or desperate for credit to lenders.

Tips for Limiting Credit Inquiries:

- Plan your credit applications: If you’re shopping around for a loan or credit card, try to do it within a short timeframe (e.g., within a 30-day period). Many credit scoring models will count multiple inquiries within this window as one inquiry, minimizing the impact on your score.

- Check your credit report and score regularly: Before applying for new credit, review your credit report for any errors and get a sense of where your score stands. This helps you avoid unnecessary applications.

- Consider alternatives: Explore alternative financing options, such as credit builder loans or secured credit cards, which may not require a hard inquiry.

Dispute Errors on Your Credit Report

One of the fastest ways to improve your credit score is to identify and dispute any errors on your credit report. Mistakes happen, and they can negatively impact your score without you even realizing it. Here’s how to tackle those inaccuracies:

1. Obtain Copies of Your Credit Reports

You can access your credit reports for free from the three major credit bureaus – Equifax, Experian, and TransUnion – through AnnualCreditReport.com. Review each report carefully for any inconsistencies.

2. Identify Errors to Dispute

Look for inaccuracies such as:

- Incorrect personal information (name, address, Social Security number)

- Accounts that don’t belong to you

- Inaccurate account balances or credit limits

- Late payments that were actually made on time

- Duplicate accounts

3. Gather Supporting Documentation

To strengthen your dispute, collect any relevant documents that support your claim. This might include:

- Bank statements

- Credit card statements

- Loan agreements

- Utility bills

- Proof of identity

4. File Your Dispute

You can dispute errors directly with the credit bureau(s) reporting the inaccuracies. Most bureaus offer online dispute portals, but you can also dispute by mail or phone. Provide specific details about each error and include copies of your supporting documents.

5. Follow Up and Monitor Your Progress

The credit bureau has 30 days to investigate your dispute. They will notify you of the outcome and provide an updated credit report if any changes were made. Continue to monitor your reports regularly to ensure accuracy.

Use Credit Wisely

One of the most effective ways to improve your credit score is by demonstrating responsible credit card use. This doesn’t mean avoiding credit altogether; instead, it’s about using it strategically and responsibly. Here’s how:

Keep Credit Utilization Low

Credit utilization, or your credit utilization ratio, is the amount of available credit you’re currently using. It’s a major factor influencing your credit score. A good rule of thumb is to keep your credit utilization below 30%, and ideally below 10%.

For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000, and ideally below $1,000. This demonstrates to lenders that you’re not overly reliant on credit and manage your finances responsibly.

Pay Your Bills On Time, Every Time

Payment history is the most crucial factor affecting your credit score. Late payments, even by a few days, can negatively impact your score and remain on your credit report for years. Set up automatic payments or reminders to ensure timely payments for all your credit accounts.

Avoid Opening Too Many Accounts in a Short Time

Each time you apply for new credit, a hard inquiry is generated on your credit report. Multiple hard inquiries in a short period can lower your score, as it signals to lenders that you might be a higher risk borrower. Focus on maintaining a healthy mix of credit accounts you already have and be mindful of applying for new credit only when necessary.

Monitor Your Credit Regularly

Regularly monitoring your credit reports is essential for maintaining a healthy credit score. It allows you to identify any inaccuracies, errors, or signs of fraudulent activity that could be negatively impacting your creditworthiness.

You can access your credit reports for free from the three major credit bureaus – Equifax, Experian, and TransUnion – through AnnualCreditReport.com. It’s advisable to review your report from each bureau at least once a year, or more frequently if you suspect any issues.

When reviewing your credit reports, pay close attention to the following:

- Personal Information: Verify that your name, address, Social Security number, and other personal details are accurate and up to date.

- Credit Accounts: Review all listed credit accounts, including credit cards, loans, and mortgages, to ensure they belong to you and the information is correct.

- Payment History: Check for any late or missed payments, as these can significantly lower your score. Dispute any inaccuracies with the respective creditor and credit bureau.

- Credit Utilization: Calculate your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. High credit utilization can hurt your score, so aim to keep it below 30%.

- Negative Items: Look for any negative marks, such as collections, charge-offs, or bankruptcies. These can stay on your report for several years and severely impact your score. If you find any errors, dispute them immediately.

Conclusion

Improving your credit score quickly and effectively requires disciplined financial habits, timely payments, keeping credit card balances low, and monitoring your credit report regularly. By following these steps, you can enhance your creditworthiness and access better financial opportunities.

{kind=link}